FreightWaves’ State of Freight webinar for August discussed the holiday season and what it could mean for carriers in 2024, as well as an ongoing surge in West Coast container imports, and the need for more trucking capacity to exit the marketplace.

Craig Fuller, FreightWaves CEO and founder, said, “the fourth quarter is where you make all your margin. That’s really the most important quarter of the year, and it’s largely driven by holiday goods.”

Here are five takeaways from the webinar:

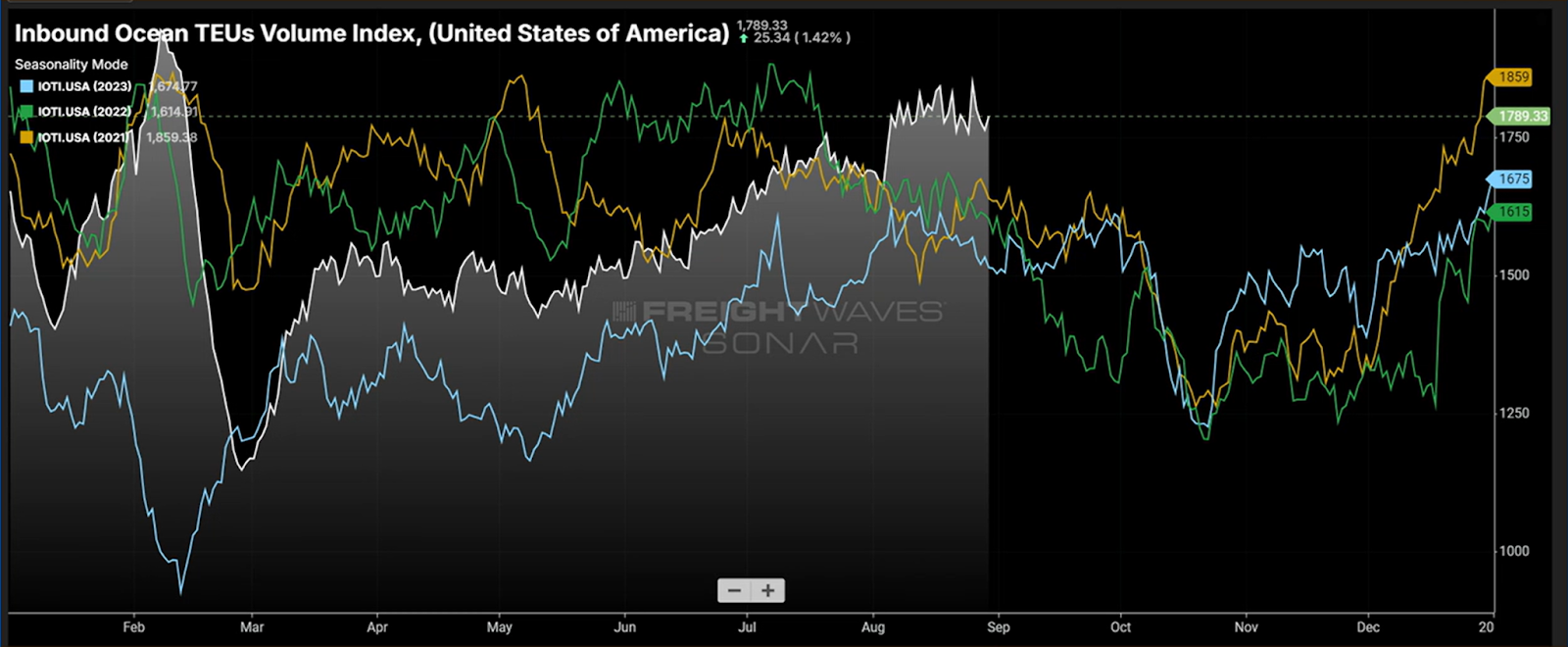

The Inbound Ocean TEUs Index shows a lot of containers headed to the US

Fuller said freight volumes in the fourth quarter should get a boost from imports of containers from China.

