Importers and exporters should brace for the pandemonium roiling the ocean freight sector — where container shipping delays and prices are at all-time highs — to wash over the air cargo market this month.

Full planes and skyrocketing freight rates are signs the market has tightened to the point that shippers will be hard-pressed to find air transport for their goods as holiday-season shipping enters the stretch run, according to market analysts and logistics specialists.

Welcome to the super-peak season.

The main culprit is a capacity deficit caused by the severe reduction in international passenger flights as cargo demand, increasingly converted from ocean bookings to air to avoid port congestion, exceeds pre-COVID levels. COVID outbreaks among pilots and airport staff in Asia have reduced flights, further squeezing logistics companies and their customers.

Destination airports with traditionally strong freighter traffic, such as Chicago O’Hare, Los Angeles, Dallas-Fort Worth and New York’s JFK, are so crowded because of workforce shortages that it can take three days to two weeks for terminals to make shipments available for pickup. Many O’Hare facilities are storing pallets in parking lots with temporary fencing because they can’t break down large shipments quickly enough for distribution. And when cargo is available, receiving agents are having difficulty finding trucks because many drivers have not returned to work from early COVID separations.

Demand is expected to surge further in the second half of October because of the holiday orders, the pickup in Chinese factory production after a weeklong break for the Golden Week holiday and continued congestion at transit hubs, including in Europe.

Large retailers and manufacturers, desperate to quickly get stalled shipments to customers in time for holiday shopping, are sucking up most remaining capacity by renting entire aircraft from cargo airlines to guarantee delivery. The supply-demand imbalance has driven airfreight rates on major trade lanes five times higher than normal for the busy fourth quarter — and still climbing — to levels approaching the early stages of the pandemic in 2020, when frenzied governments and health care organizations paid any price to airlift personal protective equipment and ventilators.

“October is probably going to be one of the worst months [ever] in terms of airfreight transportation for the shipping community” because of congestion and cost, said Edward DeMartini, vice president of air logistics development for North America at Kuehne + Nagel, the world’s largest air forwarder in terms of volume.

Many U.S. and European retail importers started utilizing air cargo charters in July for goods that would normally move from China by sea as door-to-door transit times more than doubled to 80 or 90 days in some cases. Roughly 60 container vessels are now waiting for berths outside the Los Angeles-Long Beach port complex, and 30 are offshore waiting to enter the Port of Savannah on the East Coast.

Companies are furiously bidding to secure any remaining freighters, as well as temporary cargo-only passenger aircraft, through the end of the year. Fashion brands and others with high-margin products, such as electronics, or manufacturers needing components for production lines, are willing to pay top dollar rather than lose potential sales, or customers. Making the decision somewhat easier is the fact that increases in ocean-shipping rates have significantly outpaced those in air, narrowing the price gap between the modes.

Nike, for example, has contracted for a large quantity of freighters to make up time after authorities in Vietnam shut apparel and footwear factories, or forced them to operate at minimum levels, to contain COVID outbreaks, according to the company and air cargo professionals. Peloton is also making heavy use of airfreight this year after experiencing manufacturing problems.

“We’re chartering like mad,” said Marc Schlossberg, executive director for air cargo at New York-based Unique Logistics (OTC: UNQL). The third-party logistics provider, which recently filed to be listed on the Nasdaq exchange, has scheduled more than 100 new flights in the next 60 days from India, Bangladesh and Vietnam to support customer demand. The contracts for dedicated carriage, arranged through brokers or directly with cargo airlines, give forwarders guaranteed space and direct control on routes and schedules compared to booking shared aircraft space.

“Retailers, among others, have recognized that the global ocean freight supply chain is broken and they cannot rely on any estimated times of arrival, so they are converting massive volumes to air freight for the holiday shopping season, and likely beyond, as there is no sign that the ocean congestion is improving,” Schlossberg said in an email.

Greeting card companies and specialty costume stores, nervous about products not arriving in time for the Halloween, Thanksgiving and Christmas holidays, were among those renting large all-cargo aircraft, DeMartini said in a recent webinar.

The chance of finding a cargo carrier that can spare an aircraft for the average customer is slim because October is when the integrated logistics providers — FedEx, UPS and DHL — contract with other airlines for extra capacity to augment their regular fleets as parcel volumes grow, and technology companies like Apple and Sony use hundreds of prearranged charter flights to get big product launches to locations around the world.

