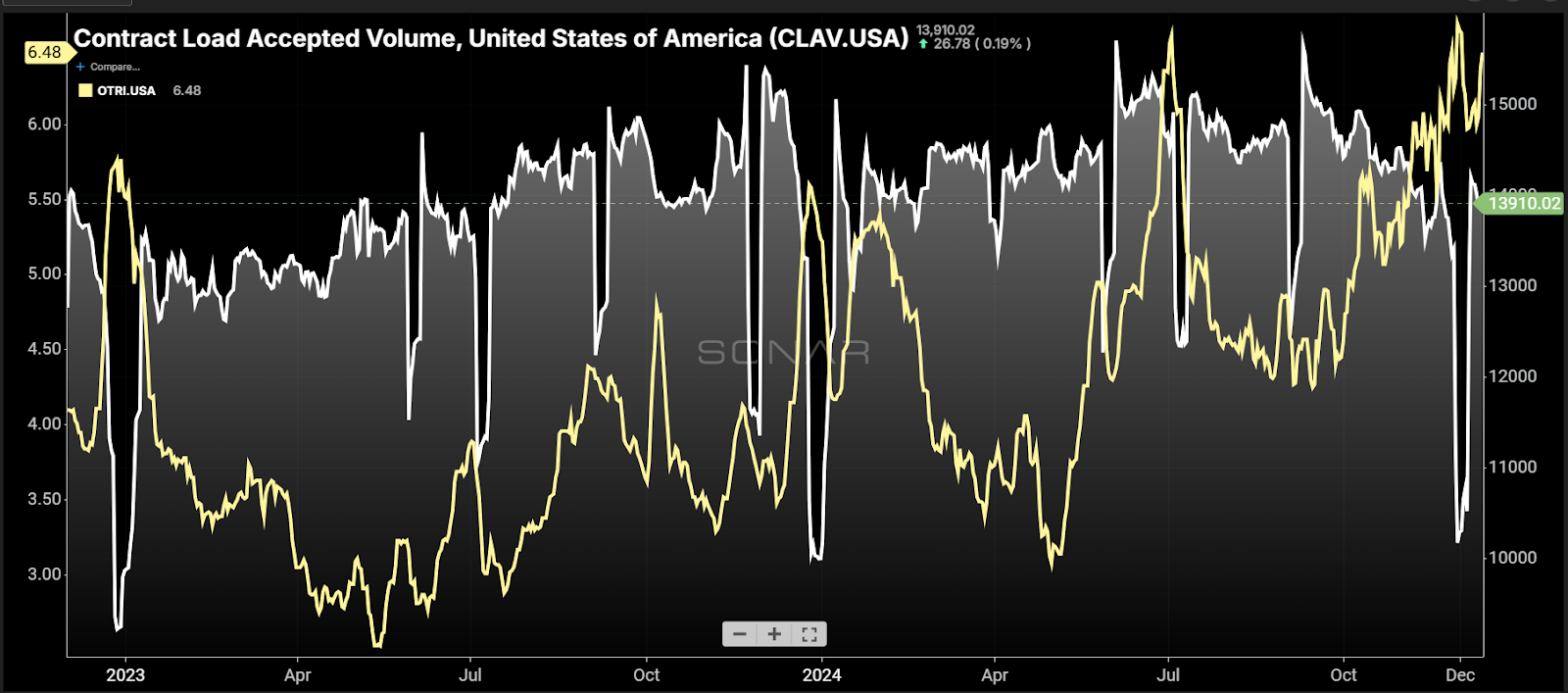

Chart of the Week: Contract Load Accepted Volume Index, Outbound Tender Volume Index – USA SONAR: CLAV.USA, OTRI.USA

Carriers are accepting the same load volumes that they were in April 2023, near the theoretical floor of the freight market’s recent recessionary period. Rejection rates (the rate at which carriers turn down load coverage requests from contracted shippers) are more than double what they were at the time. This is further evidence that a significant amount of supply has left and is continuing to leave the domestic truckload market.

The Contract Load Accepted Volume index (CLAV) is a measure of accepted load tenders from shipper to carrier. It differs from SONAR’s Outbound Tender Volume Index (OTVI) in that it does not count tenders that carriers rejected. More rejections mean it is more challenging to procure truckload capacity. When comparing the Outbound Tender Reject Index (OTRI) to the CLAV, we can approximate how balanced the supply and demand curve is in the truckload market by looking at periods of similar accepted volumes and comparing rejection rates at those times.

