Chart of the Week: Outbound Tender Reject Index, National Truckload Index (linehaul only) – USA SONAR: OTRI.USA, NTIL.USA

The national Outbound Tender Reject Index (OTRI), which is the rate at which truckload carriers turn down requests from customers to move their freight, pushed over 10% for the first time since April 2022 during the Christmas holiday. Spot rates (excluding the estimated cost of fuel) also peaked nearly 10% higher than in 2023.

While this is further evidence that enough capacity has come out of the market to make it noticeably more uncomfortable for shippers, it could be much worse from a transportation management perspective.

The truckload market can typically be measured by its peaks and troughs when looking at tender rejection rates. Seasonal swings define the market, but seasonality has been challenging to find since the pandemic due to extreme under- and oversupply of capacity.

As the truckload market emerges from one of the longest periods of extreme oversupply, seasonal peaks are becoming more noticeable, Christmas being the highest among them.

Last Christmas, the OTRI topped out at 5.6%, a figure that characterizes a relatively easy transportation sourcing environment. This means shippers would have trouble finding a truck for one in every 18 loads.

During the pandemic years, the OTRI hovered above 20% for nearly 18 months. This means the transportation managers are having to navigate sourcing problems about one in every five loads. That is quite a bit of extra work.

While the current market is still a far cry from where it was two years ago, it is continuing to transition away from the easiest of sourcing environments and becoming more erratic. The increasing volatility may be the more challenging component as shippers can plan for seasonal swings but still have trouble with estimating the magnitude.

Shippers have been employing strategies that mitigate their exposure to increasing transportation market volatility.

Increasing lead times, the amount of time between the initial request and requested pickup date, has been an ongoing trend even as the market has been relatively loose. Shippers are giving about half a day more notice to carriers on average than in 2019.

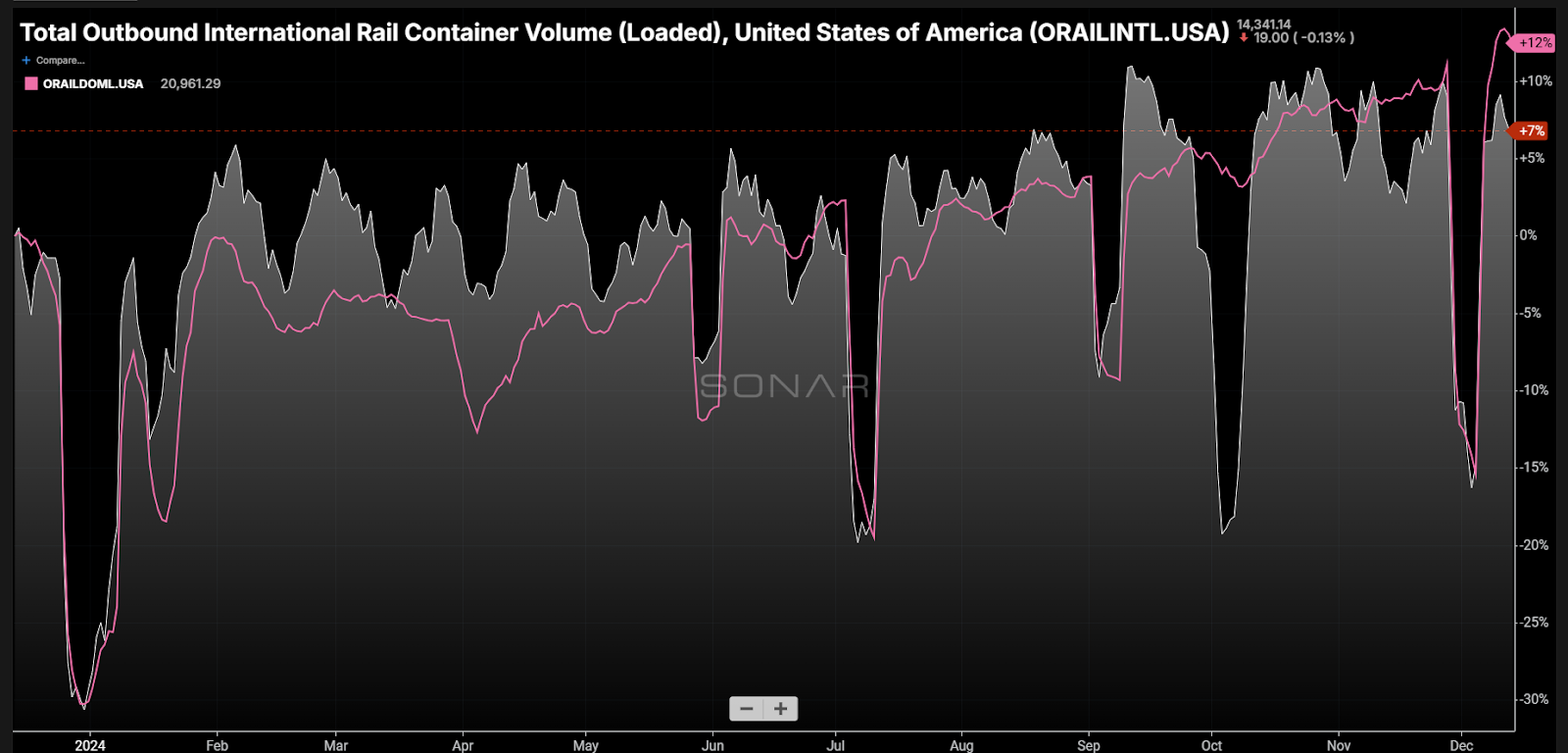

Intermodal has regained favor with the shipping community, with domestic-size containers (ORAILDOML) averaging over 10% higher y/y this past December. International containers (ORAILINTL) are staying on trains and moving inland with more frequency, which has also taken pressure off West Coast trucking capacity since this summer.