“One of the things I think is really interesting is that the ocean container movements foretell what we’re about to see in over-the-road trucking and intermodal,” Fuller said.

Container import volume into the U.S. continues to trend upwards compared to August 2023, according to FreightWaves’ SONAR Inbound Ocean TEUs Volume Index (IOTI.USA). Import volume into the U.S. increased 14% year over year in June and was up 18% year over year compared to July 2023.

Zach Strickland, FreightWaves Director of Market Intelligence, said the IOTI.USA index for container movements shows large amounts of freight coming to the U.S.

“This shocks me at how crazy this data set looks,” Strickland said. “The white line is the current year, and I left the pandemic era on here. So the green and orange lines are the pandemic era years where we had this flood of imports. Right now, we are seeing bookings data on par with the pandemic years.”

Fuller said while volumes are high, the freight marketplace isn’t seeing the disruption from all of the container movements like it did in 2021 and 2022.

“The reason we’re not seeing a supply chain crunch or supply chain inflation is because what’s driving the volume today are the big importers and the big box retailers, and not a lot of the other importers that make up the broader part of the economy during COVID,” Fuller said.

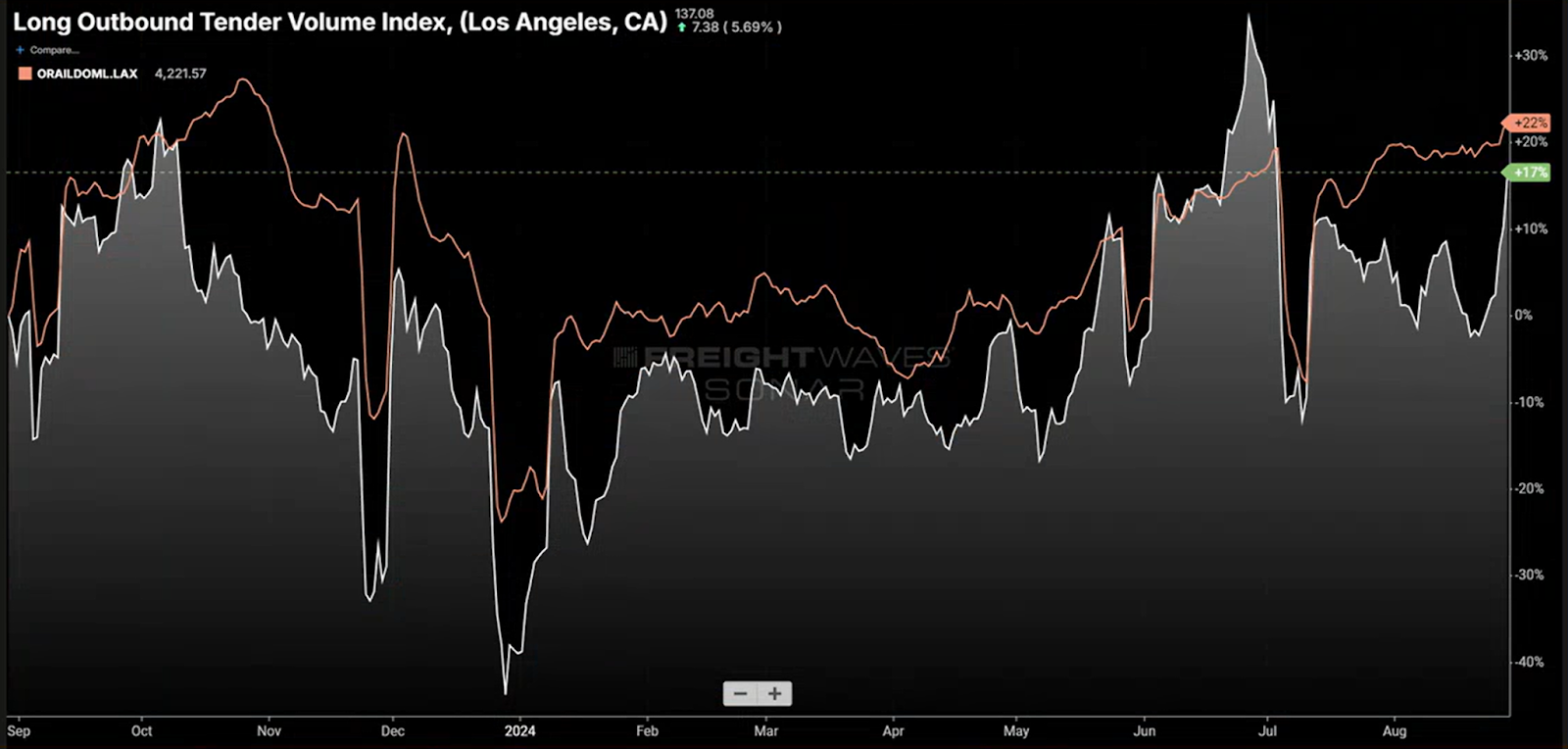

Los Angeles has become a bellwether for the global supply chain

Looking at the Long Outbound Tender Volume for Los Angeles and the Rail Intermodal – Container Volumes indices, freight movements are trending upwards since mid-July.

“This represents the loads moving more than 800 miles leaving the Los Angeles area market,” Strickland said. “On top of that is the domestic intermodal Los Angeles outbound component. This is stuff that’s literally getting translated onto a 53-foot container from probably some international containers leaving the port area and crossing the country. Los Angeles to me, has become kind of this bellwether, or maybe just this centroid of global supply chain activity. I feel like that this long haul component out of Los Angeles is getting relief that did not occur during COVID from the rail yards.”

Fuller said there is enough trucking capacity in the market to absorb all of the freight moving from the West Coast to other parts of the country.

“What’s driving this particular surge in goods is different from what drove the surge in goods during the COVID years,” Fuller said. “That surge in goods was caused by so much moving through the economy and you couldn’t get your hands on any capacity. We’re not seeing that right now.”