In May 2023, the CLAV had a value of 13,951 while the OTRI was 2.92% – basically carriers were automatically accepting loads without discrimination. Last Thursday, the CLAV was at 13,910 while the OTRI hit 6.48%. While not all loads are created equal, the average lengths of haul were also similar between the two periods. Seasonality is a factor, but the trends are the main tell.

Accepted volumes trended lower from early September until November before flattening. Rejection rates have been increasing since early October, rising from about 4.5% on Sept. 29 to 6.5% on Dec. 12.

This rise is more than your typical seasonal spike driven by holiday capacity reduction. The only year that rejection rates increased steadily during this period was 2019. In every other year outside 2019 and the current one, rejection rates are either flat or declining heading into the Thanksgiving period.

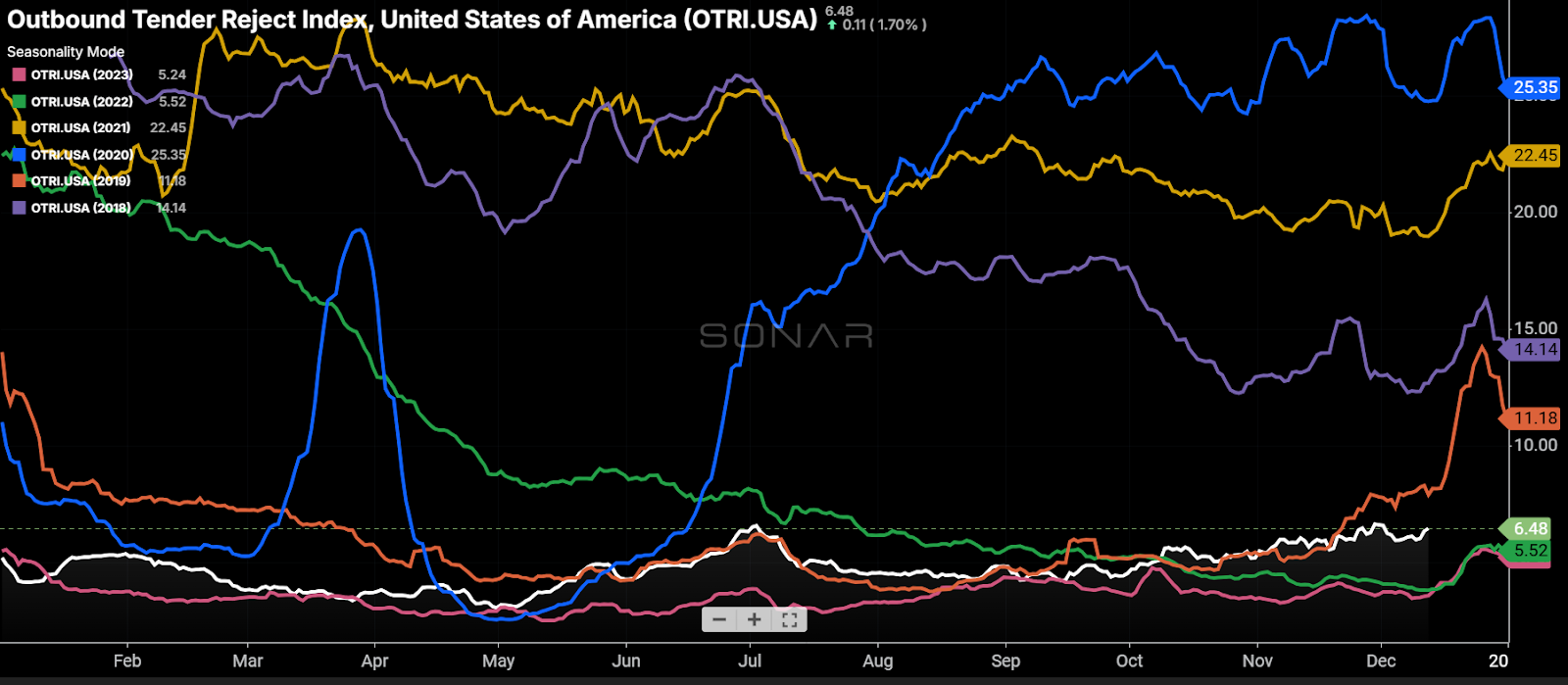

Looking at the historical OTRI figures from the past seven years, a downward trend is present in most. This aligns with a bit of a slide in demand coming out of the Labor Day weekend surge.

