ILA and USMX come to the table

While it’s still unclear what will happen in the middle of this month, a report from CNBC noted that the two sides in the East and Gulf Coast port labor dispute are meeting, which is a step in the right direction. That is a contrast to the days leading up to the strike deadline this past fall, when it appeared to the United States Maritime Alliance (and most others) that the International Longshoremen’s Association had already decided to strike. That said, the two parties still have major differences. The union wants human workers to be added to payrolls to complement added automation/semiautomation, while the employers say that automating/semiautomating repetitive tasks is one of the methods for paying for the wage increase the parties agreed to this past fall.

For details, see these CNBC and FreightWaves articles.

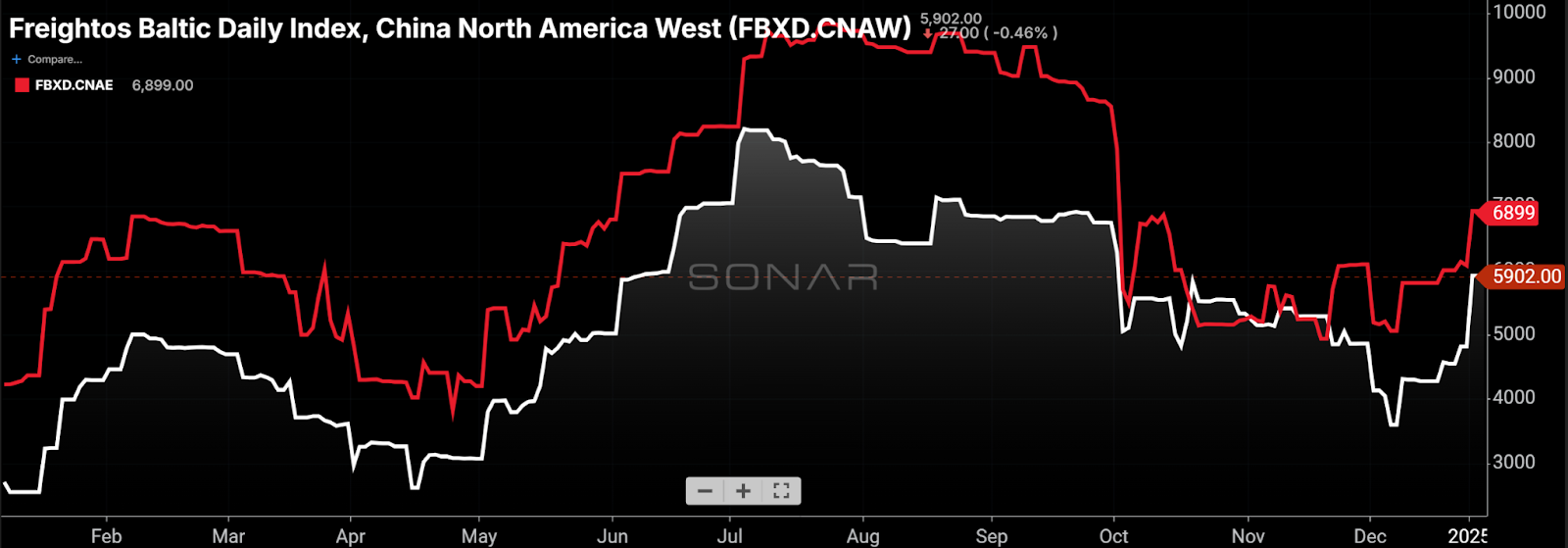

Ocean rates moving higher near term but may fall later in Q1

Trans-Pacific eastbound spot rates have risen to start the year. The spot rates to move a 40-foot container from China to the U.S. West Coast and U.S. East Coast are shown in white and red, respectively. (Chart: SONAR)

It stands to reason that containership capacity that is set to come into the industry this year and next – Flexport estimates the added capacity will total 8% and 6% of total capacity in 2025 and 2026, respectively – will put pressure on ocean rates. However, the near-term fundamentals point to higher rates in the immediate term. JP Hampstead describes why in a FreightWaves article. In short, general rate increases took hold at the start of the year combined with a volume pull-forward ahead of Lunar New Year, a potential ILA strike and higher tariffs. Drewry forecasts rates to rise further in the coming week while Freightos expects rates to decline given an expected seasonal demand decrease in late February.

