This week’s FreightWaves Supply Chain Pricing Power Index: 35 (Shippers)

Last week’s FreightWaves Supply Chain Pricing Power Index: 35 (Shippers)

Three-month FreightWaves Supply Chain Pricing Power Index Outlook: 35 (Shippers)

The FreightWaves Supply Chain Pricing Power Index uses the analytics and data in FreightWaves SONAR to analyze the market and estimate the negotiating power for rates between shippers and carriers.

This week’s Pricing Power Index is based on the following indicators:

Seasonal volume declines hit market throughout July

Seasonality reigned supreme in July as the summer doldrums arrived following the Fourth of July holiday. Tender volumes fell throughout July, which is seasonally expected, but have held on to year-over-year gains, despite the declines. The challenge for freight market participants has been where the volume growth has occurred. Over the past year, volumes in the local length of haul mileage band (<100 miles) are up 26%, while the long haul volumes (800+ miles) are down 1%.

To learn more about FreightWaves SONAR, click here.

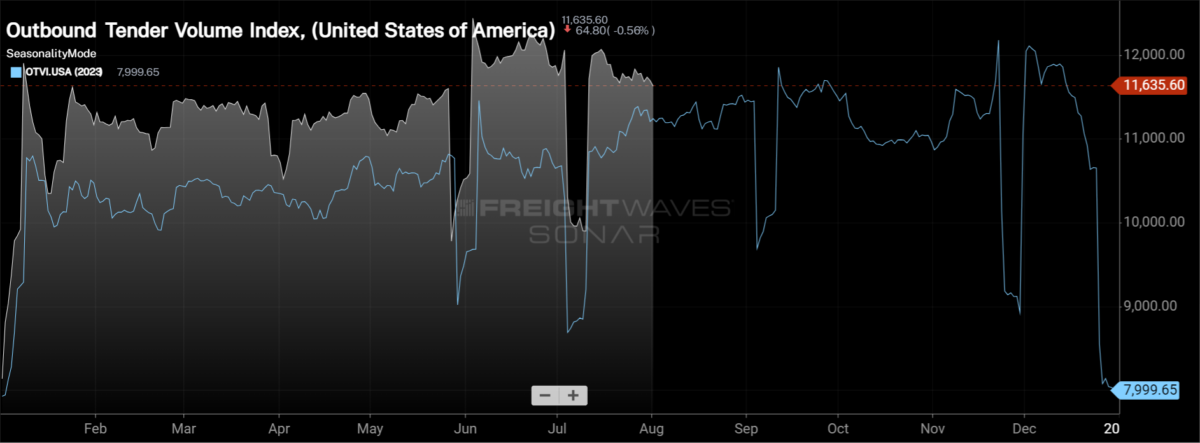

The Outbound Tender Volume Index , a measure of national freight demand that tracks shippers’ requests for trucking capacity, is 0.57% lower week over week as volume levels retreat from the recent high. OTVI fell by 0.54% during July, similar to the decline in 2022, when OTVI fell by 1.1% during the month. Even with the decline, OTVI is holding on to the year-over-year gains, currently 3.44% higher y/y.

To learn more about FreightWaves SONAR, click here.

