Mexican president puts end to border-skipping

Ocean demand from China to Mexico has grown sharply in recent years, which many attribute to border-skipping. (Chart: SONAR)

The coming months are likely to be marked by sweeping changes to trade policies that shippers, particularly apparel and e-commerce companies, will have to adapt to. Those changes are starting to take place even before President-elect Donald Trump is sworn in for his second administration. On Dec. 19, Mexican President Claudia Sheinbaum issued a decree that effectively ended the “border-skipping” strategy that some e-commerce sellers use to avoid tariffs by importing through Mexico so Chinese-manufactured goods can be treated the same as Mexican-manufactured goods. It appears that the Mexican president is using a Trump-like move to put Mexico first since manufacturing would drive far more employment and economic activity than simply distributing finished goods.

For details, I recommend FreightWaves CEO Craig Fuller’s article here.

Trump’s Panama Canal threats could alter shippers’ plans

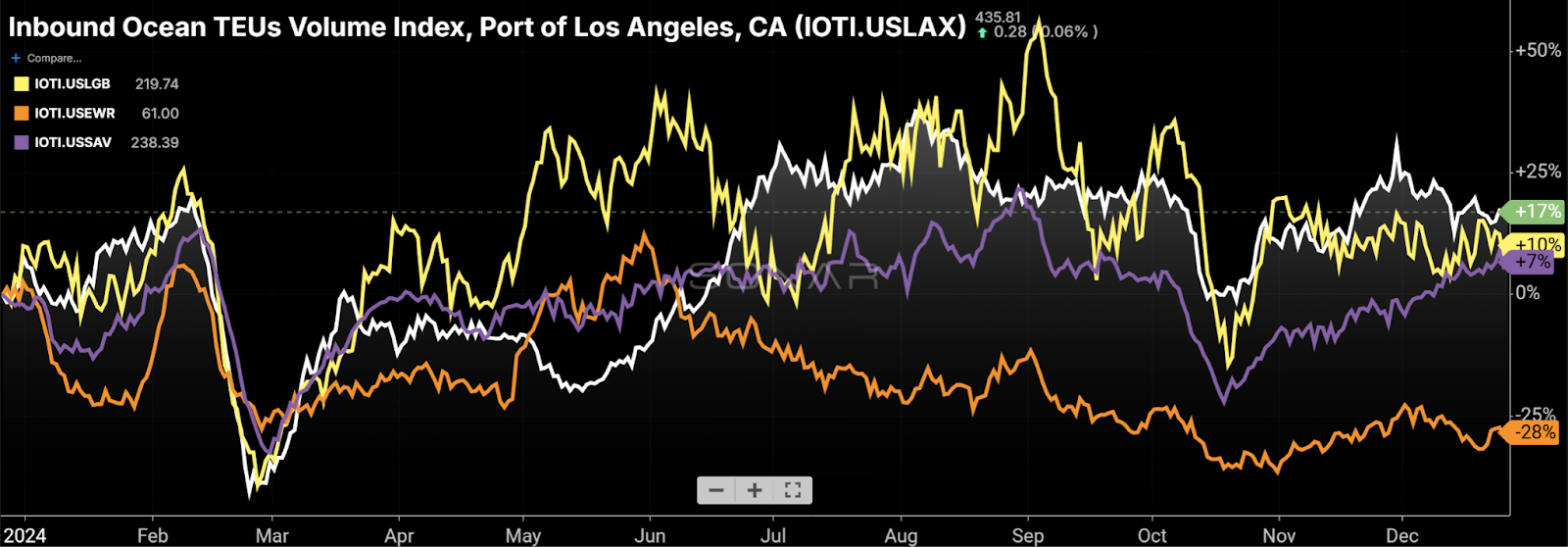

Shippers often opt for routings with the least risk of disruption. Relative to a year ago, import volumes at the West Coast ports have outperformed those at East Coast ports. (SONAR: IOTI.USLAX, IOTI.USLGB, IOTI.USEWR, IOTI.USSAV)

Trump is threatening to demand that the Panama Canal return to U.S. control, which is seemingly related to China’s investment at or near the canal. (See article here for details on the situation and the canal’s importance.) It’s unclear whether anything will come of the threats – the Panamanian government clearly has no interest in ceding control.

Nonetheless, the threats alone could have the positive impacts of reducing fees for U.S. cargo — Trump insists this is one of many ways the U.S. is being “ripped off” — and improving efficiency. However, in the near term, they create risk and potential for disruption as the issue gets more heated. Shippers hate risk, and many will likely choose to avoid using the Panama Canal entirely for freight where that is an option. This move would pertain largely containerized cargo that originates in East Asia and is ultimately bound for the U.S. East Coast consumption centers. SONAR data showed a similar avoidance to mitigate the risk of disruption associated with the International Longshoremen’s Association strike.