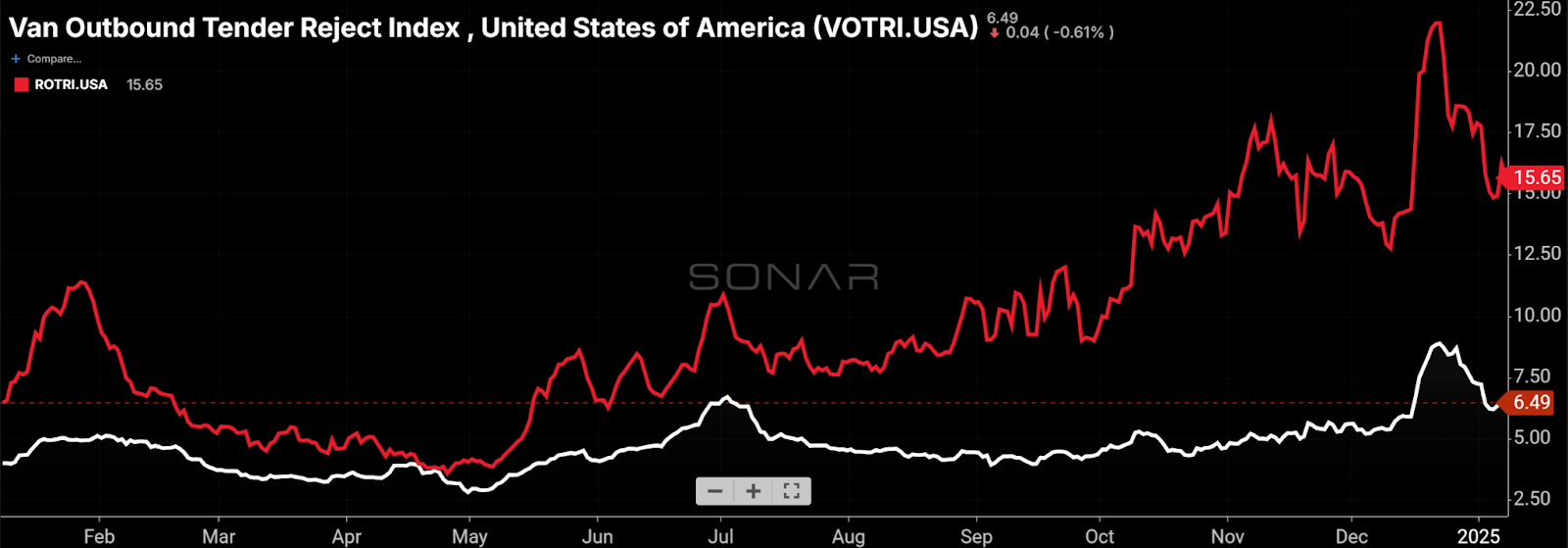

Following the holidays, truckload capacity returns to the market

Tender rejection rates for dry van (white) and reefer (red) are ahead of where they were at this time last year but have come down in the past week as capacity returned to the market. (Chart: SONAR)

The freight market still appears to be on track to become meaningfully tighter this year, but not without the impact of normal seasonality during this slow period for demand. As the first full week following the holidays progresses, rejection rates have come down from recent highs but remain higher year over year. The higher tender rejection rates, relative to one year ago, appear to be driven by capacity exiting the market given that tender volume is 7% lower compared to this time last year.