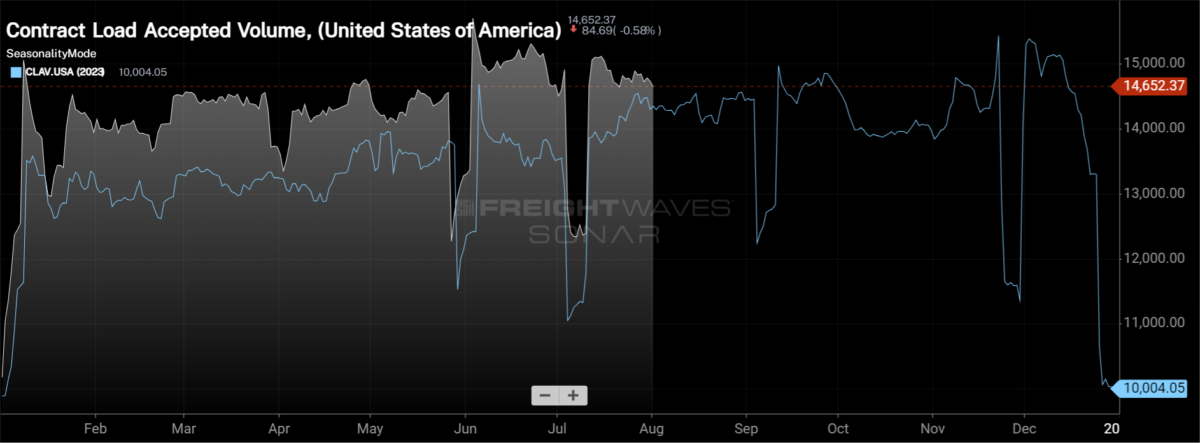

Contract Load Accepted Volume (CLAV) is an index that measures accepted load volumes moving under contracted agreements. In short, it is similar to OTVI but without the rejected tenders. Looking at accepted tender volumes, we see a decrease of 0.47% w/w, a slight improvement from last week when CLAV was down over 1% from the prior week. At present, contract accepted volumes are 2.1% above where they were this time last year, the narrowest the gap has been since November 2023.

At the Federal Open Market Committee meeting last Tuesday and Wednesday, Fed officials opted to hold interest rates stable once again. There were some changes to the statement released by the FOMC from the prior meeting, but painted a fuzzy picture on if a cut to the target range of the Federal Funds rate was likely at the September meeting. Positive inflation data for the last three months along with Friday’s underwhelming employment report lay out that a cut to the target range in September is not only possible, but likely. What could hamper that possibility is poor inflation data from July’s reading, but as of now it seems that there will be an interest rate cut in September.

Elsewhere, the consumer appears to be slowing spending. In Bank of America’s most recent credit card spending report for the week ending July 27, total card spending was up 0.1% y/y, but retail spending excluding autos was down 1.1%. Entertainment, furniture and home improvement spending remain the main sources of pressure as they were down 14.9% y/y, 10.3% y/y and 7.5% y/y, respectively. The two bright spots were: transit, up 5.8% y/y and online retail, up 5.5% y/y.

To learn more about FreightWaves SONAR, click here.

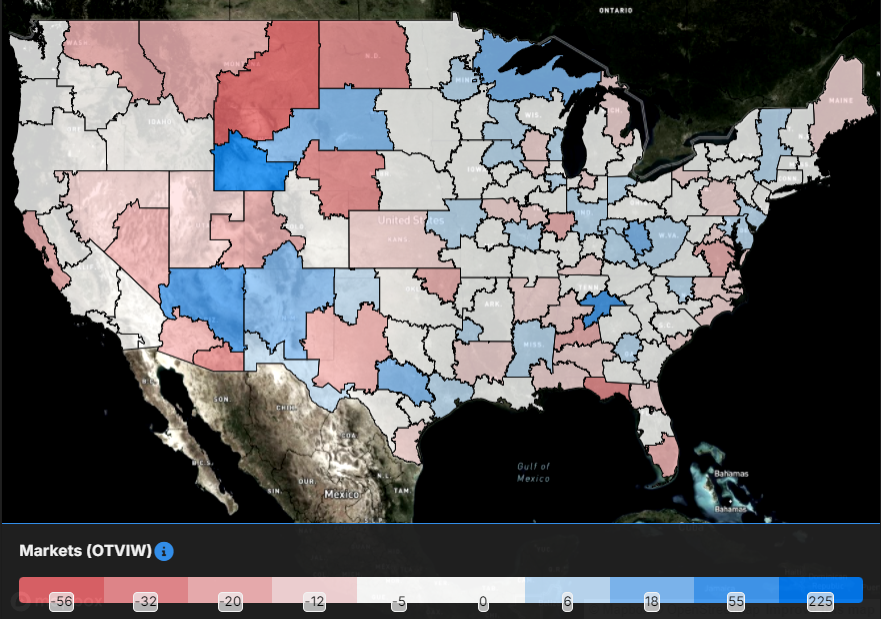

As one might expect when tender volumes decline on the national level, a majority of the markets in the country saw volumes decline over the past week. Of the 135 freight markets within SONAR, 77 experienced lower volumes week over week.

