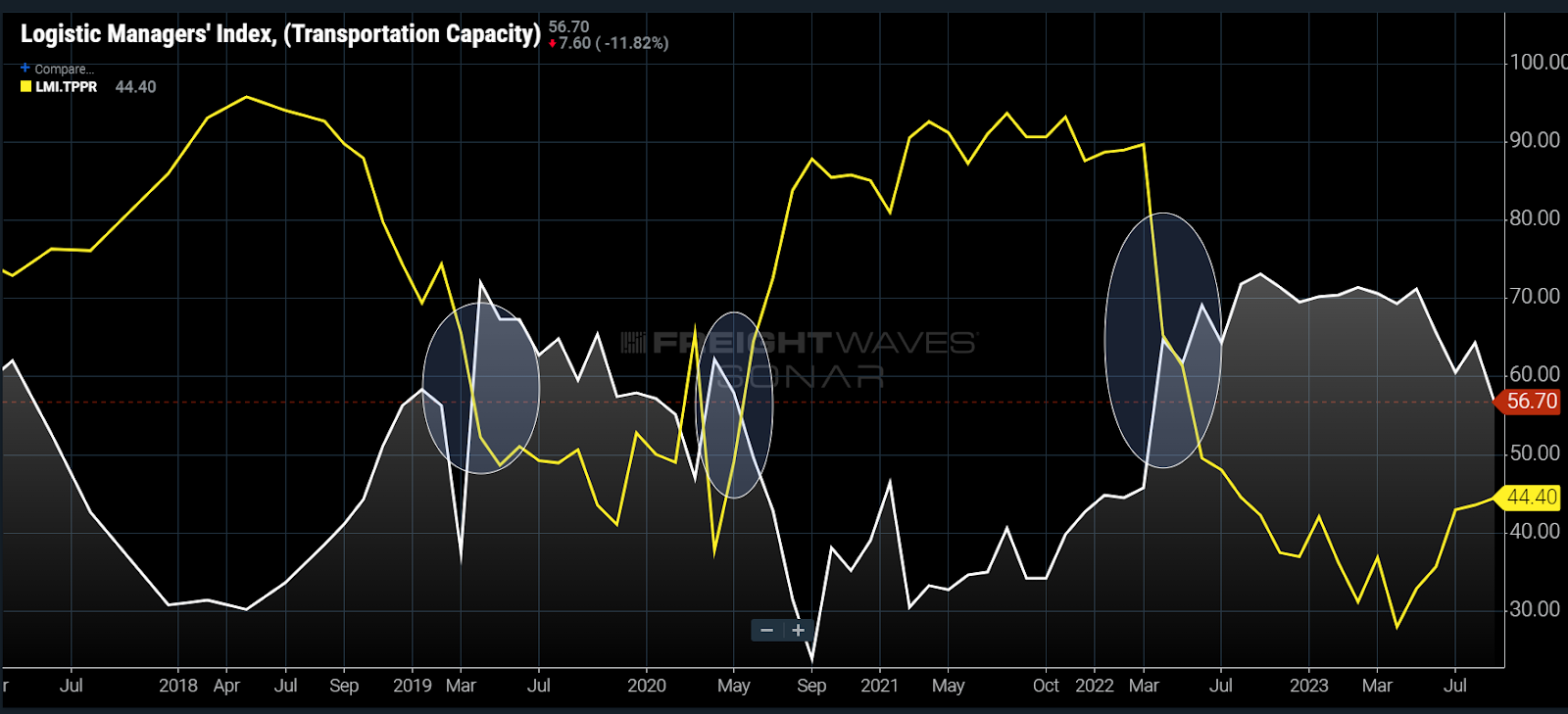

Chart of the Week: Logistics Managers’ Index – Transportation Capacity, Transportation Prices SONAR: LMI.TPCP, LMI.TPPR

When the Logistics Managers’ Index (LMI) transportation capacity component falls below the transportation price figure, capacity is relatively tight. When the inverse is true, capacity is generally loose. The past few months are trending toward another flip that may suggest equilibrium of supply and demand is closer than we thought in the transportation market.

