The Asia-U.S. container market is now in a class by itself, with the trans-Pacific eastbound trade pricing differently than any other route in the world.

Because stimulus-driven demand is so high compared to capacity — not just capacity of ships and boxes but of ports, trucks, rail and warehouses — the high-low spread of trans-Pacific spot pricing has ballooned.

The largest importers are paying far lower freight rates than smaller importers, the playing field is becoming increasingly uneven, and foreign ocean carriers are in position to pick the American import sector’s winners and losers.

“We’re seeing a price differential of $15,000 [per forty-foot equivalent unit or FEU] between the lowest short-term price in the [trans-Pacific] market and the top price,” said Erik Devetak, chief product and data officer of Xeneta, a Norwegian company that analyzes freight rates, during a press conference on Thursday.

“That implies a huge competitive advantage for established players, which has consequences across the economy and for everyday life, and also, from a point of view of lowering competition and increasing barriers to entry for future competitors.”

Patrik Berglund, CEO of Xeneta, added, “Everybody’s seeing price increases but … being really big is really a massive competitive edge in this market.”

Berglund warned, “When I think about the smaller mom-and-pop importers and exporters, I’m really concerned that if this lasts, the big players can eat even more market share simply because the infrastructure now is so tilted in favor of the big players.”

Origins and destinations matter a lot more

According to Devetak and Berglund, the trans-Pacific is no longer a single shipping market with a single “right price.” Rather, the vast spread between the high and low price has allowed carriers to splinter the trans-Pacific into multiple market layers. This explains why different container indexes are showing vastly different spot rates for the trans-Pacific.

“There is a whole series of different markets now for different situations and different import parameters,” explained Devetak.