Southern California volumes continue to be a bright spot as volumes out of the Ontario market increased by 2.66% over the past week. The growth in Ontario throughout the past week was growth in tweener (451-800 miles) loads which increased by 9.54% w/w and local (<100 miles) loads which were up 16.63% w/w.

Volumes out of the Dallas market also increased the past week, rising 1.37% w/w. Similar to the Ontario market, growth really stems from the tweener length of haul as volumes grew by 7% w/w and the local length of haul as volumes were up 6.7% w/w.

To learn more about FreightWaves SONAR, click here.

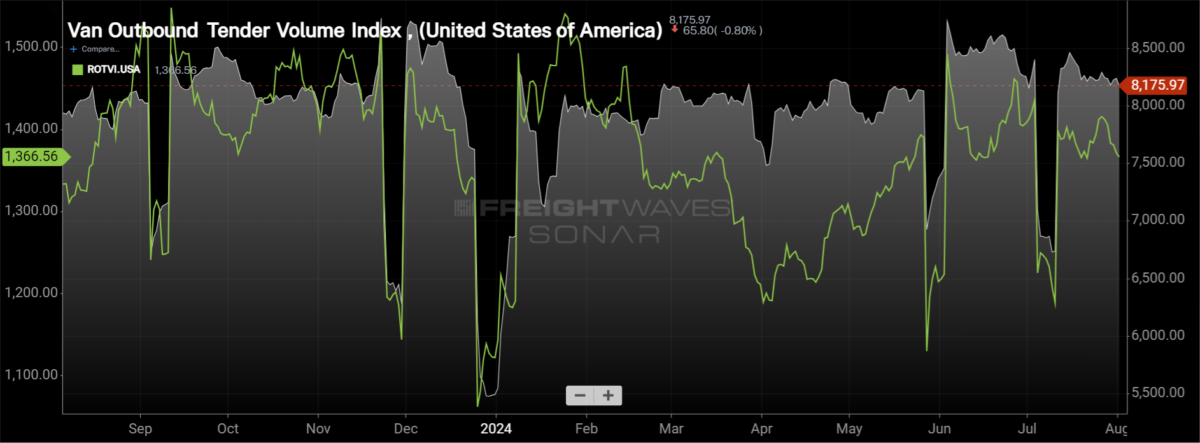

By mode: The dry van market held up in July better than the reefer market as volumes grew throughout the month. The Van Outbound Tender Volume Index increased by 1% in July despite falling by 0.68% during the past week. Van volumes are still 2.83% higher than they were this time last year.

The reefer market was challenged throughout much of July, though there was a jump in the final week of the month. The Reefer Outbound Tender Volume Index fell by 2.9% throughout July, falling 3.24% in the past week. Even with the declines, the reefer market is faring better year over year than the van market as reefer volumes are up 3.44% higher y/y.

Rejection rates flatten out to wrap July

Capacity is continuing to exit the market, but publicly traded companies are stating that the market is starting to stabilize. Werner Enterprises’ CEO, Derek Leathers, stated that International Roadcheck created a “tighter environment” and that more seasonal freight trends are appearing. The reduction in capacity is evident at the large carriers as fleet sizes are being reduced, including Werner’s one-way truckload segment which reduced its fleet by over 11% y/y.

Eyes are now on the build up to Labor Day for the timeline that would highlight the level of fragility that the freight market is experiencing.

To learn more about FreightWaves SONAR, click here.

