Navistar International Corp. (NYSE: NAV) crushed fiscal third quarter analyst estimates, posting higher revenue, profits and market share.

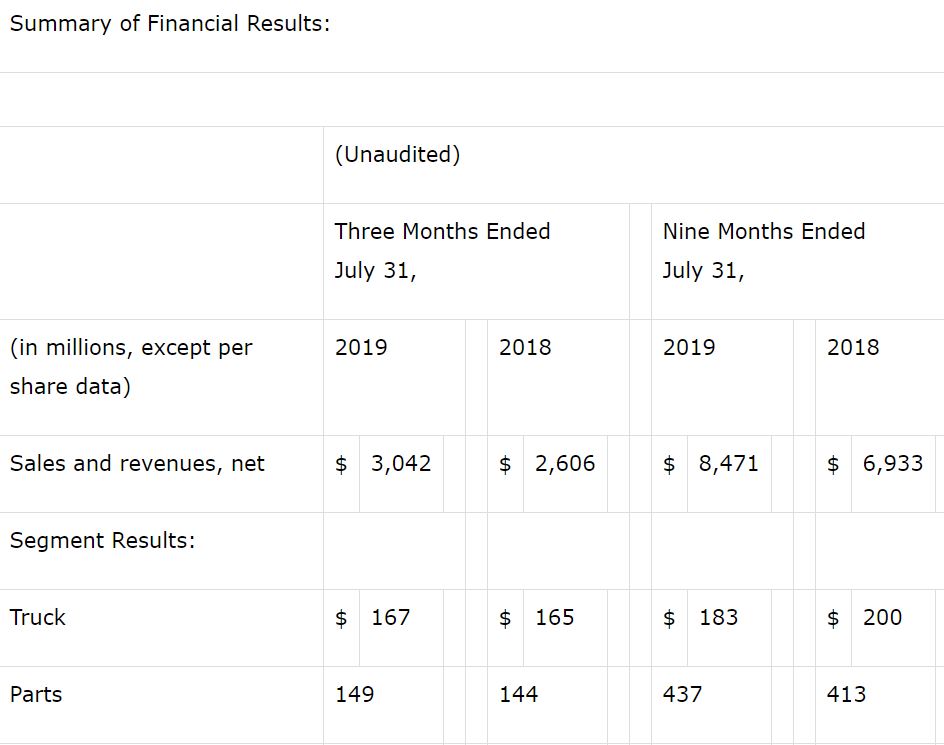

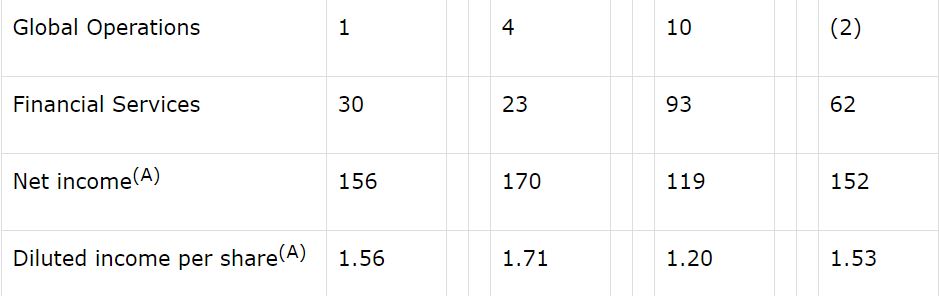

The Lisle, IL-based truck and bus maker reported net income of $156 million, or $1.56 per diluted share, compared with third quarter 2018 net income of $170 million, or $1.71 per diluted share.

Navistar said it cut line rates at assembly plants in Springfield, Ohio and Escobedo, Mexico by 15%, reversing production added through overtime and weekend shifts earlier in the year.

Year-over-year new truck orders have declined about 75 percent compared with record orders in the third quarter a year ago. The backlog of orders waiting to be built has declined 44% since peaking in October 2018.

Crushing consensus

Ten analysts who cover the company estimated earnings per share of $1.21, according to investor site Seeking Alpha. Navistar shares closed at $24.81 up 13.49% on the New York Stock Exchange (NYSE) Wednesday, September 4.

Revenues in the quarter were $3 billion, up 17% from the same period a year ago. That was primarily due to a 28% increase in volumes in sales of Class 6-8 trucks and buses in the United States and Canada. The consensus estimate for revenue was $2.92 billion.

Market share for the year, including Class 6-8 trucks and school buses, is expected to be 18.5% to 19% toward the company implied goal of 25% share by 2025.

Navistar took a “greater share of wallet” from customers who buy from several truck makers, Troy Clarke, Navistar chairman, president and chief executive officer Clarke said on a conference call with analysts.

“What we’re hearing and seeing is that we continue to improve our share of their buy,” he said. “In Class 8, we’ll continue to grow with these customers.”

As the new truck market softens heading into 2020, Clarke said Navistar is well positioned to gain additional share. Dealer inventories stand at 85 days, which is the “lower end” of the inventory range, Clarke said.

“With the (production) adjustments we’ve made, we see a stable environment through Q1 of 2020,” Clarke said.

“We think our position for next year will continue to improve even as industry volumes continue to decline,” Walter Borst, Navistar chief financial officer, said on the analyst call. “On a per-unit basis, we would look to continue growing profitability.”

Service expansion

Navistar’s partnership with Love’s Travel Stops and Country Stores and its Speedco service centers in August activated the commercial vehicle industry’s largest service network in North America with more than 1,000 outlets.

The company also opened a parts distribution center near Memphis, TN, to meet the growing demand for parts and faster maintenance turnaround times. A retail inventory management system resulted in 50% fewer emergency parts orders.

Navistar forecasts the industry will deliver an estimated 295,000 to 315,000 Class 8 trucks in the United States and Canada this year. It pegs 2020 deliveries between 210,000 and 240,000 units.

“We’ve been preparing for this (downturn),” Clarke said. “We think 2020 will be a good year for Navistar.”

Additional financials

Third quarter 2019 adjusted earnings before interest, taxes, depreciation and amortization (EBITDA) was $266 million, compared to $218 million in the fiscal third quarter of 2018.

Adjusted net income grew 55% to $147 million, compared to $95 million in the same period last year.

Navistar ended the quarter with $1.16 billion in consolidated cash, cash equivalents and marketable securities.

The company announced during the quarter it would invest $125 million in new and expanded manufacturing facilities at its Huntsville, AL, plant to produce next-generation big-bore powertrains developed with its global alliance partner Traton.

Navistar reaffirmed guidance for 2019 full-year revenues of between $11.25 billion and $11.75 billion. The company expects adjusted EBITDA to be near the midpoint of $875 million to $925 million.

“We are on course for a strong end to 2019, and we’re not standing still,” Clarke said. “The company is recapturing market share and is growing revenue, EBITDA and cash flow. We remain focused on setting ourselves up for long-term success.”