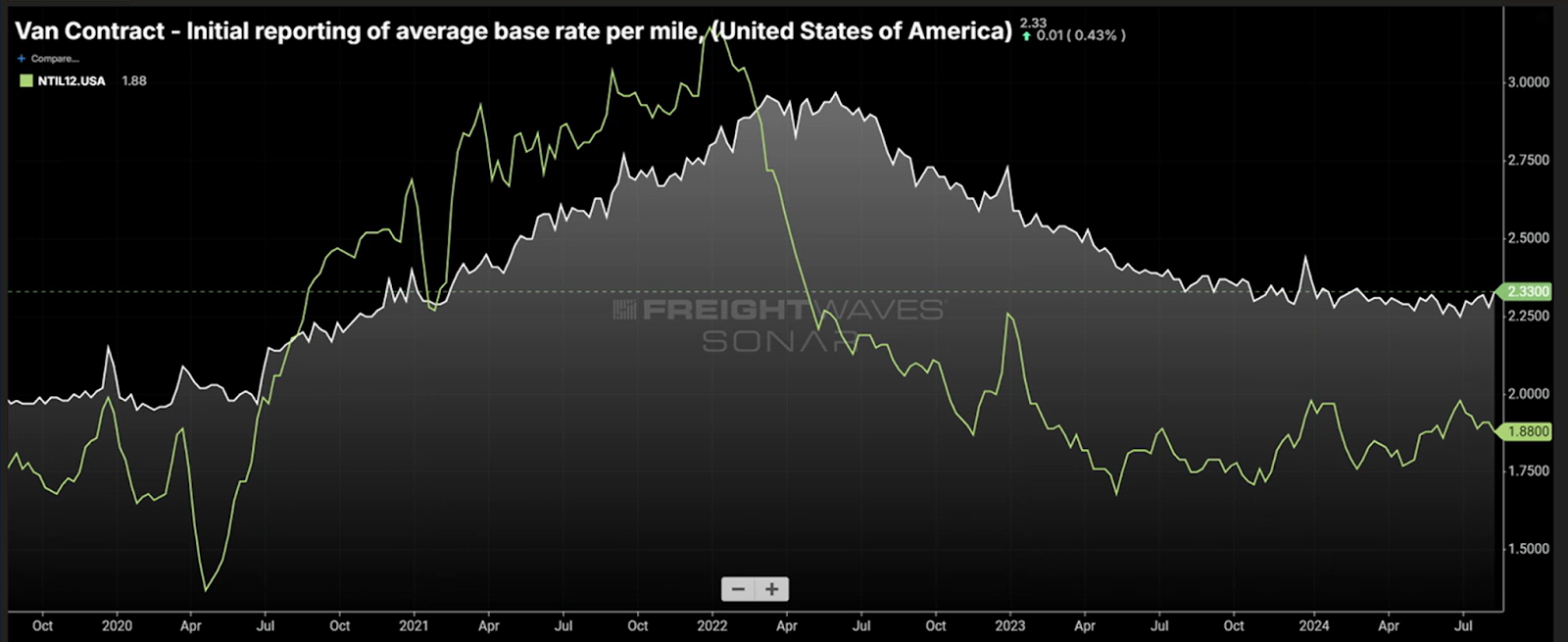

Contract rates are showing some positivity in the marketplace

Truckload contract rates (VCRPM1) continue to show stronger upward movements in relation to spot rates, Strickland said.

“Contract rates are now starting to trend up,” Strickand said. “We’ve actually started to see the front edge of a turn. Now it’s very short, and it’s not a long term signal at all, but it looks like rates on the contracts are starting to turn up, a signal that we’ve seen already out of the spot market for the past year.”

Fuller said while contract rates are slightly up, it’s unclear whether it’s a trend that will continue for the rest of 2024.

“I think it is fair to say that contract rates probably are not getting cheaper,” Fuller said. “The market cannot reset until there’s more of a normalized range between contract and spot. It is getting close to there. It also tells us we have a little bit of room to go before the market is truly in balance.”

Related: State of Freight for July: ‘Bullish’ market coming for freight economy

Not worried about possible disruptions from port worker’s strike

Strickland questioned whether a potential East and Gulf coast strike from dockworkers with the International Longshoremen’s Association (ILA) could affect the freight market in the coming months.

Contract talks between the ILA and United States Maritime Alliance are ongoing but some shippers are preparing to avoid any disruption if a strike occurs starting Oct. 1.

Fuller said election years are usually the worst time a union can threaten to hold a worker’s strike.

“I don’t think the Biden administration, which has been arguably the most labor friendly administration in decades, can afford to let a strike go on to disrupt the holiday season,” Fuller said. “They will likely put it into some type of arbitration. The administration will do everything it can to avoid a strike or a shutdown before the U.S. election. Frankly, if I’m the union, the worst possible time to have my contract come up is right before a U.S. election, because there is no way that the Biden administration or the Harris administration can allow for something catastrophic to happen to it.”

There’s still too much trucking capacity in the market

Fuller said more trucking capacity has to leave the market before the freight recession can end.

FreightWaves reported in July that $37 billion in Small Business Administration loans went to 419,500 companies in transportation and warehousing during the pandemic. The loans helped carriers hang around the market for far longer than anyone anticipated, keeping rates lower for longer, according to FreightWaves’ John Paul Hampstead.

“We want to see operators that have stayed in the industry, that do not have state sustainable businesses, to leave the market. Because this market needs a reset. We need to wash it out,” Fuller said. “I hate the fact that people struggle. As someone who takes risks in business, it sucks. No one wants to lose their job. No one wants to lose their business. But this is the way that the market works. We need a reset.”