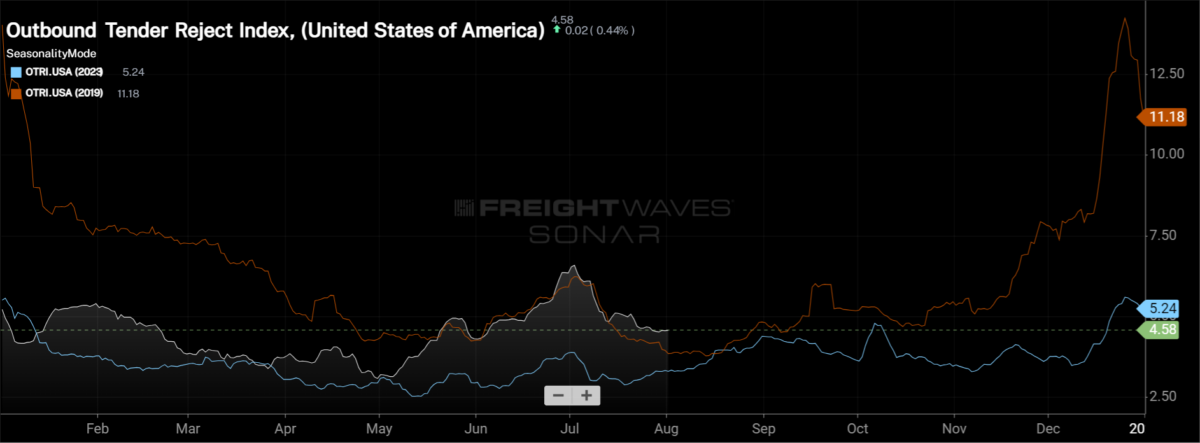

Over the past week, the Outbound Tender Reject Index, which measures relative capacity in the market, was relatively stable, falling by just 10 basis points to 4.58%. Tender rejection rates continue to trend above 2019 levels, now up 73 basis points, widening the gap from where it was just a few weeks ago.

To learn more about FreightWaves SONAR, click here.

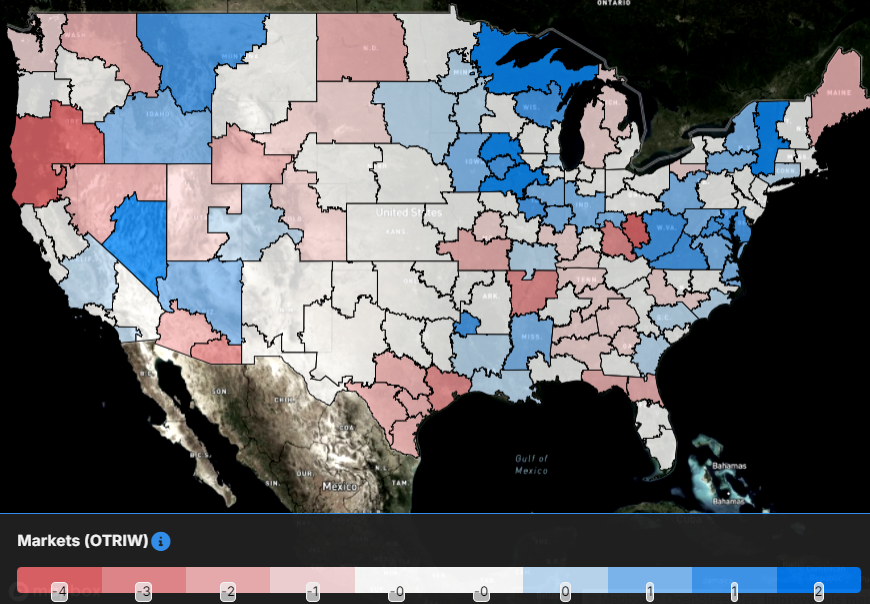

The map above shows the Outbound Tender Reject Index — Weekly Change for the 135 markets across the country. Markets shaded in blue are those where tender rejection rates have increased over the past week, while those in red have seen rejection rates decline. The bolder the color, the larger the change in rejection rates.

Of the 135 markets, 67 reported higher rejection rates over the past week, above the 45 markets which reported weekly increases last week.

The markets where rejection rates largely increased were the smaller freight markets, especially across the grain belt. With that said, the Chicago market did experience rejection rates move higher in the past week, by 40 basis points, nearly double the increase experienced in other large freight markets.

Las Vegas, Nevada experienced the largest increase in rejection rates across the country, rising 412 basis points over the past week.

To learn more about FreightWaves SONAR, click here.

