Dreamstime

by FreightWaves’ Chief Economist Ibrahiim Bayaan

Economic data from the goods side of the economy showed some signs of life in May, as growth in retail sales and industrial production exceeded expectations during the month. This is an encouraging sign that activity may be stabilizing in the second quarter, though details in manufacturing point to some struggles.

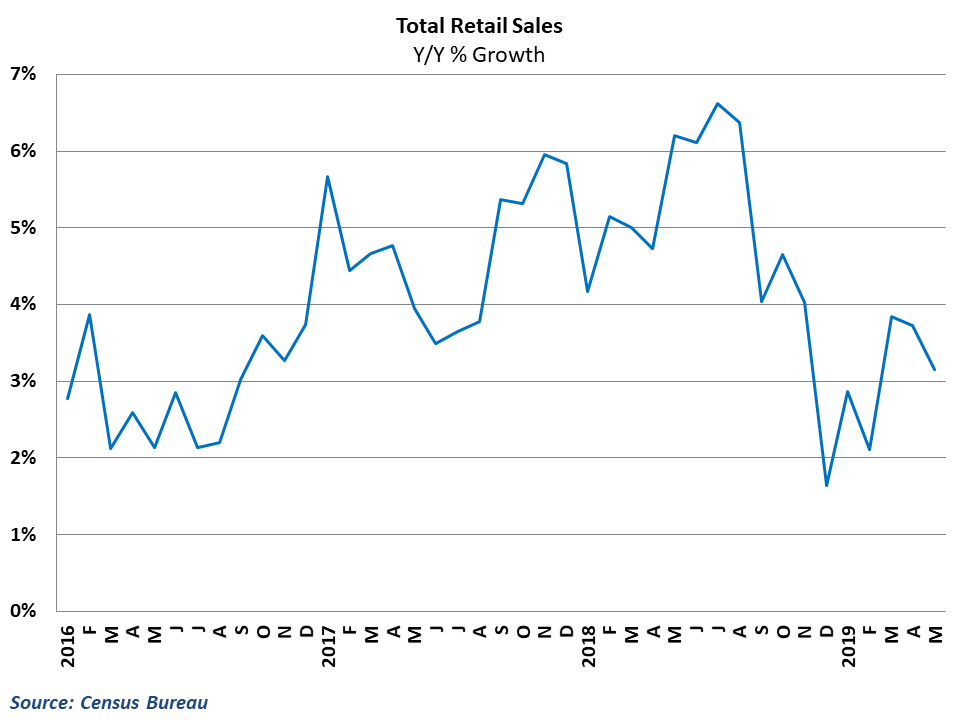

The Census Bureau reported that total retail sales rose 0.5 percent in May from April’s levels. This beat consensus estimates of a 0.3 percent gain, and marks the third consecutive monthly increase in retail spending. In addition, results from the previous month were revised up to 0.3 percent from initial reports of a 0.2 percent decline. Year-over-year growth in the retail sector slipped to 3.2 percent in May, however, driven by tougher comparisons to last year.

Retail growth was generally broad-based during the month, as sales in 11 of the 13 major industries in the sector saw higher sales in May. Big gains in sales at nonstore (mostly online) retailers, sporting goods stores and auto dealers helped lead the way during the month, with only food & beverage stores and miscellaneous retailers reporting declines. Core retail sales, which exclude auto and gasoline purchases, also rose 0.5 percent in May with year-over-year growth of 3.2 percent.

This serves as encouraging news for the economy going forward, particularly as it relates to trucking and parcel demand. Most of the goods movements between warehouses and retail locations occurs by either truckload, less-than-truckload, or parcel shipments, and May’s healthy results and April’s revision paints a healthy picture of the retail sector after a difficult first quarter of the year. Growth has still clearly shifted into lower gear after impressive growth in the second and third quarters of 2018, but appears to have stabilized in recent months.

