Dry van truckload (TL) carrier P.A.M. Transportation Services (NASDAQ: PTSI) announced second quarter 2019 earnings of $1.45 per share which was well ahead of the analysts’ expectations of $1.24. The company reported earnings of $1.55 per share excluding non-cash, non-operating losses associated with securities investments.

“We are very pleased with our financial performance for the second quarter 2019, which resulted in our best second quarter operating income on record, and the second best quarterly operating income in the company’s history,” said PTSI’s President Daniel H. Cushman.

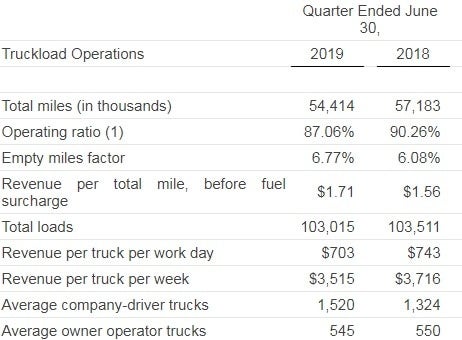

Revenue excluding fuel surcharge declined 0.5 percent year-over-year to $112.4 million in the quarter. The company added almost 200 company-driver trucks on average, which was offset by a 5.4 percent year-over-year decline in revenue per truck per week at $3,515. Revenue per total mile (excluding fuel) increased 9.6 percent year-over-year to $1.71. The TL division reported an 87.1 percent operating ratio, a 320 basis point improvement.

Management said that the operating income growth was attributable to fleet growth and improving its operating ratio to “more acceptable levels.” They made reference to a sustained period of rate increases which allowed the company to increase driver pay, recruit additional drivers and limit driver turnover.

However, it appears that the rate improvement seen in the quarter will be difficult to replicate moving forward.

“As the year has progressed, we have experienced a more balanced market than comparative periods during 2018 and have been increasingly challenged to hold customer rates at levels that cover the new ‘normal’ increased driver and owner-operator rates, and that cover various other increased costs while maintaining acceptable margins. While we have not conceded to pressure to decrease rates on existing lanes, the market has not allowed the addition of new business at similar margins that were achieved during the comparative periods in 2018,” said Cushman.

The company hasn’t seen a decline in freight demand as severe as that of other carriers. Management said that demand hasn’t been as strong as 2018, but that it has been “much better” than levels they experienced in 2016 and 2017. Northbound traffic from Mexico has benefited both its TL and logistics divisions and demand for its dedicated offering is “on par with 2018 levels.” That said, PTSI’s dedicated service is heavily tied to the automotive sector, an industry that is in decline.

PTSI’s logistics business saw an 18 percent decline in revenue to $19.5 million compared to the second quarter of 2018, but the division’s operating ratio improved 50 basis points to 93.9 percent.

Consolidated operating income increased 32 percent year-over-year to $13.2 million, but it appears that the company may not be able to hold this level. Management called out increasing costs in areas like replacement equipment, recruiting and insurance and said that margins could be challenged if demand doesn’t improve.

“Many shippers have expressed intentions of returning rates to levels seen prior to the 2018 increases. However, these increases were, in large part, passed through by many carriers, including us, to drivers and owner-operators in an effort to increase the competitiveness of the truck driving profession with other career opportunities and to increase the pool of available driver capacity. This increase combined with increases in other operating costs means that rate decreases can only be granted through giving up margin,” said Cushman.

Shares of PTSI have experienced a considerable run since its May 13, 2019 tender offer announcement that it would purchase up to 200,000 shares, 3.4 percent of the outstanding stock, at a price of $55 to $60 per share.

PTSI Stock Price Chart – SONAR