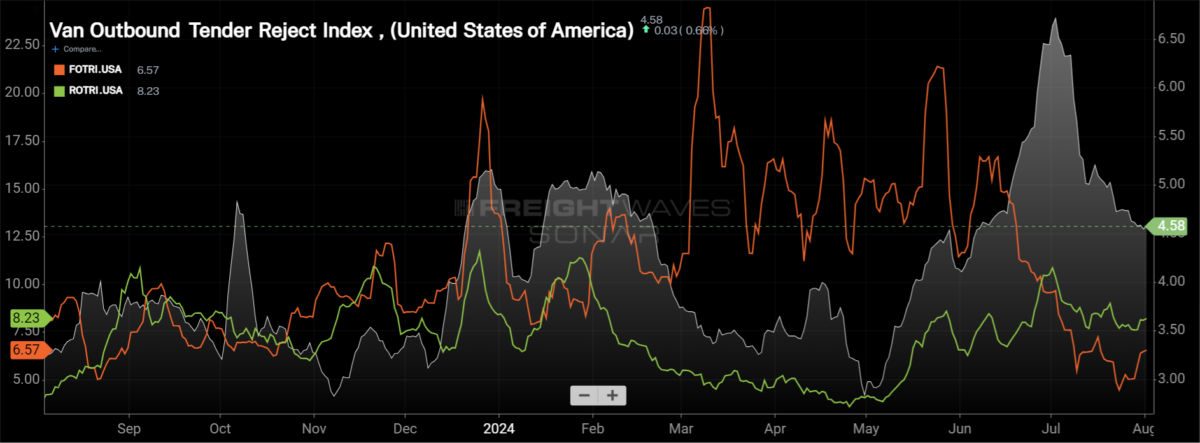

By mode: The dry van market has continued to see rejection rates retreat from the recent highs. The Van Outbound Tender Reject Index fell by 16 bps over the past week to 4.58%. In the past month, van tender rejection rates have fallen by 187 bps. Despite the declines, van rejection rates are 131 bps higher than they were this time last year.

Reefer rejection rates were fairly stable in July at levels well above where they had been throughout much of the year. The Reefer Outbound Tender Reject Index increased by 42 bps over the past week to 8.22%. Reefer rejection rates are 430 bps higher than they were this time last year.

The flatbed market remains under pressure as the industrial sector of the economy is lagging behind the consumer side. The Flatbed Tender Reject Index did increase over the past week, rising 128 bps w/w to 6.52%. Even with the increase, flatbed rejection rates are 183 bps lower than they were this time last year, highlighting the softness in the space.

Spot rates see slight bump to close July

The spot rate increases that first started during International Roadcheck in the middle of May have been strong enough to sustain throughout both June and July. This sentiment has been echoed by Derek Leathers as stated on the company’s second quarter earnings call, Roadcheck brought about “improving spot rates, and those gains have held.”

To learn more about FreightWaves SONAR, click here.

