The views expressed here are solely those of the author and do not necessarily represent the views of FreightWaves or its affiliates.

In 2020, hospitals around the world faced a shortage of N95 face masks and other medical essentials, adding to the chaos surrounding COVID-19. Two years later, the same hospitals confronted the opposite problem, as a surplus of supplies overwhelmed the system.

These issues ignited the demand for health care supply chain solutions, triggering a wave of M&A.

In 2023, the global health care industry completed over 2,700 deals, representing $341 billion in value, an increase of 22% over the prior year. In the coming year, 70% of all health care leaders expect to see this consolidation continue.

Understanding the implications for CEOs of supply chain companies in this sector is crucial for the investing community.

On one side, industry leaders such as McKesson, Amerisource and Cardinal are consolidating the market. On the opposite side, venture-backed startups like Vamstar, Notisphere and Hystrix are securing substantial capital.

Determining strategies for midsize companies to optimize value and prevent getting stuck in the middle is essential.

This industry dynamic is characterized by the pressure exerted on midsize companies, compelling them to respond swiftly and strategically. Optimal approaches include (1) investing in growth and differentiation to secure additional market share, (2) engaging in rapid, inorganic growth by acquiring smaller companies, or (3) considering a sale to a financially robust entity.

The market

The global health care supply chain management market is expected to grow close to $8 billion by 2030, representing a 15% compound annual growth rate, a figure consistent with the fast-paced growth throughout the rest of the industry.

Domestic players in the supply chain are expecting growth as well. U.S. 3PLs that service health care expect their market to grow to $193 billion by 2032 with a 9% CAGR.

Midsize CEOs aiming to capitalize on this market growth must strategically position themselves as viable candidates for acquisition or to acquire other entities.

Recall that in just a few decades, the supply chain and logistics industry serving health care has evolved significantly. Systems that previously relied on pen and paper have undergone massive changes, with customers now expecting accurate, real-time data on inventory management, medical resources and other core logistical items. The continued trend of technological advancements within the space coupled with the consolidation throughout the health care sector will lead to exciting (or concerning) futures for health care supply chain companies, depending on how they respond to the changing dynamics.

Increasingly large and complex health care systems will soon scrutinize their providers’ abilities to meet their evolving needs. The winners in the industry will disproportionately be those who best adapt to the environment, especially by supplementing their organic growth with strategic acquisitions.

Before delving into the key drivers of the health care supply chain M&A trend, it’s helpful to highlight the various segments of the market.

Key market drivers

Increasing M&A activity in the health care industry results in fewer, yet more valuable, contracts available for the logistics and supply chain providers. The companies that win the mega contracts will be cash-rich and ultimately emerge as winners in the space.

However, to fulfill the scope of these massive contracts, the providers will need to bolster their service offerings, achievable through the acquisition of their competitors.