“The market has gone insane,” Brady Borycki, executive vice president of global business development at Wen-Parker Logistics, told FreightWaves.

“There is absolutely not enough commercial lift. There’s problems at origin, problems at destination. Honestly, if you’re not chartering right, I’m not sure how you’re managing to service your customer base because the demand for airfreight is so high. The ocean market is so screwed up that companies are basically saying we’re going to miss Christmas, we’re going to miss Black Friday. We’ve got all this cargo stuck in China or Vietnam and it’s not going to make it.”

With space selling out, shippers need to use multiple logistics providers that control leased aircraft to cobble together enough capacity because they are all booked, Borycki said.

“If you don’t already have arrangements made, you’re in trouble,” he explained. “We had one customer come to us for a massive [ocean] conversion out of Vietnam. We were not able to provide everything they needed. They went to at least one other forwarder and it ended up being a request for something like 90 charters.”

Astronomical rates

The Baltic Air Freight Index (BAI), powered by TAC Data, finished September at the highest level since the index first reported in January 2018. It shows ir cargo rates globally have increased 166% on average since October 2019, but inflation is greatest on routes from Asia to North America and Europe.

Average Asia outbound airfreight rates moved up sharply in September and the upswing is happening earlier this year — and off a higher base, according to the BAI. Spot rates for Hong Kong to Europe and North America were up, respectively, 66% and 85% year-over-year and 21% and 13% since August. Out of Shanghai, the numbers are even starker. In September, prices rose 73% from 2020 and 38% since this August. Rates to North America jumped 116% versus September 2020 and 40% since August.

Benchmark spot rates from Asia have topped $10 to $15 per kilogram.

But the true rate to ensure a booking makes it on a plane, without getting bumped and having to wait up to two weeks, is closer to $18 to $20 per kilo, with some quotes as high as $22, according to DeMartini.

Absolute rates from China to North America are closing in on the all-time peak in the second quarter of 2020 when the rush to source personal protective equipment drove air cargo rates near the $20 mark.

The situation is similar to the ocean world, where shipping rates have spiked several hundred percent to more than $10,000 per container but don’t reflect premium charges for equipment, space guarantees and customs services that can push the price above $20,000 for a forty-foot box.

The rent on a 747 freighter for a single flight from China to Chicago is now $1.5 million to $2 million, compared to about $500,000 two years ago. And for companies trying to get products out of Vietnam, charter rates are running between $2.5 million and $3 million, DeMartini said. The latter figure is equivalent to $25 to $30 per kilo.

Shipping prices to Africa are also rising because capacity has dried up, with most freighters pulled into the major trade lanes. And airlines have sharply cut widebody passenger service to South America via Miami, a major gateway for shipments from North America, Europe and Asia, which has triggered large rate increases for cargo too.

Shippers in Asia are increasingly turning to sea-air products, as well as rail and truck, to bypass port congestion for shipments to Europe. A sea-air move involves booking an ocean leg to Dubai, or another intermediate port, and then arranging ground transport to the airport, where the shipment is repacked and put on a plane to the destination city. Some logistics providers, such as San Francisco-based Flexport, are using technology to identify a customer’s highest selling merchandise and move it by air, with the rest sent by ship.

“It’s going to get messy pretty soon,” said Niall van de Wouw, managing director of Clive Data Services, during a briefing with reporters.

The firm last week released data illustrating how the annual fourth-quarter surge will be more pronounced this year. Airline load factors — the percentage of an aircraft’s available cargo payload that is utilized — in the last week of September were higher than the pre-COVID peak seasons in 2018 and 2019.

Clive sources data on widebody passenger and freighter flights from many airlines around the world but doesn’t measure cargo on smaller, single-aisle passenger aircraft that tend to fly domestic or short-haul routes.

Planes were 66% full for the entire month, on a global basis, with demand up 1% while capacity shrank 13% versus 2019. Fewer aircraft in the air means any extra throughput is felt more by the logistics system. A strong upward trend toward the end of the month pushed the dynamic load factor, which accounts for both the volumetric size and weight of shipments, to 68%.

Before the pandemic, peak-season load factors hovered around 67% and last year reached 72%.

(The International Air Cargo Association, which uses a different methodology that doesn’t factor in dimensional weight and can double count some shipments, says air cargo is growing at an 8% clip versus 2019, with capacity 12% lower.)

Aircraft utilization of 68% may not sound like much, but it’s quite high for so early in the surge season. Also, the maximum global load factor is about 80% because of trade imbalances on certain routes — think heavy exports from Shanghai and weak backhauls — where emptier planes push down the overall average, van de Wouw explained.