Still missing from the current year’s OTRI is the Thanksgiving week spike, which has been muted the past three years. But the upward trend in rejections is a new development, especially considering it does not appear to be driven by a demand-side event.

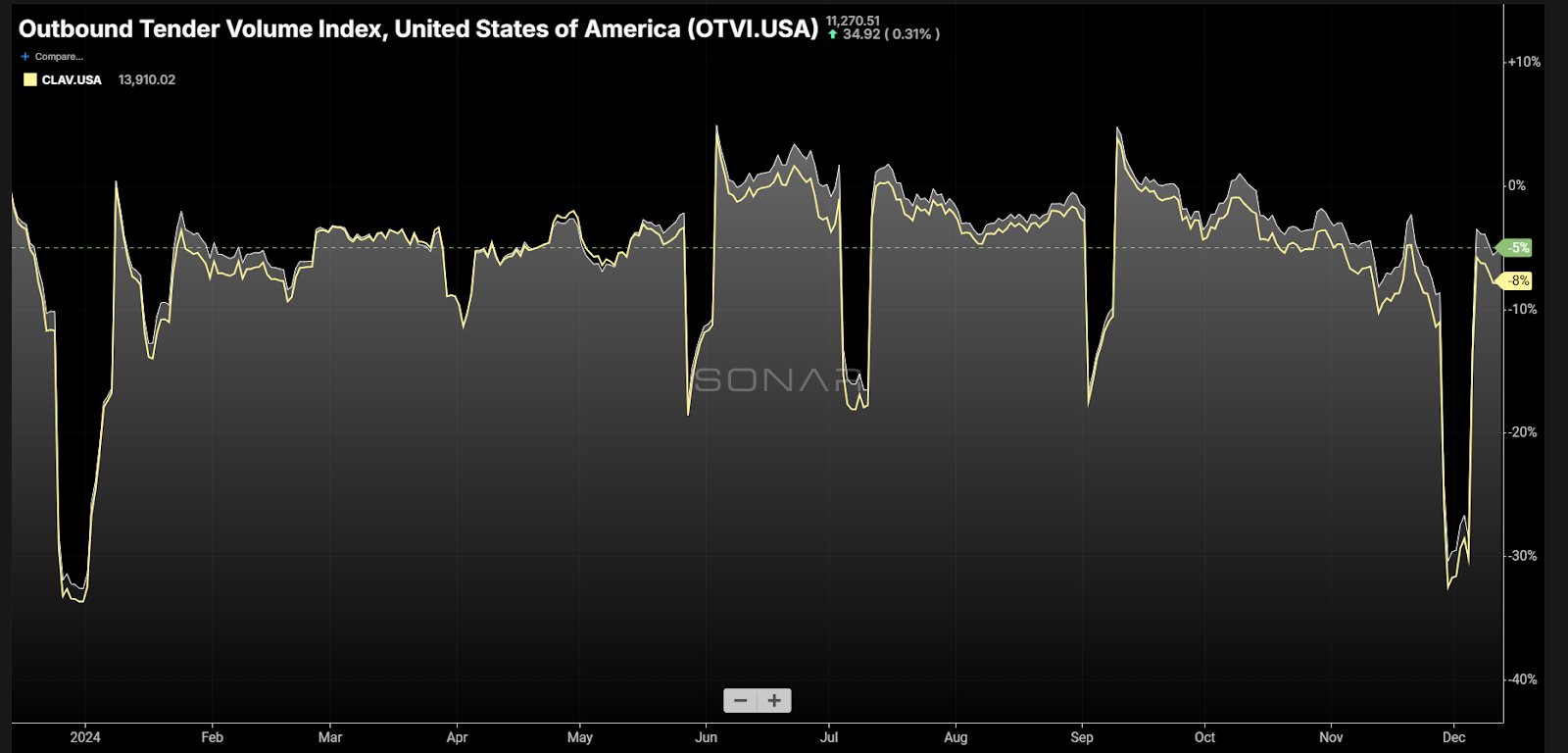

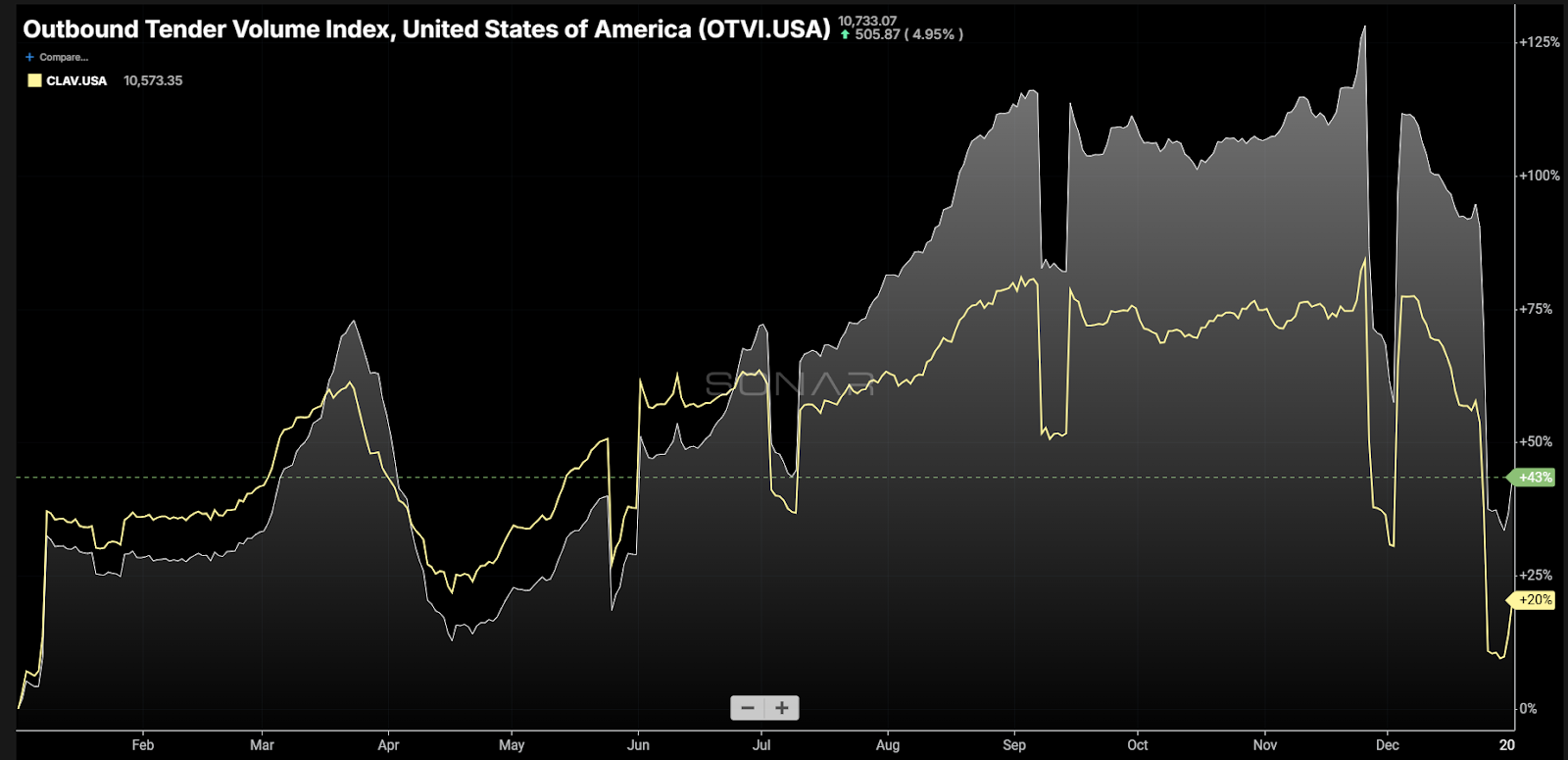

Comparing the OTVI (total tenders) and CLAV (accepted tenders) over the past year, the gap is steadily growing. This is the result of less availability of trucking capacity. The gap is represented by the OTRI. The interesting part is that both CLAV and OTVI are falling. Most people familiar with transportation markets would think a transitioning market would have a flat to slowly growing CLAV and an increasing OTVI, which is what happened in 2020 as seen below.

This is a very telling detail that capacity is eroding at an incredibly fast clip. That is difficult to measure with traditional figures.

