On a Thursday call with analysts, management from Schneider National (NYSE: SNDR) said they expect the current strong freight fundamentals to carry through the rest of 2021. Elevated consumer spending, incremental federal stimulus and the need to replenish depleted inventories were some of the catalysts supporting the outlook.

The company’s new full-year guidance calls for adjusted earnings per share of $1.60 to $1.70, which is higher than the prior range of $1.45 to $1.60 and the current consensus estimate of $1.59.

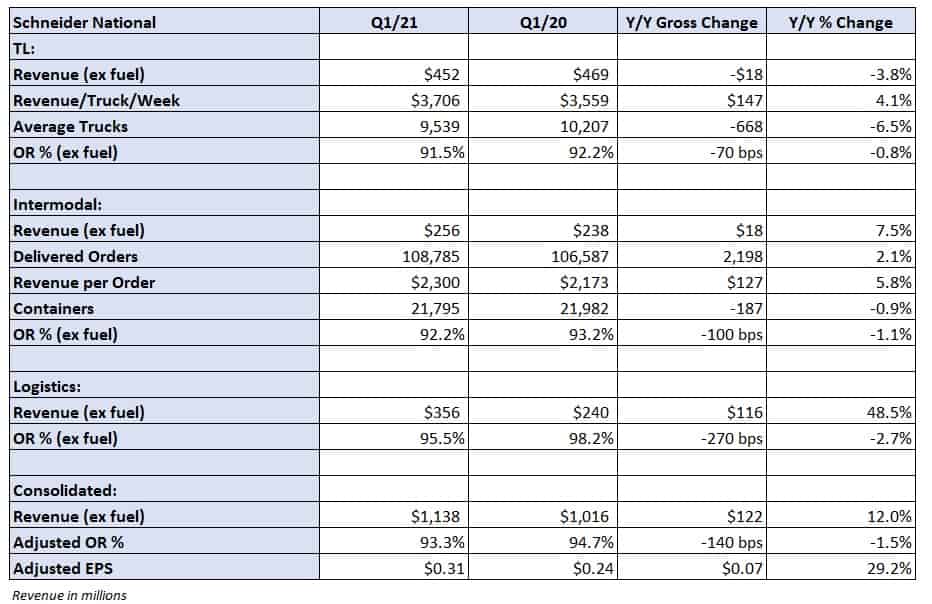

The Green Bay, Wisconsin-based truckload carrier reported first-quarter adjusted EPS of 31 cents, 3 cents ahead of analysts’ expectations and 7 cents better than the year-ago result. Gains on equipment sales in the quarter were $4 million to $5 million higher, a reversal from the loss reported a year ago but well within historical results.

A favorable rate environment, the result of high demand and a lack of drivers, moved contractual rate renewals up by low- to mid-double-digit percentages in the TL segment during the period. Additionally, rates on intermodal contracts are renewing higher by high-single digits.

TL revenue declined 3.8% year-over-year to $452 million as weather impacted the amount of capacity the carrier could put on the road. Revenue per truck per week was up 4.1% to $3,706, flat in the dedicated fleet but up 7.3% in one-way. Rate improvement, an increase in spot loads and a favorable insurance and claims profile led to a 70-bp operating ratio improvement at 91.5%.

Management said they weren’t satisfied with the current margin profile in TL and want to get to the high end of the long-term range of 11% to 13%. The first quarter of any year is seasonally the toughest for margins. By comparison the carrier posted ORs of 86.2% in the fourth quarter and 90.1% in the third quarter.

Schneider wants to grow TL volumes and revenue. It plans on adding a couple hundred trucks in the dedicated segment in 2021 and increasing the truck count by roughly 100 units in the over-the-road fleet. However, the new OTR fleet growth plan is 500 units lower than management’s expectation at the beginning of the year. Difficulties recruiting and retaining drivers have increased as the year has progressed.

An additional growth headwind will be production schedules at the original equipment manufacturers. Management said the OEMs are running approximately six weeks behind due to headwinds finding semiconductors and parts.

Schneider reeled in its net capital expenditures budget for the year to a range of $375 million to $425 million versus the prior expectation of $425 million due to the production issues.

Intermodal rail service is back to normal in the East but still challenged in the West, although improving. Container backlogs at West Coast ports and longer box turn times throughout the network remain headwinds. The company plans to add several intermodal containers to the fleet this year but acknowledged a lack of visibility in container production capabilities.

Intermodal revenue was up 7.5% year-over-year in the quarter as loads increased 2.1% and revenue per load climbed 5.8%. Continued volume expansion in the East offset the headwinds seen in the Western part of the network. The OR was 100 bps better at 92.2%

The logistics division recorded a 48.5% year-over-year increase in revenue, excluding fuel, at $356 million. Increases in revenue per load and load counts were the drivers. OR improved 270 bps to 95.5%.

Shares of SNDR were up 2.17% at noon EDT Thursday compared to the S&P 500, which was up 0.21%.

Hill Loans

Are you a business man or woman? Are you in any financial mess or Do you need funds to start up your own business? Do you need a loan to start a nice Small Scale and medium business?

If YES, kindly reply to this email as soon as possible: hillloansusa@gmail.com

E-mail: hillloansusa@aol.com

Phone + (+1) 804 660 2670

Website: http://www.hillloans.weebly.com

Hill Loans

A

Go away

Stephen Webster

These are the same companies that 10 months ago cut rates so many owner ops and small transport companies could afford insurance. Many had to sell tractors for scrap.