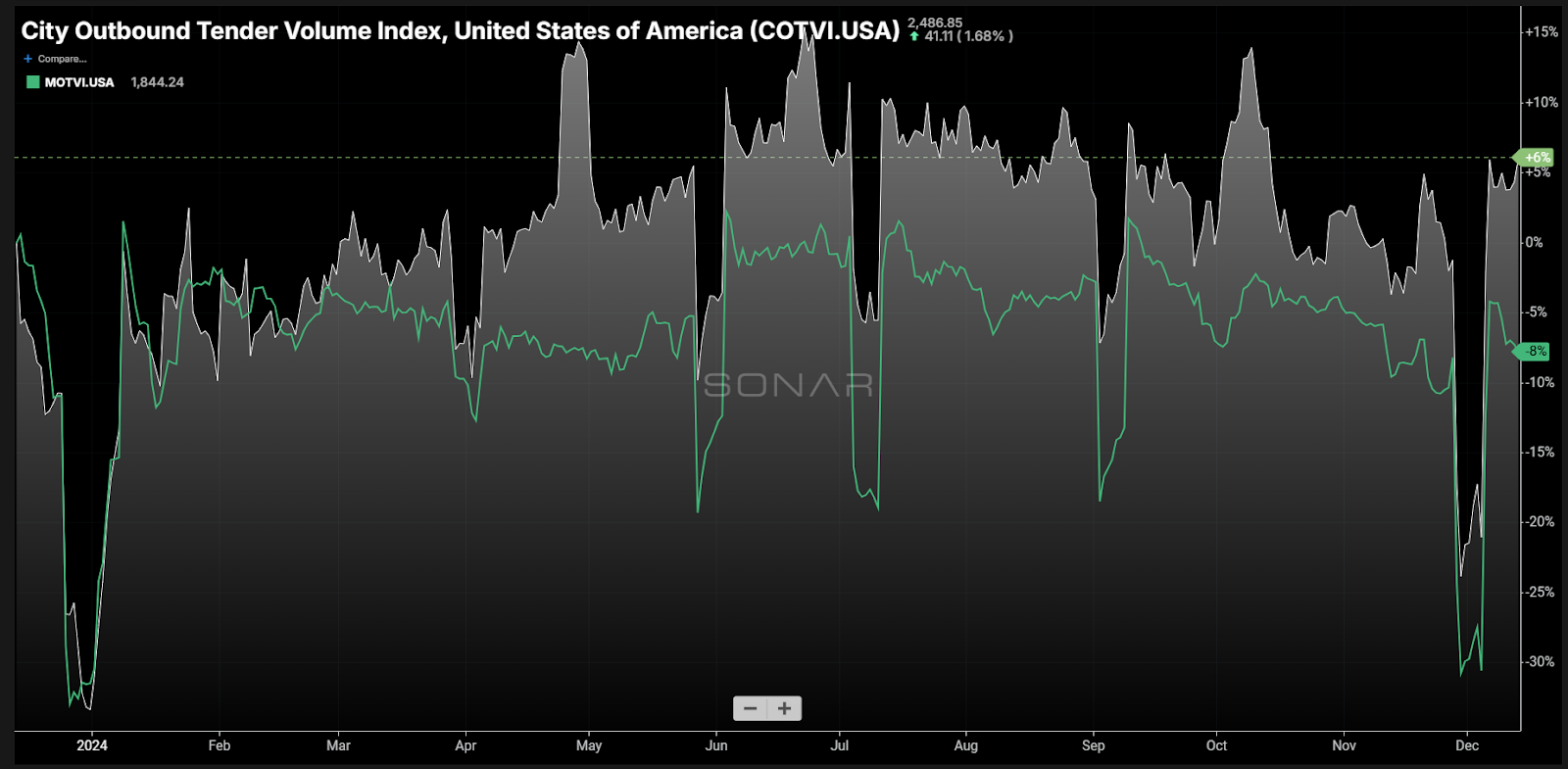

Inventory management practices have evolved, eliminating a lot of the distance between warehouses and consumers. In the weeks leading into Christmas, middle (MOTVI) haul loads, moving 250 to 450 miles, were down 8% y/y while local (COTVI) haul loads, moving less than 100 miles, were up 6%.

A blend of just-in-time at downstream warehouses and just-in-case at upstream facilities has become more prevalent as supply chains have endured an onslaught of increasing geopolitical risk since 2020.