The LMI has proven to be very accurate in describing domestic transportation market conditions over the past several years. In the generally soft 2019 market, the price index was below the capacity index. In June 2020, the two components flipped and remained in strong opposition until March 2022.

The LMI is a diffusion index based on surveys of more than 300 supply chain professionals measuring various components of the transportation and logistics space. Values above 50 indicate expansion, while sub-50 readings are indicative of contraction.

The most recent October reading for prices was 44.4, indicating that prices were contracting but at a much slower pace than the 28 that was printed in April. The October capacity value was 56.7, which was down significantly from the 71 that occurred in May.

As you can tell, over the past five years, there has been little balance in the transportation markets, moving violently from very tight to very loose. COVID can be blamed for most of this. The 2017-18 market was also very tight but was considered a “black swan” type of environment at the time.

The reality is that the economic stability (or stagnation depending on your perspective) of the post-2009 recession may have been the real anomaly. Economically speaking, there are more questions than answers and that will keep companies on edge and more prone to erratic behavior — especially in shipping.

In this past week’s Freightonomics, Zac Rogers, assistant professor of supply chain management at Colorado State University and contributor to the LMI, talked about how shippers have reverted to more of a just-in-time pattern of shipping as demand remains uncertain and warehousing costs have increased.

He also cited how Yellow’s exit has seemingly helped accelerate the perception of a decline in available capacity and propped prices at higher levels. One thing that isn’t clear is to what scale this is occurring.

Tender rejection rates, which measure the rate carriers reject or turn down requests for truckload capacity from their customers, bottomed in May as well and have been trending higher since then — suggesting the correlation between Yellow’s exit could be spurious to some extent.

Regardless of the reasoning, there are multiple data sources painting the same picture. Capacity is tightening, though still not enough to generate disruption — yet. The larger question remains around just when will freight market participants feel some noticeable and more consistent service disruptions.

Caveats are always a thing

Possibly the most uncertain aspect of predicting a freight market turn is the underlying economics. The advance release of the Q3 GDP produced one of the most disconnected values in recent history in terms of economic perception.

The 4.9% quarterly growth figure seemed somewhat unbelievable in the context that it would normally be considered a value that is indicative of an economic boom. But the Federal Reserve economists seemingly dismissed the figure and consumer confidence declined.

The consumer spending that fed the figure has become increasingly leveraged with credit card debt and the labor market is showing signs of weakening as people are having increasing difficulties finding employment as continued claims have hit their highest values since late 2021.

In the near-term future, the gap between the two LMI figures may reverse course over the winter if traditional seasonality returns. January and February tend to be the slowest months of the year for shipping. This would push demand down, widening the gap between the capacity ceiling temporarily.

The gap between the LMI capacity and price figures has shrunk from 41 to 12 over a five-month period. The sheer momentum suggests we may be closer to a market flip than we think, but the longest yard is always the last one.

About the Chart of the Week

The FreightWaves Chart of the Week is a chart selection from SONAR that provides an interesting data point to describe the state of the freight markets. A chart is chosen from thousands of potential charts on SONAR to help participants visualize the freight market in real time. Each week a Market Expert will post a chart, along with commentary, live on the front page. After that, the Chart of the Week will be archived on FreightWaves.com for future reference.

SONAR aggregates data from hundreds of sources, presenting the data in charts and maps and providing commentary on what freight market experts want to know about the industry in real time.

The FreightWaves data science and product teams are releasing new datasets each week and enhancing the client experience.

To request a SONAR demo, click here.

Rishi

To the comments attacking brokers, what world are you living in. We are not making any money,. This article is so spot on. As a broker I am struggling with getting trucks for the price, which everybody would have been happy with few weeks back. I cant get trucks, despite waiving my commission. Customers need to realize its not the same market anymore, but it takes time.