Planes departing major Asian airports to North America, Europe and the Middle East are completely full, with an average load factor of 92%. Aircraft utilization from Shanghai is up to 91% from 76% last month after authorities relaxed COVID-related workplace restrictions to prevent virus spread that resulted in freighters leaving partially or fully empty for several weeks because they couldn’t get loaded.

Some Europe-to-Shanghai rates finished September 60% higher than before the outbreaks in Shanghai, according to WebCargo, a multiparty booking platform for air cargo.

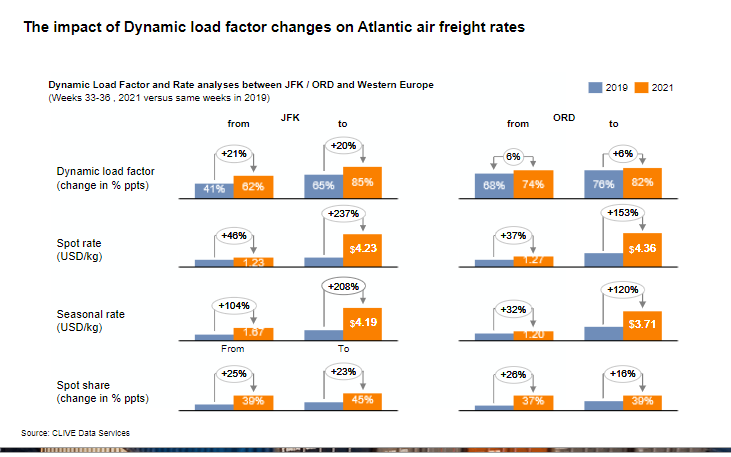

An 80% load factor represents the tipping point for rate increases, according to van de Wouw. Load factors for Europe in and out of New York’s John F. Kennedy International Airport, for example, increased about 20% each way during the previous four weeks, but rates for immediate delivery were up 46% out of JFK compared to 240% on inbound flights. The difference is that the inbound lane had a 24-point greater load factor to begin with and the extra volume pushed the load factor to 85% — a seller’s market — compared to 62% for export flights.

About 40% of airfreight shipments are currently moving under spot-rate transactions, as carriers allocated more space for last-minute bookings to take advantage of the pricing environment, compared to longer-term contracts, according to Clive Data.

The trans-Alantic cargo market is likely to benefit most from the U.S. decision to allow vaccinated travelers from 33 countries to enter the U.S. with a negative COVID test, beginning in November, because it is dominated by passenger aircraft more so than freighters.

U.S. and European airlines are adding some flights in anticipation of an uptick in passenger demand, which could mean a more stable peak season for westbound cargo compared with other trade lanes.

Even so, analysts say it could be next summer before there is significant recovery in passenger demand, especially with businesses strictly limiting employee travel. And many of the incremental flights being added by airlines are to vacation destinations like Las Vegas or beach areas where people are converging during COVID but where there is little cargo demand.

Load factors will drop below the 80% mark, bringing rates with them, once intercontinental travel picks up again. But in the short term, the situation could actually get worse for shippers, said van de Wouw. That’s because airlines will make sure they fill existing flights before they start adding frequencies and swap in larger aircraft; plus there will be more baggage competing with cargo for lower-deck space.

Air cargo capacity may catch up to pre-COVID levels because more airlines are making a strategic shift for medium-haul traffic to newer, fuel-efficient narrowbody jets, like the Airbus A321 Long Range and the Boeing 737 MAX. They provide higher yields per passenger but aren’t big enough for heavy cargo. United Airlines, American Airlines, JetBlue and Aer Lingus are among carriers planning to deploy smaller jets between cities in the Northeast, like Philadelphia and Boston, and in Western Europe.

“We’re probably never going to get back to those cargo rates that we used to know in the 2017 and 2018 environments simply because I don’t know that we will ever get back to the amount of cargo capacity that we had,” DeMartini said on the webinar.

Click here to read more FreightWaves/American Shipper stories by Eric Kulisch.

RELATED STORIES:

Supply chain woes drag down Nike sales

Retailers eye more air cargo as COVID lockdowns intensify in Vietnam

IATA forecasts 2021 air cargo revenues to hit record $175B

Stealing your own freight: O’Hare cargo delays force drastic measures

Cargo airlines cancel hundreds of China flights amid COVID outbreak