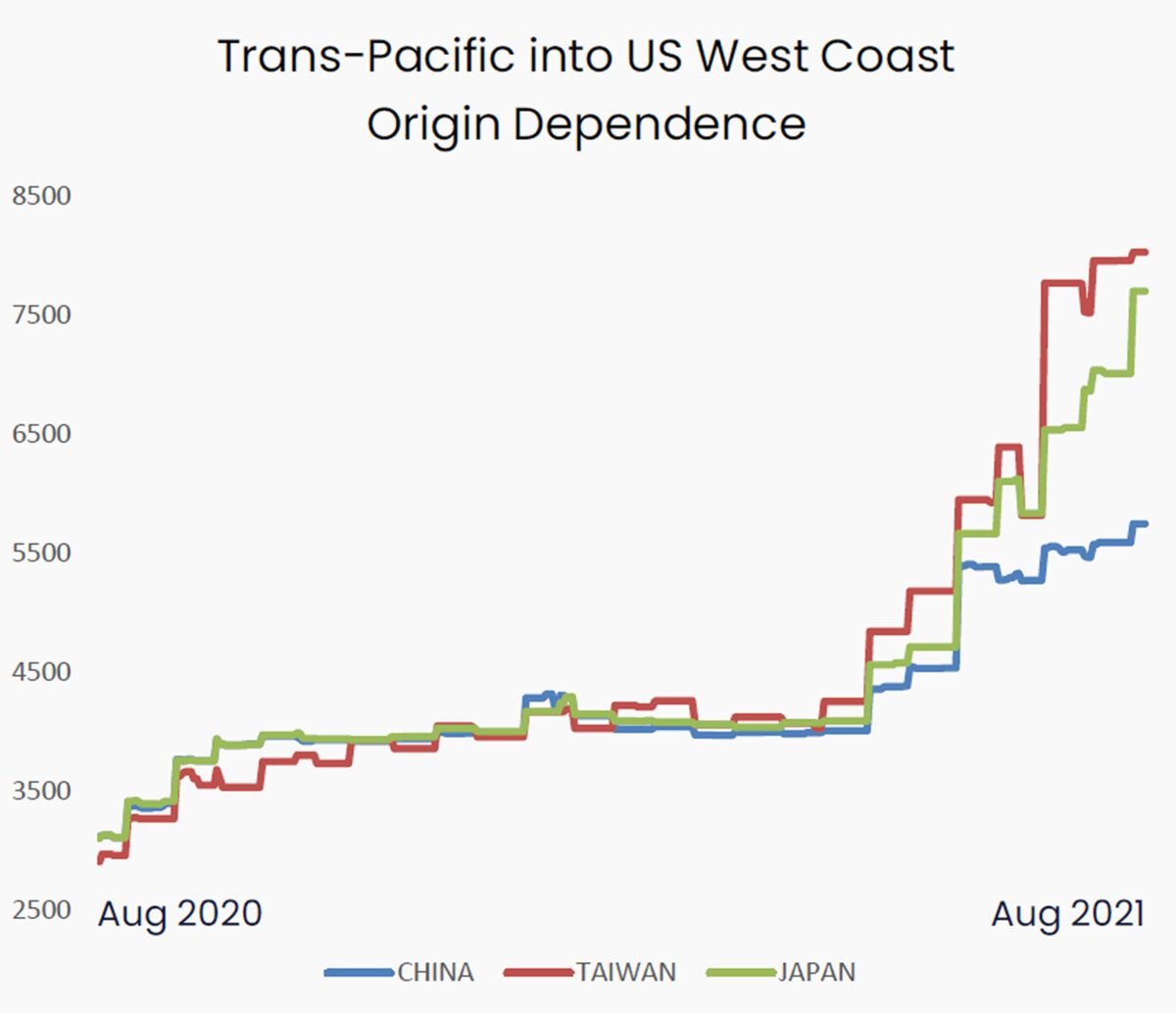

Port of origin has become one key parameter. “Historically, when we think of a single trans-Pacific market, if you go back a year, or a year and a half to pre-corona, the price differential between shipments originating in China, Taiwan, Japan or Singapore [to the west coast] was small — $100, $150, $250 [per FEU] max — on the order of 5-10% of the market rate,” said Devetak.

“Right now, we’re seeing the prices from China [to the U.S.] can be $2,500 lower than the prices one can achieve in Taiwan or Japan and $3,000 lower than Singapore. It can cost 40% more to ship from Busan [South Korea than from China]. That’s a striking price differential.

“There seems to be a strong preference [among carriers] to have a major port in China as the origin port and it seems like every other origin is indirectly being punished, probably because by concentrating on the main ports in China, one can deliver more goods and therefore have the highest profits.”

