RXO: Too much trucking capacity heading into 2024

On Wednesday, FreightWaves hosted the Domestic Supply Chain Summit, a virtual event with RXO Chief Strategy Officer Jared Weisfeld as the keynote speaker. The interview, conducted by enterprise trucking carrier expert Thomas Wasson, included an outlook for 2024 and highlighted the biggest supply chain challenges and opportunities. RXO is the freight brokerage that was spun off from LTL carrier XPO last year.

Excess truckload capacity and carrier exits were a central theme. Weisfeld noted that since October 2022, each month has seen more net revocations in operating authorities than carriers entering the market. He added, “That’s encouraging but not yet at the pace that’s required to bring that load-to-truck ratio above where it is right now, which is about 3-to-1. The long-term average is about 4-to-1. You’ll start seeing the spot market reemerge when we start seeing that punch up above that. There’s still too much capacity in the market.”

Another topic highlighted was the growth in 3PL/brokerage market penetration that began during the consumer COVID- and stimulus-inspired spending boom. Weisfeld told Wasson, “If you look at 3PL/brokerage penetration as a percentage of the for-hire truckload market, we estimate about a year ago it was around a low 20%, up from close to 10% a decade ago.” Asked if this trend will continue, Weisfeld was bullish, adding, “If you’re a shipper and can get better access to technology, incredible service, more flexibility — we think that penetration can increase to 40-50% over the long term, as a percentage of the $400 billion for-hire truckload market. We think RXO is going to be a winner in that trend.”

Experts caution structural risks to supply chain remain

On Thursday, FreightWaves’ Rachel Premack wrote an article arguing that the impacts of the pandemic on supply chains may not have caused any lasting structural changes. Premack writes, “Ultimately, the reason we’re no longer in a supply chain crisis isn’t that companies did anything particularly amazing to overhaul their manufacturing and distribution systems. Rather, we just started buying less stuff than we did in the peak of 2020 to 2021 — and corporations were able to catch up at last.”

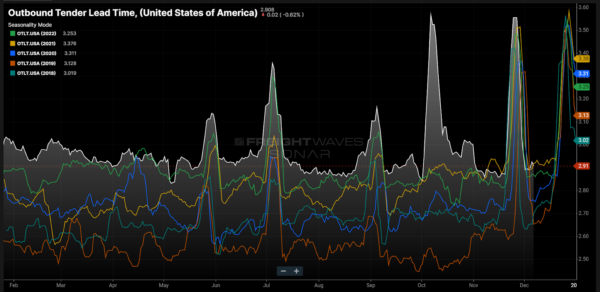

This comes as Outbound Tender Lead Times (OTLT) in 2023 remain elevated and are 10%-15% higher than pre-pandemic levels. Dustin Jalbert, senior economist of wood products at FastMarkets RISI, adds, “I don’t think a lot has changed. I think a lot of people assume that there was a paradigm shift during the pandemic … . Structurally, nothing has really changed in the market from a supply standpoint.” Given lower transportation costs and abundance of truckload capacity, there appears to be little incentive to keep higher inventory levels in the face of uncertain consumer demand.

“We are not seeing retailers/manufacturers embrace higher inventory,” notes Sandy Gosling, a partner in consultancy McKinsey’s Miami office. “In fact, most of what we see being reported is inventory being right sized after many months of being too high. Of course, this varies by industry and will continue to remain an important trade-off for companies as they consider lead time due to source locations, cost to carry, and service levels to their customers.”

Market update: Cass November data suggests painful peak season

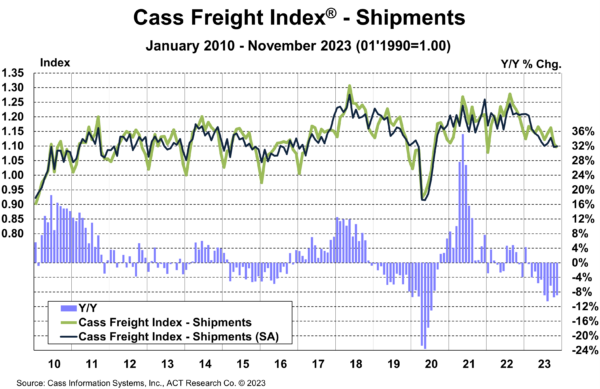

On Thursday, freight audit and payment provider Cass Information Systems released its November Transportation Index report, “Painful Peak Season Proceeds.” The Cass shipments index fell 1.3% month over month (m/m) and is down 8.9% year over year. The report notes the larger y/y declines “remain exaggerated by unusual excess inventory repositioning in 2H’22.”

