The highlight reel from Tuesday’s SONAR reports. For more information on SONAR — the fastest freight-forecasting platform in the industry — or to request a demo, click here.

Lanes to watch

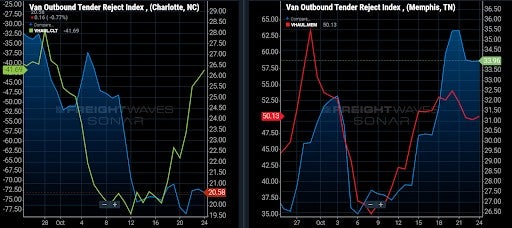

By Zach Strickland, director, Freight Market Intelligence

CHARLOTTE to MEMPHIS

Overview: Market conditions favor carriers shifting their trucks from Charlotte to Memphis.

Highlights:

- Charlotte’s dry van Headhaul score has increased as capacity tightens, but remains extremely low at -41.69.

- Charlotte’s dry van rejection rates declined in mid-October, and have held steady around 20%.

- Capacity has tightened in the Memphis market as the dry van Headhaul score increased to 50.13, pushing rejection rates up to 33.96%.

What does this mean for you?

Brokers: The Charlotte market is saturated with dry van capacity as more trucks are delivering into the market than outbound loads leaving the market, giving the market a Headhaul score of -41.69. Brokers should search the spot market for loads that run across the CLT–MEM lane, helping carriers shift their trucks to the stronger Memphis market. Hold firm on your bids, but brokers will need to push carrier rates down to create margins on the loads.

Carriers: Soft market conditions in the Charlotte market will reduce truck utilization for dry van carriers. Carriers need to search the spot market for dry van loads that deliver into Memphis, adjusting rates accordingly to secure the loads. Market conditions have tightened in Memphis, and rejection rates have increased to 33.96%, allowing carriers to increase their truck utilization and increase their rates for on-demand capacity.

Shippers: Shippers in the Charlotte market need to test the spot market for on-demand capacity rates as capacity builds in the market. Market conditions have softened in the Charlotte market, which should allow shippers to push carrier rates down since there is a surplus in capacity. Monitor rejection rates for any shifts that indicate market conditions are tightening, and adjust tender lead times accordingly.

CINCINNATI to ATLANTA

Overview: Outbound tender rejections likely to increase further in the days ahead as the Headhaul Index surges 17% week-over-week (w/w).

Highlights:

- Cincinnati outbound tender volumes are up 6% week-over-week (w/w), signaling that demand for outbound capacity is increasing.

- The Headhaul Index in Cincinnati is up 17% w/w, signaling that capacity is likely to tighten due to the growing imbalance between inbound and outbound volumes.

- Cincinnati outbound tender rejections are up 255 bpsw/w, but are likely to increase soon due to the growing imbalance between inbound and outbound volumes.

What does this mean for you?

Brokers: Cincinnati outbound tender rejections have been increasing over the last couple of weeks, and are expected to climb further as the imbalance between inbound and outbound tender volumes grows. There has been a 17% increase w/w in the Headhaul Index which is oftentimes a leading signal that capacity is likely to get tighter in the days ahead.

Carriers: Cincinnati pricing power will likely be shifting further into your favor in the coming days as larger peak season intermodal volumes arrive into Cincinnati from overseas with more and more shippers choosing to reroute freight inland via the East Coast from overseas in an attempt to bypass the severe congestion on the West Coast. Keep an eye on outbound tender rejections, and once they start to climb w/w, adjust your pricing to reflect the likely tightening of capacity.

Shippers: Your shipper cohorts in Cincinnati are currently averaging 3.1 days in tender lead times, but with outbound volumes and the Headhaul Index on the rise, it would be wise to push your tender lead times closer to 4 days through the next couple of weeks to ensure you are able to secure capacity if the market begins tightening further.

STOCKTON (California) to SEATTLE

Overview: Oversupplied Stockton market’s rejection rates jump

Highlights:

- Though not a record breaking move, Stockton’s outbound rejection rate hit its highest point in over a month, increasing from 13% to 15% over the past week. Heavy rains could be contributing.

- Lane specific rejection rates to Seattle made an even larger jump, increasing 2.7% over the past week and remaining well above the market average.

- Seattle’s outbound rejection rate has fallen significantly since the first of October, but is edging higher once again on consistent outbound demand.

What does this mean for you?

Brokers: Do not expect a large change in conditions in this lane, but coverage may be slightly harder to come by over the next week. This lane should have the highest priority among the more regular lanes moving out of the Stockton market if it isn’t already, as most carriers will want to move in the opposite direction and the weather will add to the challenges.

Carriers: Expect a bit more activity in this lane this week, diverting capacity to the spot market to cover. This lane should produce some of the highest margins out of Stockton, but do not expect Seattle to be any more productive for reload potential. Be on alert for road closures and mudslides.

Shippers: Be aware of unusually wet weather in the region that could lead to service delays. Expect slightly lower compliance in this lane this week, keeping lead times between three to seven days where possible to minimize spot market exposure. Both markets are oversupplied, but that only helps you on the origin. Seattle has not hit the busy season for the region yet.

Carrier update presented by PowerFleet

Zach Strickland, director of Freight Market Intelligence at FreightWaves, and FreightCaster Michael Vincent take a look at rejection rates nationwide in the Carrier Update presented by PowerFleet.

Good news for diesel buyers

From John Kingston’s weekly report:

A piece of positive news for diesel buyers: Diesel weakened slightly relative to crude.

In recent weeks, diesel prices have been climbing at a rate higher than the two key crude benchmarks: West Texas Intermediate, which is the U.S. benchmark, and Brent, the global crude benchmark. The spread of ULSD against Brent got as high as 56.14 cents a gallon on Oct. 14. But the spread Monday was down to 51.73 cents per gallon. On Friday it was even lower, declining to 50.25 cents a gallon.

Another piece of good news for buyers: Wholesale prices have started to come down. The national average wholesale price for ULSD in the ULSDR.USA data feed in SONAR is down roughly 4 cents per gallon in the past week.

Shipper update

Lead Economist Anthony Smith and FreightCaster Michael Vincent look at new houses sold and those impacts downstream in the Shipper Update.

Update on … dry van outbound tender rates, volumes

By Zach Strickland

The national average for dry van outbound tender rejection rates continued to decline last week to 20.01% as freight volumes declined to 11,205 index points. As we approach the end of October, SONAR users need to monitor rejection rates for any shifts as market conditions tighten, and carriers push spot rates upward for on-demand capacity.

Shippers in the Cape Girardeau, Cedar Rapids, Dubuque, Des Moines and Sioux Falls markets are struggling with dry van rejection rates over 40%, and rejection rates are over 30% in the Augusta, Omaha, Rock Island, Duluth, Memphis, Jefferson City, Shreveport and Evansville markets.

Carriers will find the most opportunity for dry van freight in the Ontario, Atlanta, Harrisburg, Dallas, Elizabeth, Los Angeles, Columbus, Allentown, Joliet, Chicago, Indianapolis and Houston markets, which are the largest markets by volume in the nation.