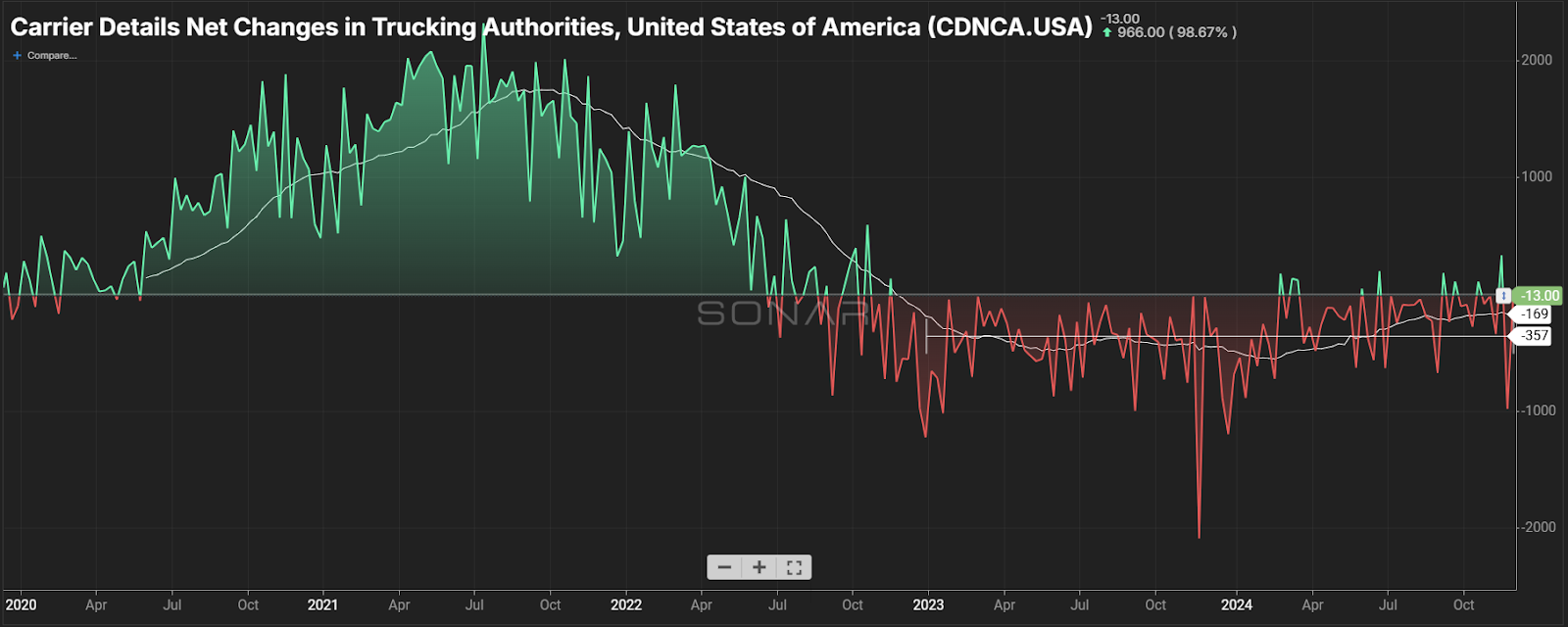

Carrier Details puts an extra layer of cleaning on Federal Motor Carrier Safety Administration data to get to its net changes (revocations plus additions) in active operating authorities that are reported weekly. This data would suggest there is a slowing of the erosion, but it does not account for size of fleets or the removal of tractors from ongoing operations. It is still a good measure of market conditions and health. Anytime it is negative, conditions are extremely challenging for carriers. It is rarely in this state for long periods of time as it biases toward growth. The two years of averaging more than 350 net carrier exits a week is historic and has never been seen.

The bottom line is that the exodus of capacity is finally showing up in the form of sustainably higher rejection rates. There is certainly a level of seasonal pressure on the market at the moment that was not present in May 2023, but the difference is not straight seasonality. Rejection and spot rates may slide after the holidays, but it should not be taken as a snapback moment.

About the Chart of the Week

The FreightWaves Chart of the Week is a chart selection from SONAR that provides an interesting data point to describe the state of the freight markets. A chart is chosen from thousands of potential charts on SONAR to help participants visualize the freight market in real time. Each week a Market Expert will post a chart, along with commentary, live on the front page. After that, the Chart of the Week will be archived on FreightWaves.com for future reference.

SONAR aggregates data from hundreds of sources, presenting the data in charts and maps and providing commentary on what freight market experts want to know about the industry in real time.

The FreightWaves data science and product teams are releasing new datasets each week and enhancing the client experience.

To request a SONAR demo, click here.