The Stockout Show: Election special

(Image: FWTV)

On Monday’s The Stockout show, I discussed what the election results could mean for the retail and CPG industries. For those who prefer to read, FreightWaves’ Caleb Revill summarized it well. On the show, I went through four major issues: tariffs, taxes, the Federal Trade Commission and food regulations. Producing the show one day before Election Day, I also speculated on how the CPG and retail industries might vote based on their presumed self-interests in those issues.

The outcome of the election made the show more relevant since President-elect Trump was more of a change agent. In particular, the retail industry is wary of Trump’s tariffs, and the CPG industry is wary of a Trump administration overhauling the food and medicine industries by granting widespread power to Robert F. Kennedy Jr. In addition, the FTC could look much different, resulting in more leniency on mergers.

See Monday’s show here or check out the full The Stockout playlist here.

Proposed tax cuts expected to boost freight demand

For a discussion of why, check out last week’s State of Freight election special or Tuesday’s article written by Revill and John Gallagher. In short, tax cuts at both the personal and corporate levels should result in more economic activity. In addition, if tariffs have the intended effect of boosting domestic manufacturing, that production often involves numerous transportation points of handling in the supply chain. That contrasts with imported goods, which typically arrive finished.

LTL carrier Old Dominion Freight Line (NASDAQ: ODFL) is one of many freight carriers bouncing in Wednesday’s trading as the broad indexes also rise. (Chart: Yahoo! Finance)

Ocean rates should continue moderating from the currently elevated levels

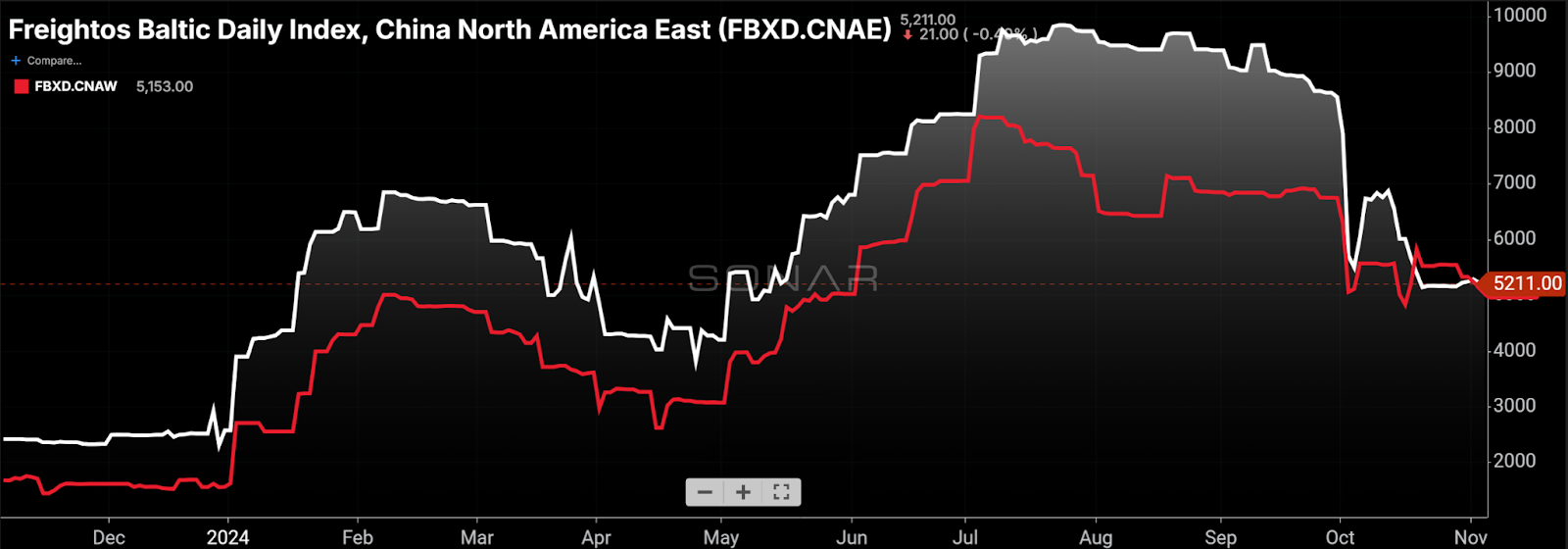

Trans-Pacific ocean spot rates from China to the U.S. East Coast and U.S. West Coast are shown in white and red, respectively. On its webinar, Flexport described the recent volatility in inbound U.S. ocean rates as “extreme” and acknowledged how unusual it is that these rates are roughly at parity. The China to U.S. East Coast lane is typically about $1,000 per container higher than the China to U.S. West Coast lane. But, it did not offer an estimate on when the spread might return to the historical average. The rates for both trans-Pacific lanes appear set to decline next year, with capacity likely to increase faster than demand. (Chart: SONAR: FBXD.CNAE, FBXD.CNAW)

Barring something unexpected happening in ocean demand, ocean capacity is set to increase faster than demand in the coming years. That was one of the primary messages from Flexport’s Oct. 31 webinar. The company is expecting the supply of ocean capacity to grow by 8% in 2025 followed by an additional 6% increase in 2026 due to vessel additions to fleets. If carriers were to again fully utilize the Red Sea, the effective capacity deployed would increase much more. Meanwhile, demand is expected to grow by about 3% annually, which would be roughly in line with to slightly above growth rates of global GDP. I believe the election results and more protectionist trade policies create risk to that demand expectation, potentially creating another factor to pressure rates.