It is challenging and time-consuming to shift manufacturing facilities and sources, but it is easy and relatively cheap to hold goods in remote locations away from city centers.

Even with all of these mitigating factors, the trucking market has become more responsive. This is due to the fact that all of these strategies, save for lead time, remove demand from the market.

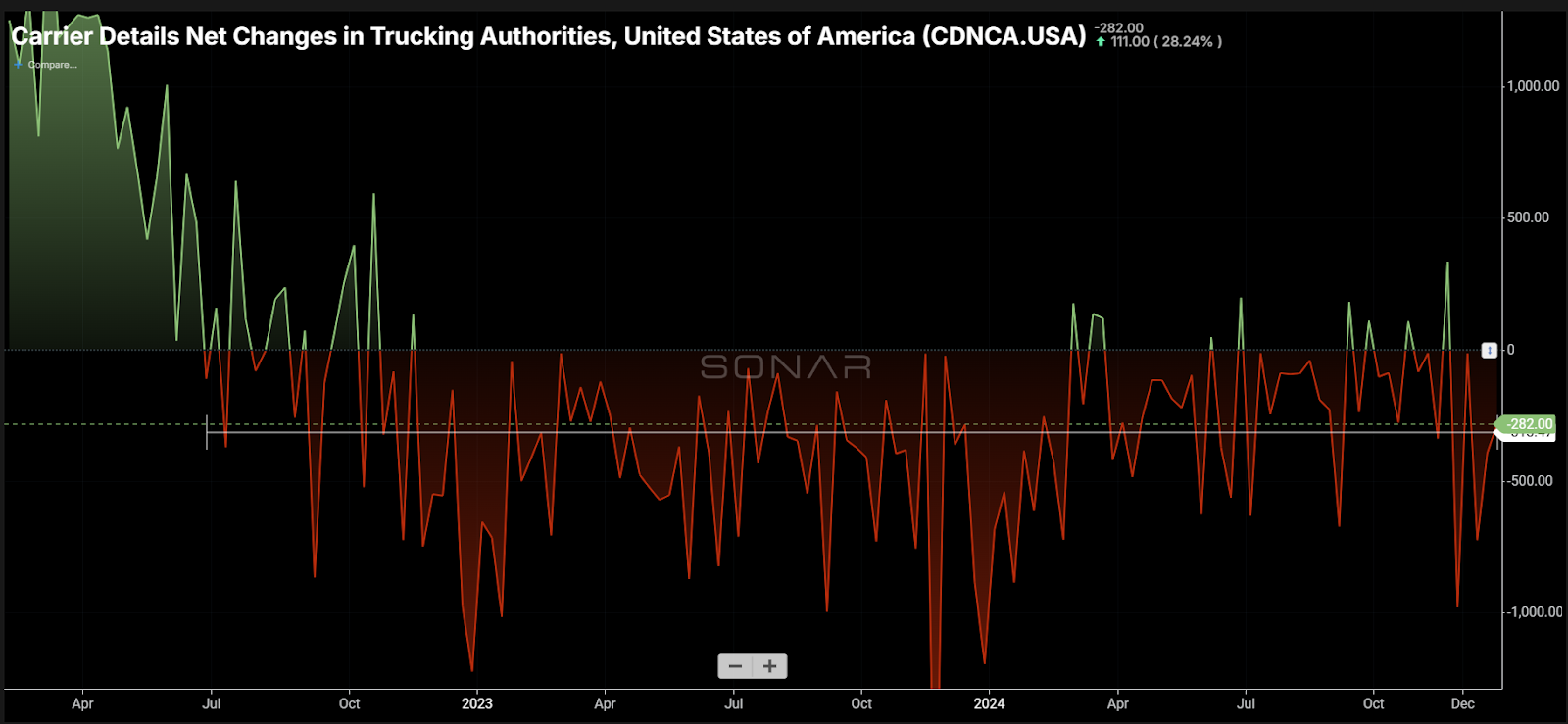

Extreme demand deficiency in relation to the supply of capacity has led to a record number of carrier exits, roughly netting 41,000 fewer carriers since July 2022, according to Carrier Details analysis of Federal Motor Carrier Safety Administration data.

If shippers had fallen back purely to a pre-COVID supply chain management strategy, the truckload market would have been in chaos over the holiday season. Many of these strategies are only making the market transition to a tighter state more manageable, which is a good thing for all. With capacity still bleeding off at record levels, what has become never-ending economic uncertainty and geopolitical instability, supply chain and transportation managers will have their work cut out for them in 2025.

About the Chart of the Week

The FreightWaves Chart of the Week is a chart selection from SONAR that provides an interesting data point to describe the state of the freight markets. A chart is chosen from thousands of potential charts on SONAR to help participants visualize the freight market in real time. Each week a Market Expert will post a chart, along with commentary, live on the front page. After that, the Chart of the Week will be archived on FreightWaves.com for future reference.

SONAR aggregates data from hundreds of sources, presenting the data in charts and maps and providing commentary on what freight market experts want to know about the industry in real time.

The FreightWaves data science and product teams are releasing new datasets each week and enhancing the client experience.

To request a SONAR demo, click here.