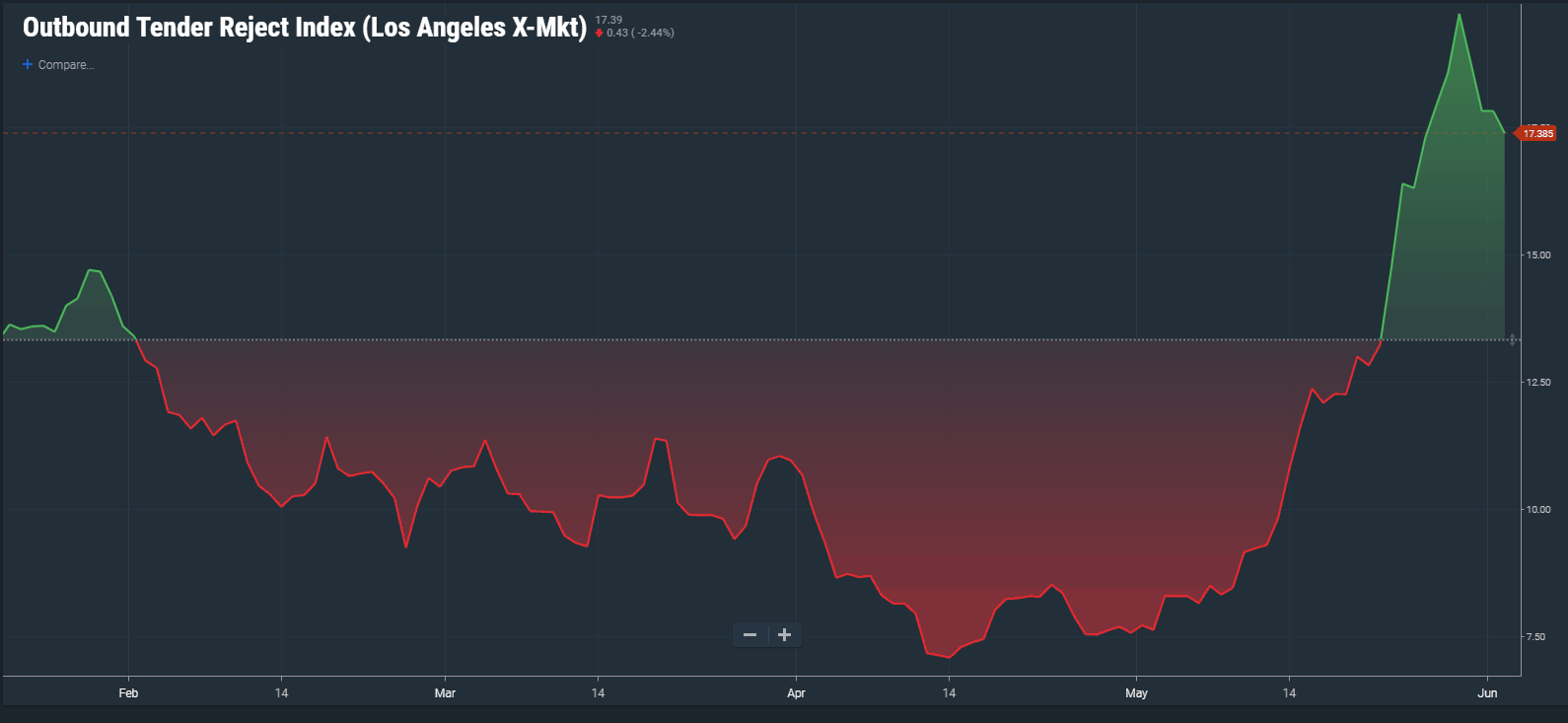

The Southern California freight market is waking up after a sleepy early spring, according to FreightWaves SONAR Outbound Tender Rejection Index (OTRI). The freight markets are starting to show some localized destabilization as we enter the warmer months. With areas like Florida and the middle of the country experiencing spikes in tender rejections earlier in the spring due to commodity flows, the Los Angeles market is showing its first signs of potential longer-run capacity concerns since before the Chinese New Year.

With many areas of the country experiencing uncharacteristic heated winter spot market activity, when freight volumes are traditionally low, the Los Angeles market was exhibiting signs of stabilization. After hitting a high in late January on tender rejections around 14.7%, the L.A. market started an erratic up and down journey to bottom out around 7% in mid April. Starting in early May the loads rejected began to spike to just under 20%.

Last year about this time we saw a delayed produce season create a huge capacity crunch, which is partially to blame this year. We saw reefer tender rejections out of the LA market move from 17.5% to the mid-twenties in early to late May. The main culprit could be the containers hitting the ports in Southern California as production in China returned following the Chinese New Year shut down.