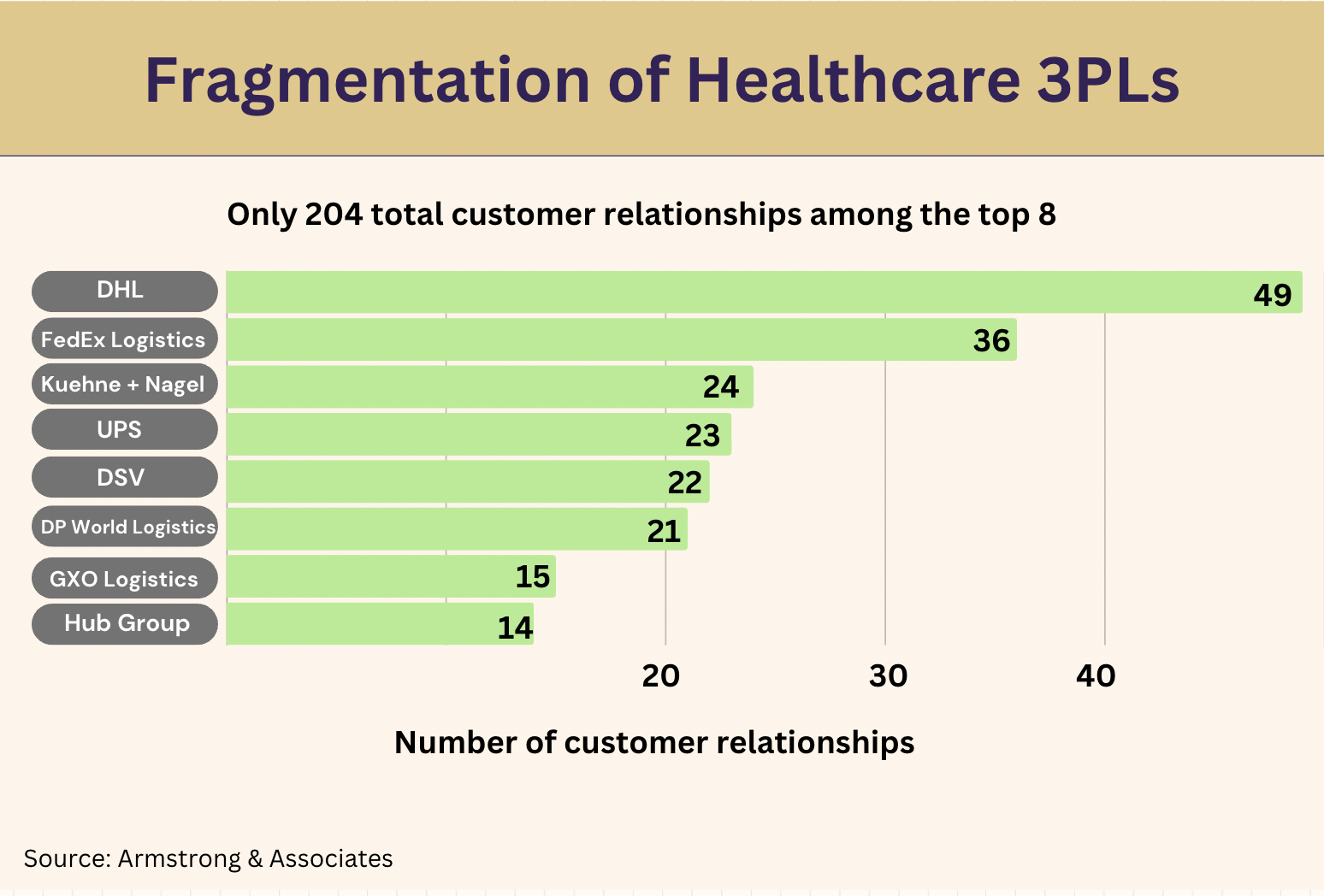

Currently, the eight most prominent health care 3PLs, comprising familiar names DHL, FedEx, Kuehne + Nagel, UPS, DSV, DP World Logistics, GXO Logistics and Hub Group, represent only 204 customer relationships.

Despite the active consolidation of the health care industry, most of the available contracts belong to companies outside the top eight, providing evidence of the fragmented market for supply chain and logistics providers.

To adequately address the changing needs of their clients, the smaller firms will experience an upcoming trend toward consolidation.

Ultimately, the three main drivers of the consolidation of the health care supply chain are the rapid restructuring of the health care sector, the development of new technologies and the emergence of cash-rich companies seeking acquisitions.

Rapid restructuring

There’s been a tremendous increase in M&A activity across the health care sector, largely driven by rising supply chain expenses that push the entire industry to consolidate its internal resources to force a more robust supply chain.

As the industry’s resources become increasingly centralized, the winners of the supply chain landscape will be the companies that secure outsize contracts with the health care giants. Thankfully, the development of new technology and the birth of cash-rich acquirers will lead to a restructuring of the health care supply chain that can fulfill these behemoth contracts.

Development of new tech

During the past couple of years, there has been meteoric growth of both AI and other technologies that improve the capabilities of companies and entire industries. More specifically, in the health care supply chain, the growth of health care e-commerce and the desire to create a more robust supply chain after COVID-19 revealed shortcomings that resulted in the maturation of the supply chain and caused logistics companies to bet on blockchain technology, cloud-focused solutions and AI’s predictive capabilities.