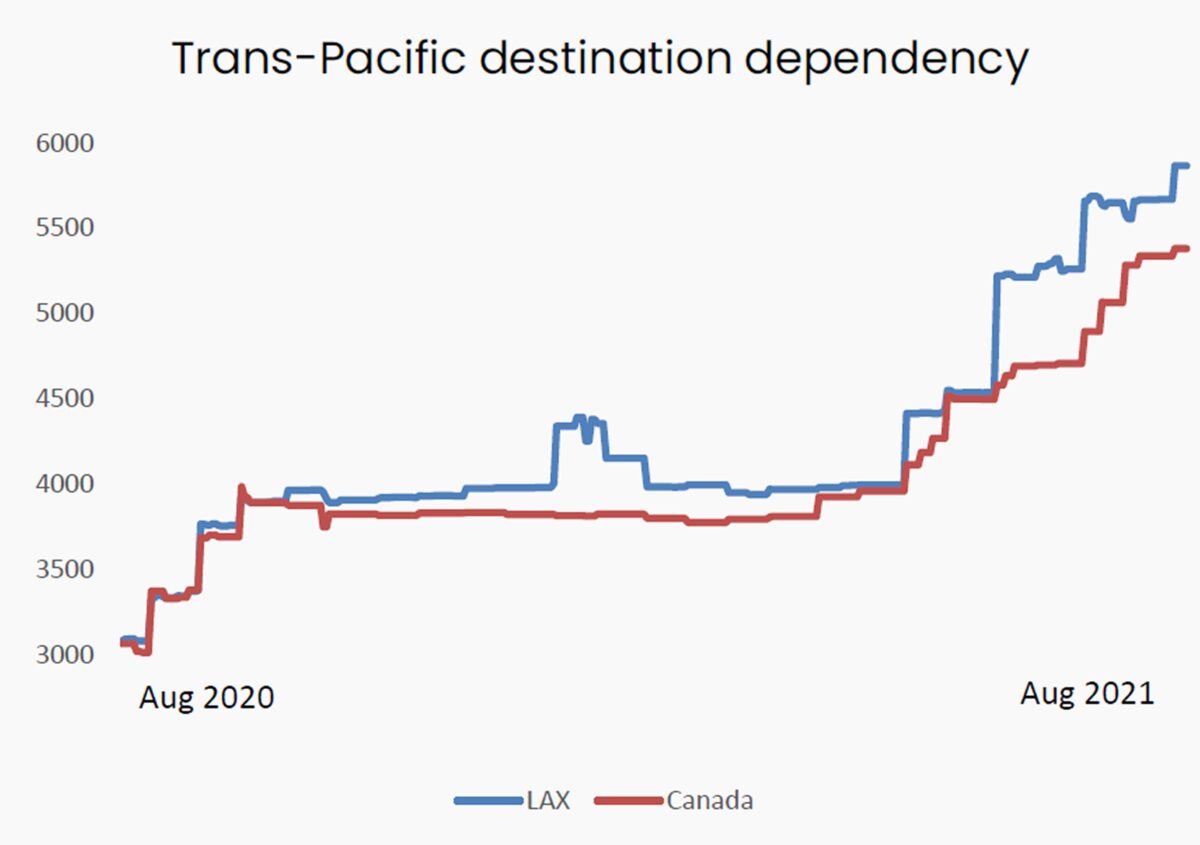

There are also trans-Pacific price disparities on the destination side. “Basically, anything that isn’t Los Angeles is preferred because you’re going to get stuck waiting for a berth in Los Angeles,” said Devetak. Short-term rates into Los Angeles/Long Beach can now be $1,000 per FEU higher than rates into Vancouver.

There is much less “geographic dependency” for pricing in the Asia-Europe trade lane compared to the trans-Pacific, Devetak noted.

Attractive vs. unattractive customers

Xeneta also found price differentiation regardless of origin and destination. It looked at short-term rates for cargoes from China to Los Angeles and found “huge developments in the market spread between the best performers and the worst performers,” said Devetak.

The differential between the high and low China-Los Angeles rates was $150 last year, or 5% of the market rate. It’s now $1,200, or 20% of the market rate. The spread has widened only recently, in the past few months.

“This is the price difference between what is an attractive customer to the carrier and what is a less attractive customer to the carrier,” he continued.

An attractive customer is generally one with large volumes, a strong preexisting relationship with the carrier, accurately predicted flows, a long-term contract being supplemented with short-term deals, and, in the case of a beneficial cargo owner (BCO), a direct relationship with the carrier as opposed to one using a freight forwarder middleman.

