FreightWaves CEO and founder Craig Fuller described the rest-of-the-year outlook for the freight environment as “uncertain” during Thursday’s “State of Freight” webinar for April.

“I have heard a lot of arguments about folks that are bullish about the state of freight,” Fuller said. “I have yet to find a piece of data that actually suggests that there is an argument made for being bullish.”

The panel also featured FreightWaves market expert Zach Strickland and Adam Josephson, senior vertical expert.

Here are five takeaways from the April webinar:

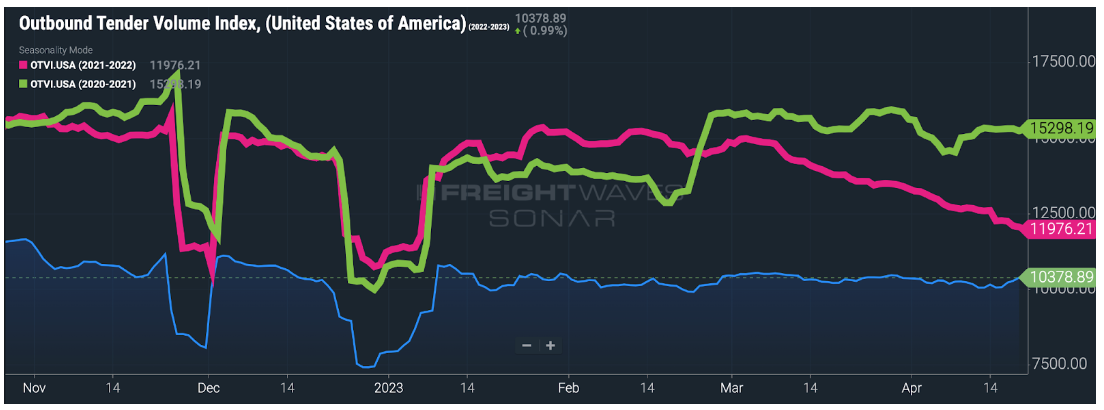

OTVI shows truckload volume is flat

Fuller said the current data from FreightWaves’ Outbound Tender Volume Index (OTVI) remains mostly flat, with little seasonality or truckload flows.

“I think in a normal year, you would have seen a March build, a limited drop-off in April — building really up until Easter, but we’ve not seen any level of seasonality,” Fuller said. “It suggests that the produce season isn’t producing, construction is not driving demand, retailers aren’t driving demand. It’s just a really flat year.”

FreightWaves market expert Zach Strickland pointed out that the OTVI data could also be read with some optimism.

“It’s still flat, which I can actually make the argument that is positive, considering we’re not falling,” Strickland said.

Fuller agreed that the data does have some silver linings.

“It’s a positive from the standpoint that there are no boom-and-bust cycles,” he said. “In fact, if you’re a shipper and you’re running a supply chain, it’s actually an incredibly positive thing for you, because it means that you’re not having to deal with trucks not showing up, or all the instability that you deal with in a volatile market. However, it is the enemy of the brokers and unfortunately for the carriers, because that lack of volatility is in a very loose market that’s oversupplied with capacity.”

Inflation is cooling consumer spending

In recent months, inflation has spurred consumers to cut down on discretionary spending, Josephson said.

“If you listen to what the retailers have been saying, starting even a year ago, Walmart and Target and others started talking about the shift away from discretionary items toward essential items,” he said. “Costco just talked about recently as well that their sales momentum has slowed quite considerably. They said quite clearly that their customers are still buying food, packaged and fresh foods, but they’re not buying discretionary items.”

Josephson said the reason people have less disposable income is the higher cost of services and dwindling savings.

“There’s this concept of excess savings that the Federal Reserve, JP Morgan and others talked about, that excess savings got built up because of all the government stimulus checks,” Josephson said. “Those excess savings have been whittled down. People have less and less money to spend; they’re not making money after the impact of inflation.”

Fuller said there is a correlation between a person’s average weekly earnings declining and the trend of falling freight volumes.

“The reason is that the people who are consuming the goods that move through the freight market are the folks that live paycheck to paycheck or live inside that market where they’re not investing money in the economy,” Fuller said. “These are the folks that are most impacted.”

Inbound ocean containers to the US have fallen dramatically

Strickland said that FreightWaves’ Inbound Ocean TEUs Volume Index (IOTI) is “arguably one of our better leading indicators for understanding what’s coming.”

Fuller said the IOTI data is indicating that retailers are not ordering more inventory at the moment.

“If retailers are restocking, because 75% of what moves on ocean containers is related to consumers, predominantly retail goods, if we’re seeing a situation where retailers believe that there’s going to be demand, then they start restocking,” Fuller said. “We’re just not seeing it; it’s very flat right now.”

Fuller noted that Henry Byers, FreightWaves’ head of ocean intelligence, predicted the deterioration of ocean import container volumes in an article he wrote in June 2022.

“This is the part that really threw people off last year: We talked about a deterioration in ocean volume,” Fuller said. “Henry wrote that article in June of last year, when the market really peaked in May; that was the largest import market.”

Linehaul spot market rates are close to the bottom

With spot rates hovering around $1.56 per mile, Fuller believes that they can’t go any lower.

“If you go back to 2019, it was a bloodbath, it was the last great recession,” Fuller said. “We were reporting on multiple bankruptcies a week. Some of them were quite sizable. It was the year Celadon went bankrupt.”

Fuller said the lowest linehaul spot rate in the 2019 market was $1.47.

“Now we’re at $1.56 today, but you have to remember how much nonfuel costs have increased for the carriers since 2019,” he said. “Looking at the nonfuel costs increases, you’re up about at least 30 cents a mile more, and there’s cost increases in driver wages. You’re also seeing things like insurance costs that have gone up, not significantly, but they have gone up, maintenance expenses are [also] actually much higher.”

Fuller said spot rates are constantly pulling on contract rates.

“If spot rates are up, it’s pulling contract rates up. It’s putting a lot of pressure on it. The further those two data points are, contract and spot, the more pressure it’s going to put on that rate,” Fuller said. “In my view, contract rates have much further to fall. We could end the year with contract rates being 20 to 25 cents less than where they’re at today.”

Nearshoring is not having a major impact on freight yet

Fuller said while nearshoring and reshoring of manufacturing from Asia to North America have been happening over the past several years, it could be a multiyear scenario before it has a major impact on the freight market.

“I am bullish on North America, because I say North America is going to be a primary beneficiary of the sort of reshoring pattern that is taking place,” Fuller said. “It will benefit the north-south trade, and the south-north trade of Mexico, the United States and Canada. I think it will have a big impact.”

Strickland said a lot of data indicates that in recent years manufacturers have left China for other parts of Asia.

“Movement from China to other Asian countries has been more significant than that from somewhere to Mexico, but it is trending towards Mexico,” he said.

Fuller said reshoring and nearshoring have already benefited U.S.-Mexico ports of entry such as Laredo, Texas.

“Laredo is growing. It’s now the No. 1 port in the U.S.,” he said.