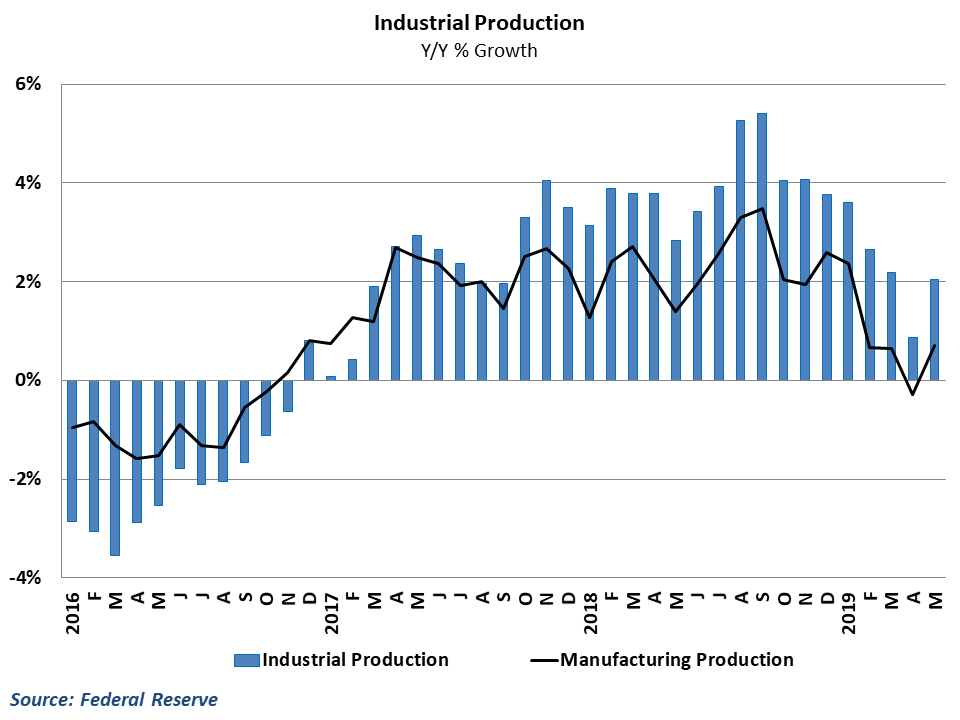

In the industrial sector, total production also surprised on the upside, rising 0.4 percent from April’s levels. This marks the largest monthly increase in industrial output of 2019, effectively erasing the decline in the previous month. Year-over-year growth improved to 2.1 percent in May, after dipping below 1 percent in the previous month.

Growth during the month was helped by a surge in utility production, which rose 2.1 percent in May. Manufacturing industrial production, which excludes mining and utility production from the total, rose by a more modest 0.2 percent. This was the first monthly gain in the manufacturing sector of 2019 and pushed year-over-year growth back into positive territory at 0.7 percent

Unlike the retail sector, there was still a good deal of weakness in manufacturing in May, with nearly half of the major industries in the sector reporting declining output. Growth during the month was propelled by an outsized gain in auto production, which surged 2.4 percent during the month. Excluding motor vehicles and parts, manufacturing activity was flat in May, including sizeable declines in primary metals and apparel production. This would suggest that the manufacturing sector still faces some significant challenges despite the generally encouraging result.

Behind the numbers

On the retail side, the May results and April revision were quite positive, and suggest that consumer spending on goods will give a solid boost to GDP growth in the second quarter. Retail went through some struggles early in 2019, as abnormal weather and a disappointing tax return season likely contributed to the erratic spending behavior during the first quarter. However, the labor market remains generally tight despite May’s disappointing employment report, and wages are still rising at a healthy clip. As a result, retail is likely to continue to grow at a solid pace going forward.

The view from the industrial sector is far less rosy, however. Even with May’s solid performance, total industrial output is still down close to 1 percent year-to-date in 2019. Moreover, since most of the gain during the month was concentrated in utility production – which is usually a temporary fluctuation – and an outsized surge in auto production, the fundamentals for manufacturing and industrial output still look quite shaky. Improved consumer demand is helping to sustain domestic manufacturing activity, but the sector still faces challenges from weakened export demand and struggling business investment. As long as these headwinds remain, manufacturing growth is going to stay subdued in the economy.