The rise of trans-Pacific premiums

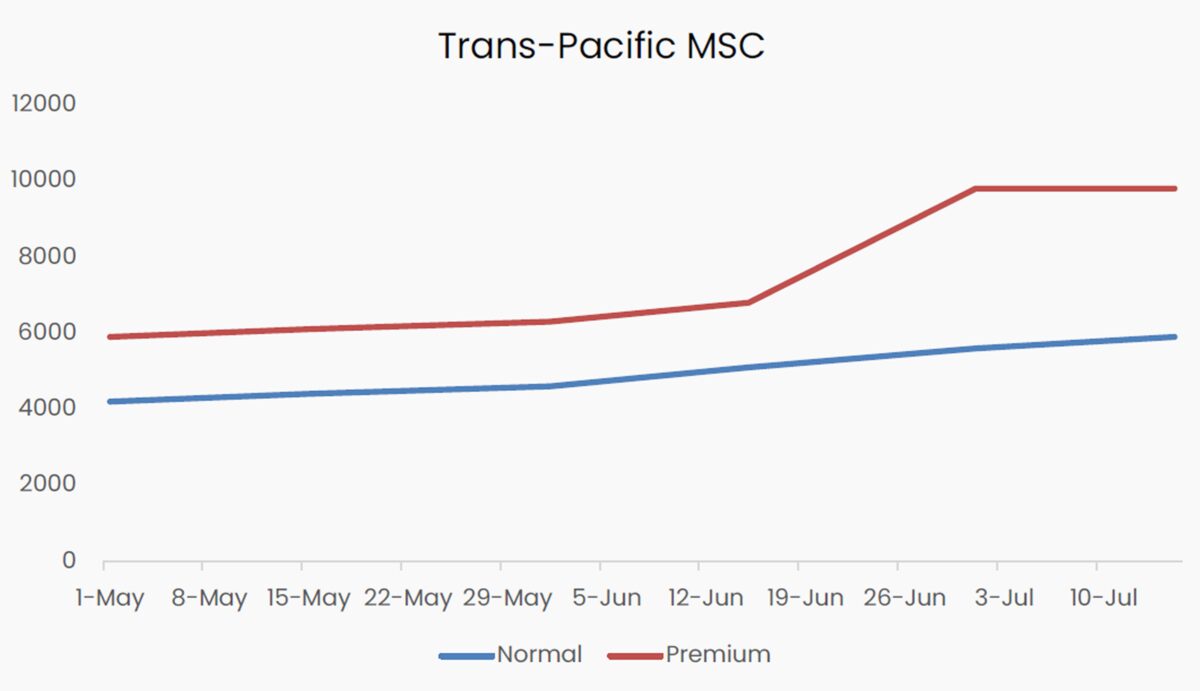

By far the most important price differentiator in today’s market is the premium paid to guarantee a cargo is loaded on a ship.

This is the biggest change since last year and the biggest differentiator of the trans-Pacific versus the rest of the world. Premiums are also being charged in the Asia-Europe trade lane, but not to the magnitude seen in the trans-Pacific.

“Shipping guarantees are not a new phenomenon, but the amount you used to have to pay to guarantee a spot on a ship was $100,” said Devetak. “Now, when we look at CMA CGM or Matson or ONE, we see premiums in the region of $2,500 or even more. If you look back to May, the premium you were seeing from MSC was less than $2,000. Now MSC is charging almost $4,000.

Carrier preferences for certain customers come into play when charging premiums, meaning that this too creates a more uneven playing field for importers.

According to Devetak, “The more attractive customers see both prices [the basic rate and the rate plus premium]. But a lot of the customers that are less attractive to the carriers — the small freight forwarders, the small BCOs — only have visibility on the rate with the extra charge. A lot of the market, at this point, has no availability of the non-premium offering.”

In other words, for many U.S. importers, it’s either pay the higher rate including the premium or find another carrier.

