Shares of truckload (TL) carrier USA Truck Inc. (NASDAQ: USAK) are off more than 20% a day after the company reported a $4.5 million fourth-quarter loss. That eclipses the $1.1 million loss it reported in the third quarter of 2019.

Even as management laid out plans to stem losses on the company’s earnings call with analysts and investors, the stock continued to gap down.

The updated plan

Since new management arrived in 2017, the carrier has undergone a myriad of initiatives aimed at improving tractor utilization and driving revenue per tractor per week higher. With the latest worse-than-expected loss, management provided more detail around the company’s strategic objectives.

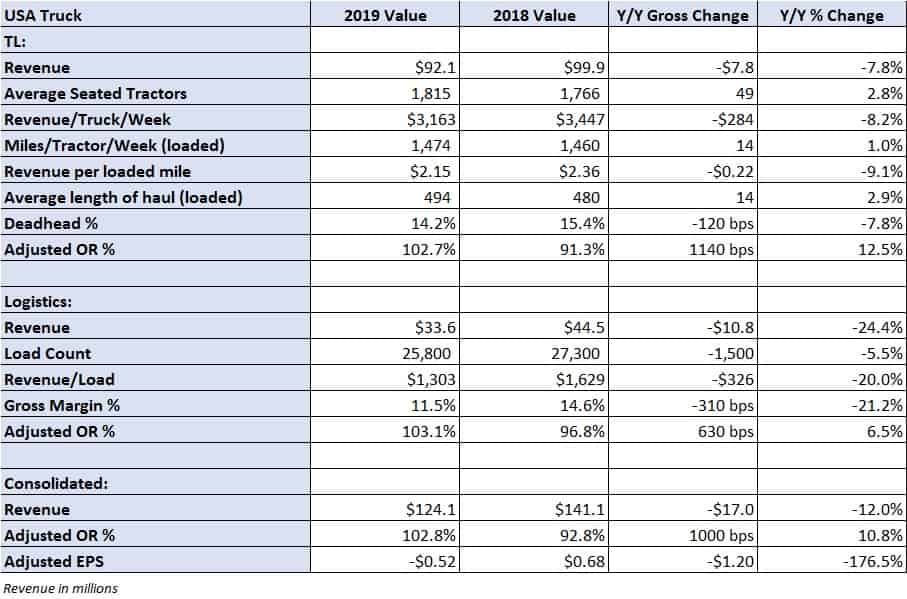

Management believes that the company can achieve a $300 improvement on revenue per truck per week by improving utilization of the existing fleet. In fourth quarter 2019, the carrier reported a 1% year-over-year increase in loaded miles per truck per week. However, revenue per truck declined 8% year-over-year, or $284 on a weekly basis, as the rate it received to haul freight (revenue per loaded mile) declined 9%. Excess truck capacity paired with only modest freight demand are the reasons the carrier saw declines in both contractual and spot rates.

USA Truck was more reliant on the spot market during the quarter, which accounted for roughly 9% of revenue compared to only 6% in the fourth quarter of 2018. Historically, the spot market accounts for less than 5% of USA Truck’s revenue. Management noted that the year-over-year increase in spot market exposure was an effort to prop up utilization. The company’s spot market exposure did decline sequentially from the 15% level experienced in the third quarter.

In efforts to lower exposure to the spot market, USA Truck more than doubled the amount of freight it bid in 2019 compared to 2018. It believes that the 13.9 million loads it bid last year will improve its freight realization, or the number of loads tendered versus awarded, on its contracted freight. In 2019, the carrier captured less than two-thirds of the freight it was under contract to potentially receive, much lower than the 80-90% realization level it saw in 2018. That’s not a surprising result given the abundance of capacity the market endured last year.

“The soft spot market and widely reported supply-demand imbalance affected both our contract and spot market opportunities during the quarter. Market rates remained pressured during the quarter and shippers allocated large portions of their freight spend to the lowest cost alternatives,” stated USA Truck President and CEO James Reed in the company’s earnings release.

Every January has been a financial loser for the company over the past five years, but management said they saw an uptick in freight during the month and stated that utilization had improved by 100 miles per tractor per week. However, that statement was quickly tempered with an acknowledgement that the freight was taken to support tractor utilization and that some of the freight is “not the highest rated freight out there,” alluding to the probability that the company has sacrificed yield for volume.

USA Truck is also attempting to increase its driver team capabilities, which could garner another $100 in revenue per truck per week. An “industry competitive team pay” package has been implemented, and the carrier has done away with the practice of keeping new drivers on a training pay scale for extended periods. Management said most of these drivers were leaving the program after 90 days for regular market pay elsewhere. The company’s total driver retention efforts are expected to achieve $750,000 in cost savings.