London-based company Vamstar, for instance, is a B2B health care supply chain platform leveraging machine learning to improve sourcing and procurement processes for medical device and pharmaceutical companies. In just a few short years since its launch in 2019, it has secured an impressive $10 million in funding to date to bolster operations and acquire additional market share.

Another venture-backed challenger, Notisphere, provides a recall management platform for health care supply disruptions through its proprietary software. Founded in 2018, the California-based startup has already garnered over $8 million from investors to scale its adoption across the health care industry.

An increasing number of these well-funded ventures aim to disrupt midsize companies by elevating client expectations, who now seek providers that integrate these powerful technologies into their solutions. With neither the speed of the startups nor the cash reserves of the major players, the midsize companies are placed in a difficult position.

How can they fend off the rapidly strengthening challengers without losing their footing?

Thankfully, there are a few wise options CEOs can take to escape the mounting pressure and use the market dynamics to their benefit.

Emergence of cash-rich companies

As companies seek to compete for the largest health care contracts, there have been impressive buyout multiples for health care supply chain and logistics deals.

In just the past few years, logistics provider Lifestage Solutions sold to Galencia Group for over 5x revenue. Similarly, health care procurement company Aknamed sold to PharmEasy for $144 million, despite only $3 million in revenue.

This trend will continue at an accelerated pace as newly acquired health care companies begin consolidating their contracts with the associated supply chain and logistics companies. As the contracts grow in size and scope, the need for rapid acquisition will become increasingly clear.

Private equity’s aggressive investments in health care supply chain companies help fuel this opportunity. Notably, 40% of the past decade’s investments have happened after 2021.

The emergence of these cash-rich acquirers and the formation of a more concentrated health care sector create a ripe environment for midsize companies to embrace consolidation of the health care supply chain industry.

CEO options

To be well suited for continued success, health care supply chain and logistics companies will need to adapt to the changing conditions.

For large companies such as Global Healthcare Exchange (GHX), the path is fairly straightforward: Use the advantage of their deep pockets to buy health care logistics providers. In early 2022, GHX bought the AI-enhanced inventory control company Syft for an undisclosed amount, its third acquisition in recent years.

Moreover, in mid-2022, GHX announced a collaboration with the Healthcare Industry Resiliency Collaborative to form an increasingly resilient and transparent supply chain for the industry, hinting at additional acquisitions.

For small companies, such as Vamstar and Notisphere, the path to survival is to use their recent injections of investor cash to scale and challenge midlevel competitors. Successful implementation of this strategy requires the speed, vision and investment already commonplace among the growing number of health care supply chain startups.

For midsize companies, on the other hand, which lack the dynamism of a startup and the establishment of a large company, there are three main options: (1) invest heavily into organic growth and substantial differentiation, (2) buy even smaller companies for rapid, inorganic growth, or (3) find a larger company with cash reserves that could facilitate a sale, merger or strategic partnership.

One such company, the Mexico-based firm Medistik, embraced the third option and enjoyed a $77 million sale to Grupo Traxión in 2022 to help integrate their pharma vertical to 4PL and last-mile logistics services.

On a larger scale, the Italian firm Bomi Group, specializing in logistics for health care product distribution, sold to UPS for $884 million in mid-2022. Both firms noticed the evolving market conditions and adapted to the trends by finding larger companies with deeper pockets that could acquire them to enhance their services and meet the health care sector’s needs.

Alternatively, a company could reject all three options and stay the course. However, for a dynamic industry experiencing rapid restructuring and massive technological progress, this choice doesn’t suggest a recipe for success.

Rather than taking their survival for granted, the winners will be those who cooperate with and respond effectively to the evolutionary forces at play, using the three key options as guidelines for growth.

BG Strategic Advisors’ David Fleming contributed to this report.

About the author

Benjamin Gordon, managing partner at Cambridge Capital, is a leading investor in the supply chain and technology sector. His investments include companies like Bringg, XPO and ReverseLogix. Before Cambridge Capital, he founded BG Strategic Advisors, a top investment bank in transportation and logistics, and 3PLex, an internet solution for logistics companies. Gordon is a published author, recognized expert and active civic leader, contributing to numerous nonprofit organizations. He holds an MBA from Harvard Business School and a BA from Yale College.