The total amount spent on freight also saw declines, with the Cass Freight Expenditures Index falling 1.3% m/m in November and down 26% y/y. The report infers that rates were flat in the past month as both shipments and expenditures fell 1.3% m/m. It adds that private fleet expansion continues to pull freight from the for-hire truckload market, but the report notes changing supply patterns may disrupt this trend. Net revocations of operating authorities remain at record levels driven by falling pent-up capex and lower freight rates.

Regarding freight expectations, the report notes some optimism, adding, “We continue to expect modest y/y growth in consumer spending this holiday season, driven by the acceleration in real disposable incomes and the ongoing strong labor market. The recent easing in fuel prices improves our confidence that peak season will end on a higher note.”

FreightWaves SONAR spotlight: DOE/EIA fuel price falls below $4 per gallon

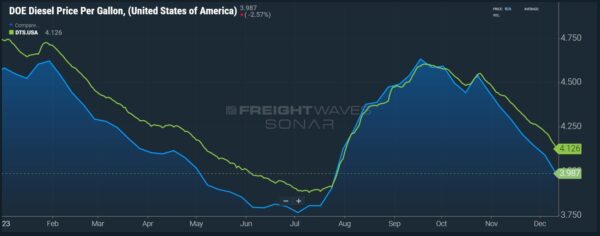

Summary: On Monday, the Department of Energy/Energy Information Administration reported that the nationwide weekly retail diesel price at the pump fell 10.5 cents per gallon to $3.987. The last time the DOE/EIA fuel price was below $4 per gallon was July 24. Diesel prices paid at the pump are 76 cents per gallon lower than this time last year.

FreightWaves’ John Kingston wrote that the current early downward movement for diesel markets partly stems from winter weather not arriving, with forecasts for the next two weeks predicting considerably higher-than-normal temperatures for December. Another factor to watch is futures market movement. Kingston wrote, “Monday’s decline in the DOE/EIA price came as the futures market for ultra low sulfur diesel on the CME commodity exchange has reversed itself significantly over the past two trading days after seven days of declines.”

According to the EIA’s short-term energy outlook, crude oil prices, which make up around 46% of the retail price of diesel, are expected to rise into 2024. The report cites the recently announced OPEC+ production cuts totaling around 2.2 million barrels per day as a catalyst for higher Brent crude spot prices into 2024. The current December spot average of $78 per barrel is expected to rise to $84 per barrel in the first half of 2024. For domestic production, the report is more upbeat, stating, “We expect net exports of U.S. crude oil and petroleum products to reach a record high of almost 2.0 million barrels per day (b/d) in 2024, up from around 1.8 million b/d this year and 1.2 million b/d in 2022. This growth is primarily driven by an increase in U.S. crude oil and hydrocarbon gas liquids production.”

The Routing Guide: Links from around the web

Some Convoy carriers say collapsed startup owes them thousands of dollars (FreightWaves)

Trailer side-guard rule likely delayed until at least October 2024 (FreightWaves)

Terminal raises $3.1M, wants to be the ‘Plaid of trucking’ (FreightWaves)

Motive Monthly Economic Report — December 2023 (Motive)

Republicans pan truck speed limiter proposal at House hearing (FreightWaves)

California asks EPA for waiver to implement Advanced Clean Fleets rule (FreightWaves)

Stephen Webster

Need to lmit trucks coming from Canada and Mexico to those drivers that have been at least in Canada or Mexico for a min of 30 months live and drive truck in Canada 🇨🇦 and set a min wage on the U S soilof $25 U S a hr plus medical