For shippers moving containerized cargo from East Asia to the eastern U.S. consumption centers, this may more often mean utilizing the “land bridge” of rail intermodal. Import share gain among the U.S. West Coast ports typically translates to intermodal volume strength since about 70% of imports that come in through the West Coast ports are moved via rail intermodal versus 20%-25% of imports coming through the East Coast ports, according to the Intermodal Association of North America. That could lead to 2025 being another strong year for intermodal volume, which the domestic intermodal companies should be able to accommodate given their recent investments in containers.

Airfreight growth to slow in ’25, but rates may remain elevated

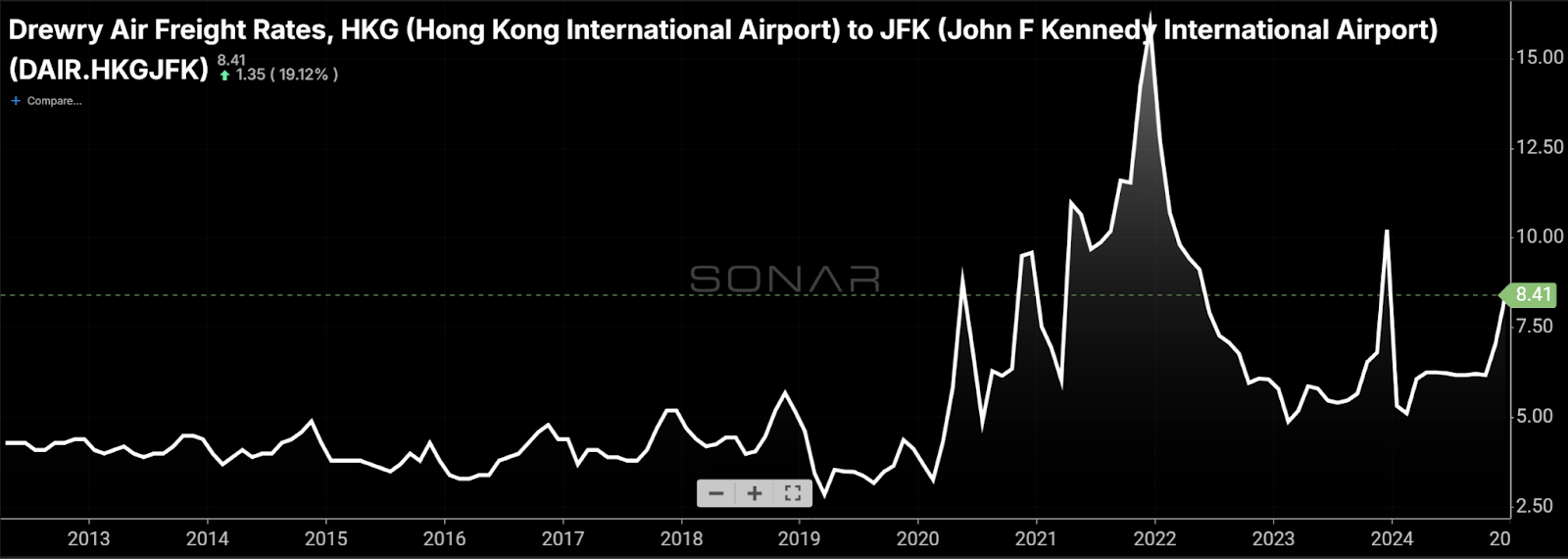

While well off their pandemic highs, airfreight rates remain elevated relative to pre-pandemic levels. (Chart: SONAR: DAIR.HKGJFK)

A recent FreightWaves article explained why air cargo volume growth will be halved in 2025. Tariffs and the potential elimination of the di minimis exemption could both hit air cargo volume. But, that outlook is not as bad as it sounds for carriers, coming off 2024, when air cargo volume grew about 12% (a rate that was enhanced by the Red Sea disruption) against a relatively easy 2023 comparison.

There is a range of expectations for 2025 volume growth. The International Air Transport Association, Xeneta, Consultancy Rotate and DSV expect year-over-year changes of +5.8%, +4%, -6% and about flat, respectively. Air cargo rates in many key lanes, such as Hong Kong to JFK, shown above, remain well above pre-pandemic levels and experienced a solid peak this year, even if it was unspectacular compared to recent years. Capacity is expected to grow in the midsingle digits next year, but as a recent Flexport webinar pointed out, comparing percent increases in demand and supply can create an overly pessimistic view of the market. Since the pandemic, available belly space in passenger aircraft has grown in leisure-oriented lanes, which are less compatible with air cargo, as opposed to business-oriented lanes, where there are now fewer flights.