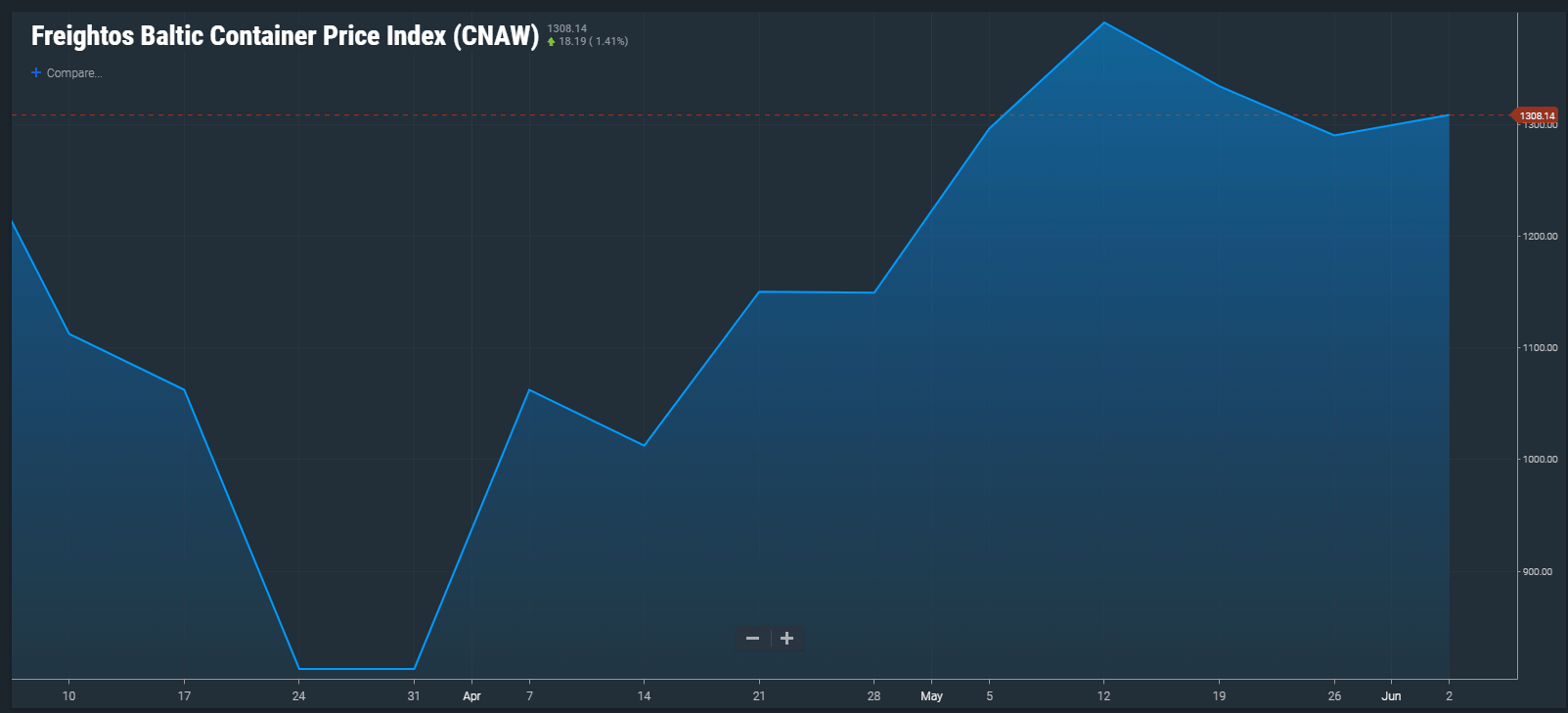

According to the Freightos Baltic Container Price Index, an index that measures the price of a container, the cost has surged 27% in the past month and a half from China to the North American West Coast. The average price for a container movement from China to the American West coast went from $1011 per container on April 14th to $1290 in late May, a sign that container volumes are surging into the ports.

Rates from China to the North American East coast show an increase in as well, further validating the shipping volume surge out of Asia. The impact was not as significant with rates only increasing 16% in the same period in that lane.

The port of Long Beach is reporting a preliminary estimate of an 8.4% year-over-year increase in loaded inbound TEUs (twenty-foot equivalent units) in the month of April and a 16% increase in TEUs from March of this year. The significance here is in relation to the ongoing trade situation between the United States and China as some manufacturers could be pressing volume out prior to any tariff implementation. The increase in year over year volume could also just imply that production has increased due to the economy staying relatively strong.

Carriers may have been taken off guard as the spike in port volumes combined with a slightly soft onset of the produce season created an imbalance in trucking networks. DAT is seeing increases in the spot market in response to this. The Los Angeles to Atlanta lane is showing an 18% increase in rate per mile in the last 7 days versus April. The Los Angeles to Dallas lane is also showing an 18% upsurge over the same period.

The significance of the surge in volume, and subsequently rates, is that the port surge is not an unusual occurrence this time of year. Every May sees a general increase in port volume, and every spring the produce moves off the West coast in volume. Even though carriers knew what was coming the market has destabilized.

Stay up-to-date with the latest commentary and insights on FreightTech and the impact to the markets by subscribing.