Same customer, same carrier, same contract … different price

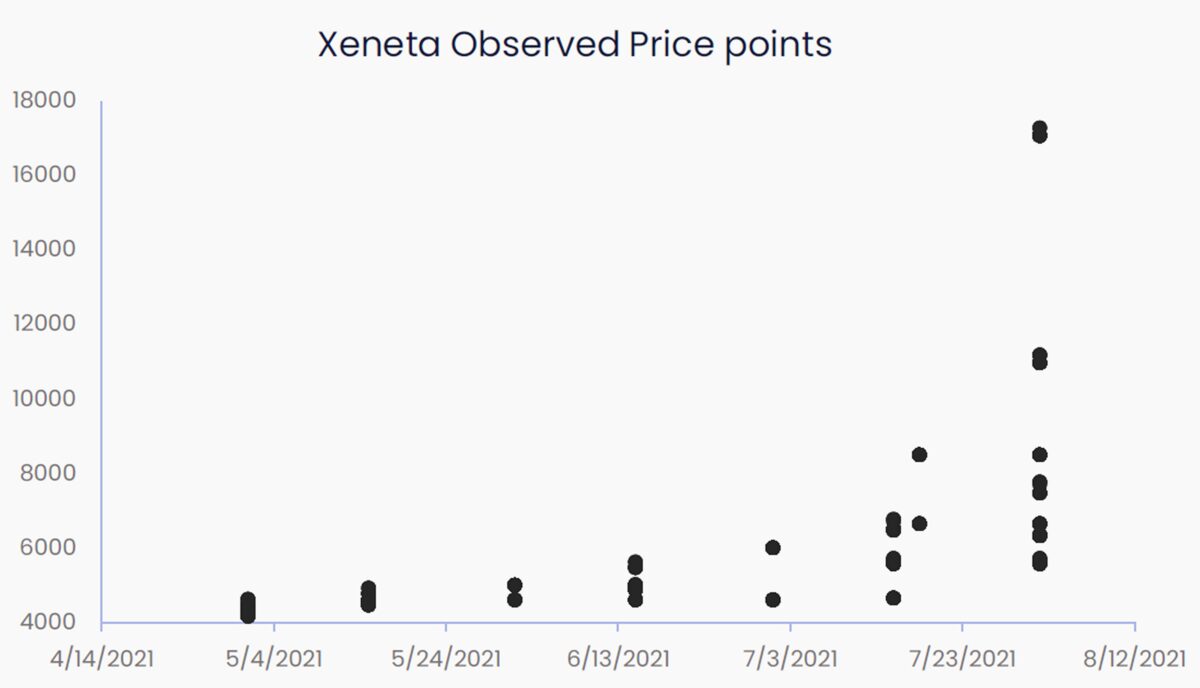

Highlighting just how much the trans-Pacific has changed in recent months, Xeneta provided a specific case of prices paid by one freight forwarder over time. The payments were all under the same contract to the same carrier.

Between April and early July, pricing was clustered in the $4,000-$6,000 per FEU range. By mid-July the spread had widened and ranged from $4,000 to $8,000. By early August, it had dramatically increased, with some prices under $6,000 and some as high as $18,000.

“We saw one market in the trans-Pacific in the beginning of April. But now we clearly see a market that has fragmented,” said Devetak.

“If you add all this up, you can conclude that if the origin is China, the destination is Canada, you’re an attractive customer, you go direct with the carrier and you ship next month, you end up paying $5,000 [in the short-term market].

“But if your origin is not China, your destination is Los Angeles, you are not an attractive customer, you go via freight forwarder and you need to ship as soon as possible, then all of a sudden, your rate is $20,000.

“To put this price differential of $15,000 into context, last year, it was $500.”

Click for more articles by Greg Miller

Related articles:

- Different container indexes, vastly different rates. Which is right?

- Clock ticking for Christmas imports as West Coast congestion mounts

- California congestion nears new high, East Coast gridlock worsens

- Global demand isn’t booming. So why are shipping rates this high?

- In the eye of the congestion storm: Q&A with Port of LA’s Gene Seroka

Eric Kulisch

Facinating analysis

Stephen Webster

Anyone who bought space on the spot market or a small shippers are a big disavantage. I think all shipping companies should be able to book up to 10 shipments per month at a certain fixed rate which 25 percent more than the average rate paid large shipping companies or receiving companies like home Depot or Walmart paid in the previous 6 months. In return a plan is put in place that minimum freight and wage rates for the next 3 years for all shipping companies by boat air or truck. Those companies that chose to chase bottom rates are getting what they deserve.