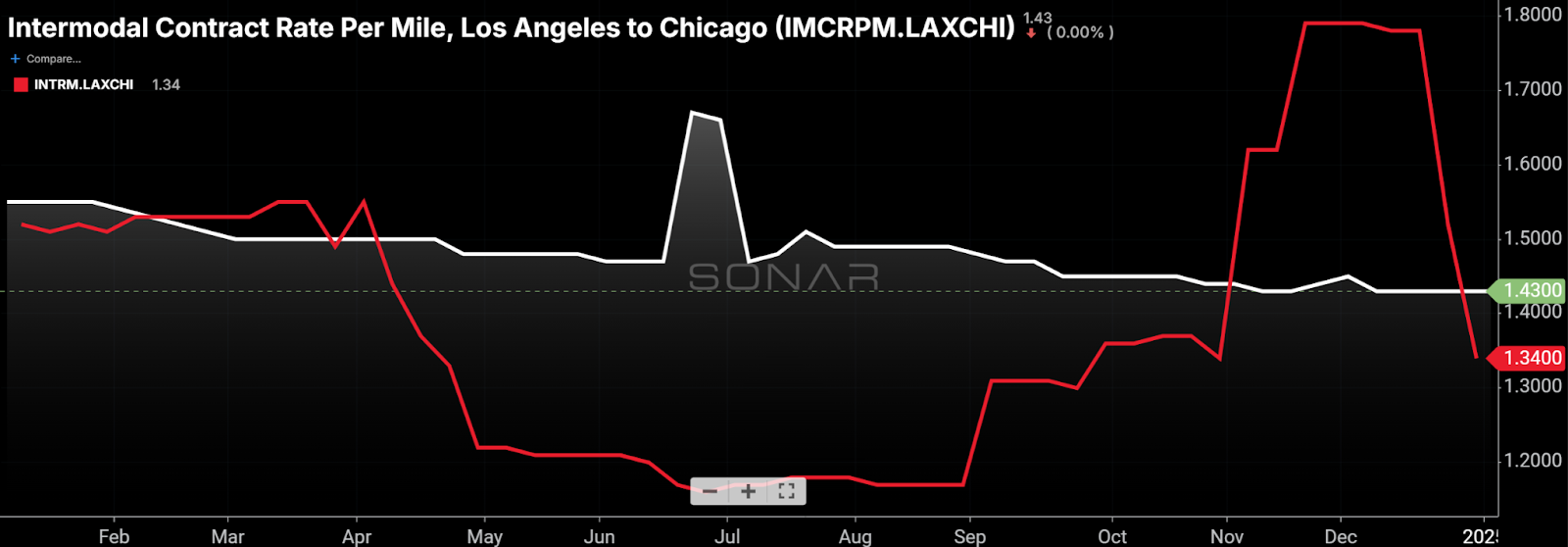

Truckload contract rates are above spot rates, on average, but that spread has narrowed the past few months. (Chart: SONAR)

Shippers can still move loads cheaper on the spot market than the contract market – SONAR shows an average difference of 51 cents per mile. But, that spread has narrowed in the past four months from as much as 69 cents a mile in late September, suggesting a market that is on the path toward tightening. In his recent article, Tony Mulvey places the Pricing Power Index at 40, meaning that pricing leverage slightly favors shippers over carriers on a 0-100 scale. Meanwhile, Zach Strickland’s Chart of the Week article argues that there would be additional evidence of a tightening market if not for shippers’ risk mitigation strategies, which include lengthening lead times and improving their inventory management practices. In addition, rail intermodal has taken share from truckload in certain long-haul corridors, especially those outbound from Los Angeles.

Intermodal spot rates have declined from LA to Chicago, the densest intermodal lane, suggesting that carriers are currently unconcerned with protecting capacity for contractual shippers. (Chart: SONAR)

The Stockout show: As e-commerce grows, so does return fraud

(Image: FWTV)

On Monday’s The Stockout show, Grace Sharkey and I tackled the growing issue of fraudulent returns. Even legitimate returns are increasingly a problem as more sellers refund the price of low-value items (say $10 or less) and instruct buyers to keep them rather than incur the cost of processing them and returning them to inventory. As e-commerce grows, so do returns – total returns represent 13% of sales; that breaks down to an 8.7% return rate for in-store purchases and a 24.5% return rate for online sales, according to Retail Dive. Recognizing the cost, retailers are giving consumers a score based on how likely they are to return an item and working behind the scenes to pass the return costs along to consumers.

In addition, a whopping 15% of returns and claims are fraudulent, with schemes that include falsely claiming porch piracy and returning stolen merchandise, among many other devious methods. Retailers lost an estimated $103 billion in 2024 to fraudulent returns, a figure that is expected to grow in the coming years unless there is successful intervention.

Watch The Stockout show here and click here for the full playlist.

For those who want a steady stream of information on freight fraud, I recommend signing up for Sharkey’s Fraud Watch newsletter here.