The company has a network optimization plan in place that could add another $50 in weekly revenue per tractor. Lastly, the carrier looks to increase its dedicated business by 10% seeking to capture more high-touch, higher-priced freight where management believes it provides a service advantage.

January’s looking up, but so are costs

Management seemed encouraged by the improvement seen in January as demand has “inflected positively.” They said that in addition to the utilization improvement, bid compliance was improving. Further, bid activity was easing as USA Truck’s customers are no longer looking to pull forward contractual negotiations, in attempts to lock in lower truck rates while the market remains soft, like they did during a good portion of the fourth quarter. Currently, one-third of the company’s bids are expected to be completed in the first quarter of 2019, which is only a “slightly higher” than normal percentage of bid activity for the period.

Even with the recent improvement, some cost headwinds don’t appear to be abating. Management said insurance expenses and lower truck valuations, as used truck prices have declined, represent roughly $1.5 million in cost increases. The company has accelerated its depreciation and amortization of equipment in attempts to keep these valuations in close proximity to actual values in the market. Also, the 8% nondriver staff reductions implemented in the fourth quarter resulted in $122,000 in severance costs.

The cost headwinds are not likely to be offset by higher rates in the near term. Management said it’s still too early to provide guidance on contractual rates for 2020. However, they believe that rates will be down in the low-single-digit to flat range compared to 2019 at least in the beginning of the year. USA Truck has 41% of its recently bid freight coming on line in the next 45 days, which will provide a good indicator for rates and freight realization for the year.

Levers to pull

Asked about a contingency plan if their restructuring objectives failed, management didn’t vocalize one if it exists. However, they did point to the ability to scale back capital expenditures (capex) if the company became cash strapped. Currently, management expects net capex to be in the range of $20 million to $30 million for 2020, but noted that capex could be reeled in if needed. The company has made significant investments in equipment over the past two years, with the average tractor age declining from 3.3 years to 2.6.

USA Truck has total net debt including leases of $190.5 million or 3.7x net debt-to-earnings before interest, taxes, depreciation, amortization and rent (EBITDAR). This is up from the 3.1x net debt-to-EBITDAR level reported in the third-quarter 2019 report. Additionally, the company had $55.1 million of available borrowing capacity on its credit facility at the close of 2019.

The near term for the carrier is likely to be a bumpy road. Management said the first half of 2020 could resemble the back half of 2019, which resulted in a $5.6 million adjusted net loss for the carrier.

Noble1 suggests SMART truck drivers should UNITE & collectively cut out the middlemen from picking truck driver pockets ! IMHO

Nice cradle on the 15 minute , will it break out ? Could be viewed as a cup & handle too !!!

Stay tuned !

Noble1 suggests SMART truck drivers should UNITE & collectively cut out the middlemen from picking truck driver pockets ! IMHO

There’s a hole in that cup , LOL ! Handle broke . Failure , not yet on the cradle .

IMHO

Noble1 suggests SMART truck drivers should UNITE & collectively cut out the middlemen from picking truck driver pockets ! IMHO

Both patterns on the 15 minute failed , price retraced to the prior day’s low at $5.46 and held the retest so far , and bounced to $5.54 as of this writing , potentially forming a double bottom . If that’s the case , primary target would be $6.06

IMHO

Noble1 suggests SMART truck drivers should UNITE & collectively cut out the middlemen from picking truck driver pockets ! IMHO

Goofed on this one .

Noble1

It’s during times like these that you can find bargains . Some of these companies are worth more than their current market value .

When sentiment is exuberant the complete opposite tends to occur .

Personally I love to see sentiment like the sentiment expressed in the comments above mine when searching for a potential deal . I also adore when sentiment is excessively exuberant when looking for a good short at a peak price as recently occurred with the Dow Jones Industrial Average Index . Everyone who went long and held the DJIA since December 19 2019 has seen all their gains wiped out as of today ! Remember how the herd felt before then ? TO THE MOON ALICE , LOL ! That’s how they felt .

Here they currently feel in HELL it shall go , ROTFLMAO !

In conclusion : Idiots will call the wise idiots . Therefore when being called an idiot , it’s a compliment , LOL !

In my humble opinion …………

Art

Nothing special about this company.

No differentiation or specialization.

Another carrier in a sea of tens of thousands of carriers at the mercy of the market.

JB Hunt owns largest fleet of intermodal containers.

USA Truck has some trucks… just another trucking company losing money.

Dave

US Xpress in the toilet too down 12% right now and down a huge 70% in 18 months. Looks like anything with USA in the name is tanking. 💩💩💩. BAD BAD BAD.