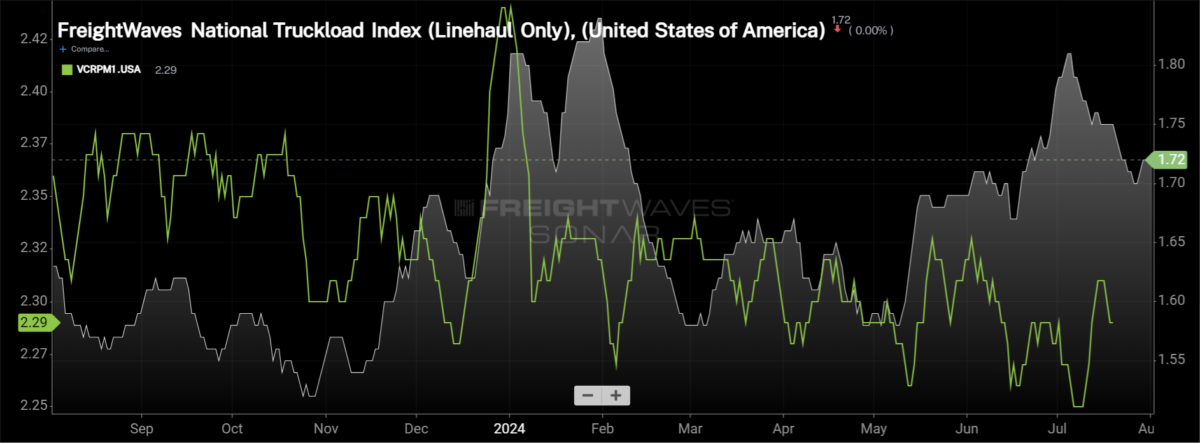

This week, the National Truckload Index — which includes fuel surcharge and various accessorials — rose by 1 cent per mile to $2.31 to close out July, 9 cents per mile off the Fourth of July holiday peak. Compared to this time last year, the NTI is up 7 cents per mile (or 3.1%). Linehaul rate declines were slightly smaller than the decline in the NTI, as the linehaul variant of the NTI (NTIL) — which excludes fuel surcharges and other accessorials — also rose by 1 cent per mile w/w to $1.72, matching the 9 cent per mile decline from the Fourth of July holiday, but 10 cents per mile higher than it was this time last year.

Initially reported dry van contract rates continue to be in a fairly tight range, remaining unchanged over the past week at $2.29 per mile. Throughout 2024, contract rates have been in the tight range, an indication that the extreme cost savings is in the rearview and service is now coming to the forefront. Initially reported contract rates are down 9 cents per mile from this time last year, about a 4% decline y/y.

To learn more about FreightWaves SONAR, click here.

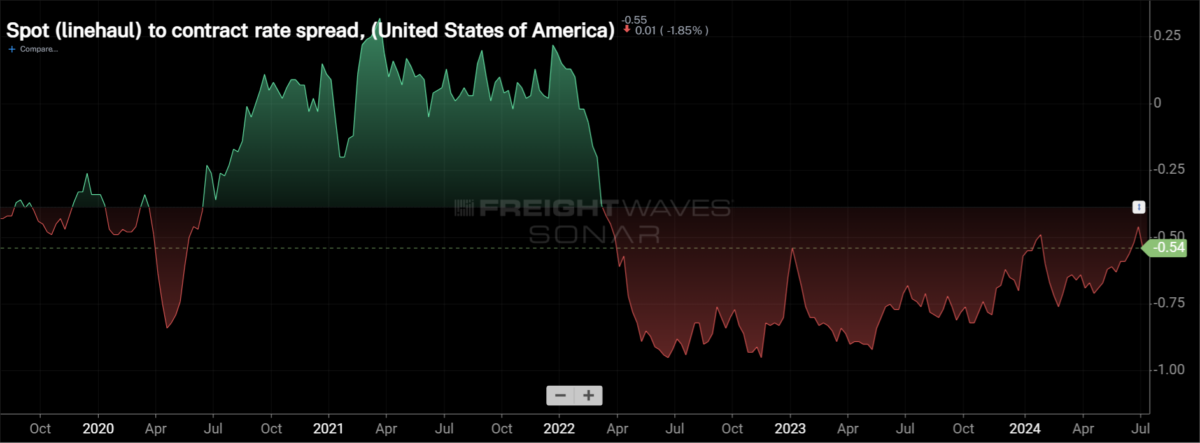

The chart above shows the spread between the NTIL and dry van contract rates is trending back to pre-pandemic levels. The recent widening of the spread is attributed to the decline off the recent highs for spot rates and a subtle bounce back in contract rates. As the spread approaches pre-pandemic levels, the market will feel tighter, especially compared to the past two years.

To learn more about FreightWaves TRAC, click here.

The FreightWaves Trusted Rate Assessment Consortium spot rate from Los Angeles to Dallas experienced a slight increase over the past week, as Southern California remains an area of opportunity for transportation providers with rejection rates above the national average and volumes growing. Over the past week, the TRAC rate along this lane increased by 3 cents per mile to $2.32 per mile, just 1 cent per mile off the recent high.

To learn more about FreightWaves TRAC, click here.

From Chicago to Atlanta, the TRAC rate also experienced a slight upward move to close out July. The TRAC rate from Chicago to Atlanta rose by 2 cents per mile, erasing last week’s decline, to $2.39 per mile, now 33 cents per mile below the contract rate.