Third-party logistics provider Radiant Logistics (NYSE: RLGT) noted strength across all of its transportation offerings on a call with analysts and investors Monday. Management said the brick-and-mortar retail segment continues to improve and that the company is even seeing some bookings for events and trade shows.

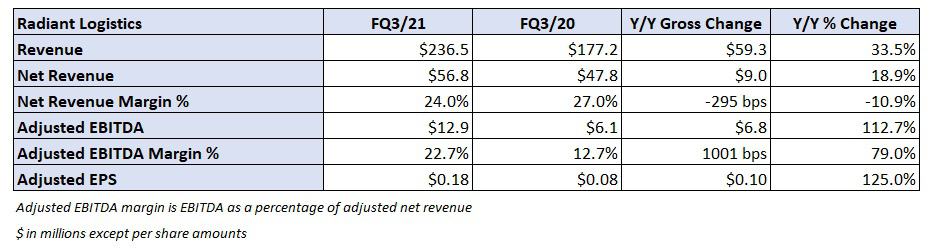

The Bellevue, Washington-based company reported record fiscal third-quarter adjusted net income of $9.1 million, or 18 cents per share, for the period ended March 31. The result was 10 cents ahead of the consensus estimate and the prior-year result.

Radiant has recorded adjusted earnings per share of 48 cents through the first three quarters of its fiscal year, nearly reaching the current full-year consensus estimate of 51 cents per share.

Founder and CEO Bohn Crain said he was hopeful that recent better-than-expected quarters would allow the company to shed its “Rodney Dangerfield of third-party logistics” moniker, a reference to Radiant’s smaller valuation multiples when compared to peers.

Shares of RLGT trade at a high-single-digit enterprise value-to-earnings before interest, taxes, depreciation and amortization multiple and a low-teen price-to-earnings multiple, compared to other nonasset and asset-light logistics providers that see EV/EBITDA multiples in the midteens and P/E multiples of 20-30x.

“We also believe that our current share price does not accurately reflect Radiant’s intrinsic value or long-term growth prospects, particularly given our unlevered balance sheet, and therefore represents an excellent investment opportunity for both the company and our shareholders,” Crain stated in the press release.

Radiant plans to use free cash flow to repurchase its stock. It has an open share repurchase authorization allowing it to buy back up to 5 million shares over the next decade. However, management said they need further clarity on the PPP loan the company received before advancing their share repurchase plan.

Management said valuation multiples on its shares make its stock more attractive than the higher multiples associated with the potential acquisition targets it has vetted. But the preferred method for using cash remains tuck-in acquisitions and agent conversions in freight forwarding, intermodal and brokerage.

Radiant reported an 18.9% year-over-year increase in net revenue to $56.8 million. Net revenue margin declined 300 basis points to 24% as spot transportation rates rose. Adjusted EBITDA more than doubled, with the margin improving 1,000 bps to 22.7%.

“We remain optimistic about the trajectory of the economy and the opportunities that it will present for Radiant. In the months ahead, we will continue to closely monitor how we and the economy are progressing and look forward to re-engaging in acquisition opportunities and/or our stock buy-back activities as the opportunities present themselves,” Crain concluded.