Other takeaways from the Flexport ocean webinar include:

- CMA CGM has announced it will return to the Red Sea and Suez Canal – see routing here. The French carrier seems to view risk differently from the rest of the industry, which continues to avoid that area. Shippers with containers going through the Suez should opt for comprehensive general average insurance rather than standard insurance.

- If carriers were to return to the Red Sea en masse, schedules would be in flux, making it difficult for carriers to manage capacity via blank sailings. That could send rates plummeting.

- Carriers’ avoidance of the Red Sea changes seasonal shipping patterns given the longer sailing times and increased lead times. Therefore, expect the impact of Chinese New Year to come early this year.

Hub Group expects intermodal rates to rise

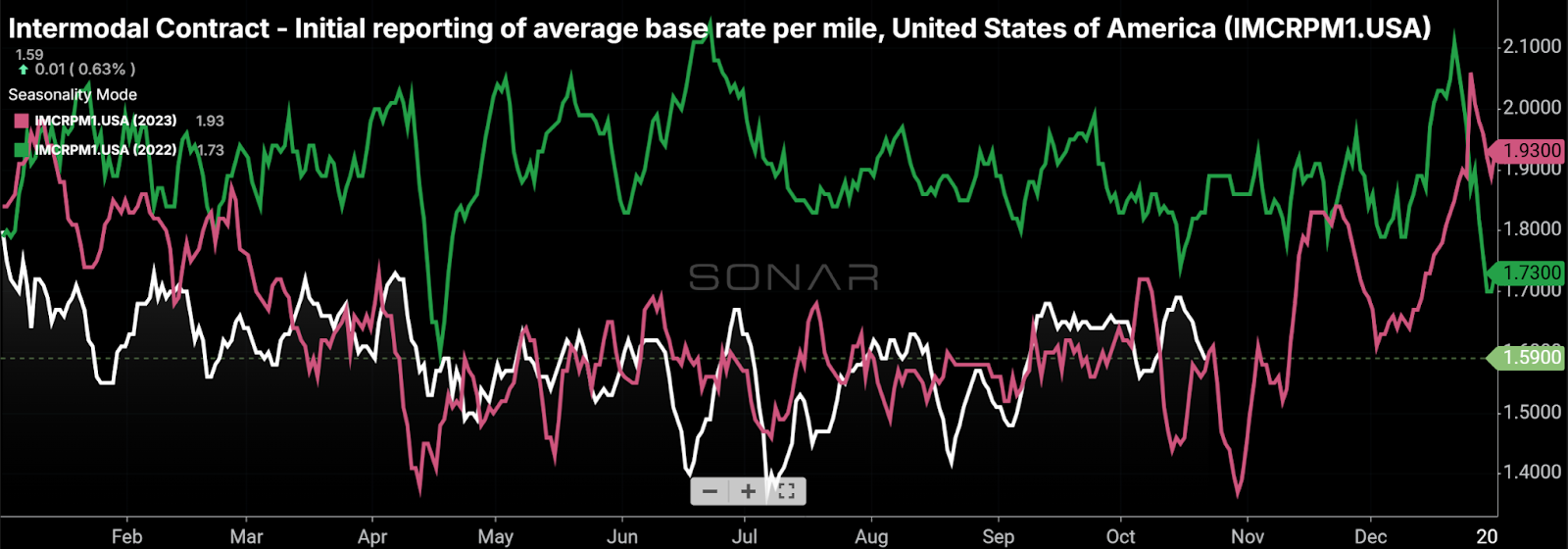

A national index of intermodal contract rates in SONAR shows rates trending roughly in line with year-ago levels. (Chart: SONAR)

When multimodal carrier J.B. Hunt reported earnings in mid-October to start the third-quarter earnings season, its management sounded optimistic on the upcoming bid season, highlighting service levels and the capacity that the carrier is able to provide. Similarly, its competitor Hub Group expressed confidence on its own analyst call last week that intermodal contract rates will rise. In response to an analyst’s question, Hub’s management described pricing as “competitive, but rational” and said it expects rates to rise with a magnitude that is not yet clear. The carrier also mentioned that it has seen disruptions in international intermodal service levels, which should help domestic intermodal volume.

For more detail, see Noi Mahoney’s writeup here.