Landstar System’s Inc. (NASDAQ: LSTR) conference call with analysts and investors on Thursday was summed up best by company President and CEO Jim Gattoni. “I can’t wait to get through this first quarter. I think it will be our most challenging quarter of the year.”

The asset-light third-party logistics provider sees several headwinds on the horizon in first-quarter 2020, following a fourth-quarter 2019 earnings report that was well below consensus expectations.

Market fundamentals weak

For starters, the company’s guidance calls for loads hauled via truck and revenue per truck load to decline in the mid-single-digit range year-over-year, in line with what the market has yielded to Landstar so far in January. Gattoni said that Landstar has seen some stability in volume and price so far this year, but noted that the market remains soft.

The company’s flatbed business, typically one-third of total revenue, remains under pressure as most industrial sectors are in decline. Gattoni said that industrial markets typically take four to six quarters to recover and noted that the year-over-year declines only began in July.

He went on to make a bit of a contrarian call to what most of the asset-based truckload (TL) carriers have been voicing in regard to capacity. Gattoni doesn’t believe that the truckload market will tighten in the second quarter of 2020 like some and noted that capacity tightening will likely take longer to play out as the demand just isn’t there yet.

Gattoni does view increases in insurance premiums and claims expenses, which he expects to continue to force carriers to exit the market, as a near-term catalyst for improving the excess truck supply dynamic. He noted that in addition to the very large jury awards that the trucking industry has seen in recent months, even minor incidents are “turning fender benders into million dollar accidents.”

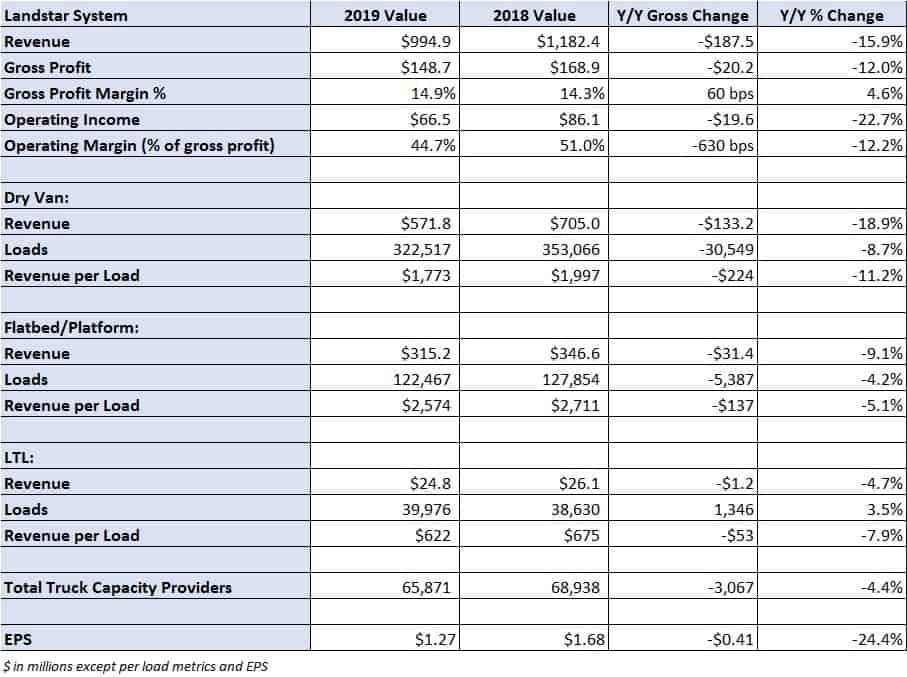

Landstar has felt the financial impact from increased insurance and claims expenses. The company’s fourth-quarter earnings shortfall, earnings per share (EPS) of $1.27 versus the consensus estimate of $1.42 and the company’s prior guidance of $1.40 to $1.46, was “entirely attributable to insurance and claims costs,” according to the earnings press release.

Additionally, the company’s first-quarter EPS guidance of $1.10 to $1.20, well below analysts’ expectation of $1.34 for the quarter, excludes the potential financial impact from another “tragic vehicular accident involving a fatality.” While Landstar reported that it is too early to determine the financial impact from this event – the company has up to $8.5 million of loss exposure or $0.16 per share – it noted that the lower than expected first-quarter guidance is in jeopardy.

“It is highly likely that, once all facts are determined, the estimated ultimate cost of this tragic accident will reduce first-quarter diluted earnings per share to an amount below the low end of the company’s 2020 first-quarter diluted earnings per share guidance,” Gattoni stated in the earnings press release.

Fourth-quarter 2019

Fourth-quarter 2019 was “characterized by soft demand, weakness in the U.S. manufacturing sector and readily available truck capacity,” according to Gattoni.

Total revenue for the company was 16% lower year-over-year at $995 million, within management’s prior guidance range of $970 million to $1.02 billion. Dry van loads declined 9% year-over-year with an 11% decline in revenue per load. Landstar’s platform business managed to hold up better with loads down 4% year-over-year and revenue per load down 5%.

Total truck capacity providers declined 4% year-over-year, which Gattoni said was largely due to the decline in volumes available in the Landstar network as overall demand has softened.

Gross profit margin improved 60 basis points (bps) year-over-year to 14.9%, but operating margin — defined as operating income as a percentage of gross profit — declined 630 bps year-over-year to 44.7%. Again, the company’s insurance and claims expense line drove the bulk of the margin underperformance.

Gross profit margin is expected to improve sequentially again in first-quarter 2020 to a range of 14.9% to 15.2%.

Cash deployment

Management guided to free cash flow of $175 million to $225 million in 2020, lower than the $288.4 million generated in 2019. With only $15 million to $20 million in planned capital expenditures in 2020, Gattoni said that the company will continue to buy back stock, specifically making reference to the stock’s pullback in after-hours trading following the company’s announced earnings miss.

“This is the cycle where you might see some activity on the buybacks,” Gattoni said on the call. Landstar repurchased nearly 850,000 shares of its stock in 2019 and has 1.85 million shares available for repurchase under its current authorization.

The company capped off its financial performance in 2019, “second-best” only to 2018, utilizing its strong financial position to pay a one-time special dividend of $2 per share in December.

Shares of LSTR have rallied back from a near 5% decline following the open to only 2% lower on the day.