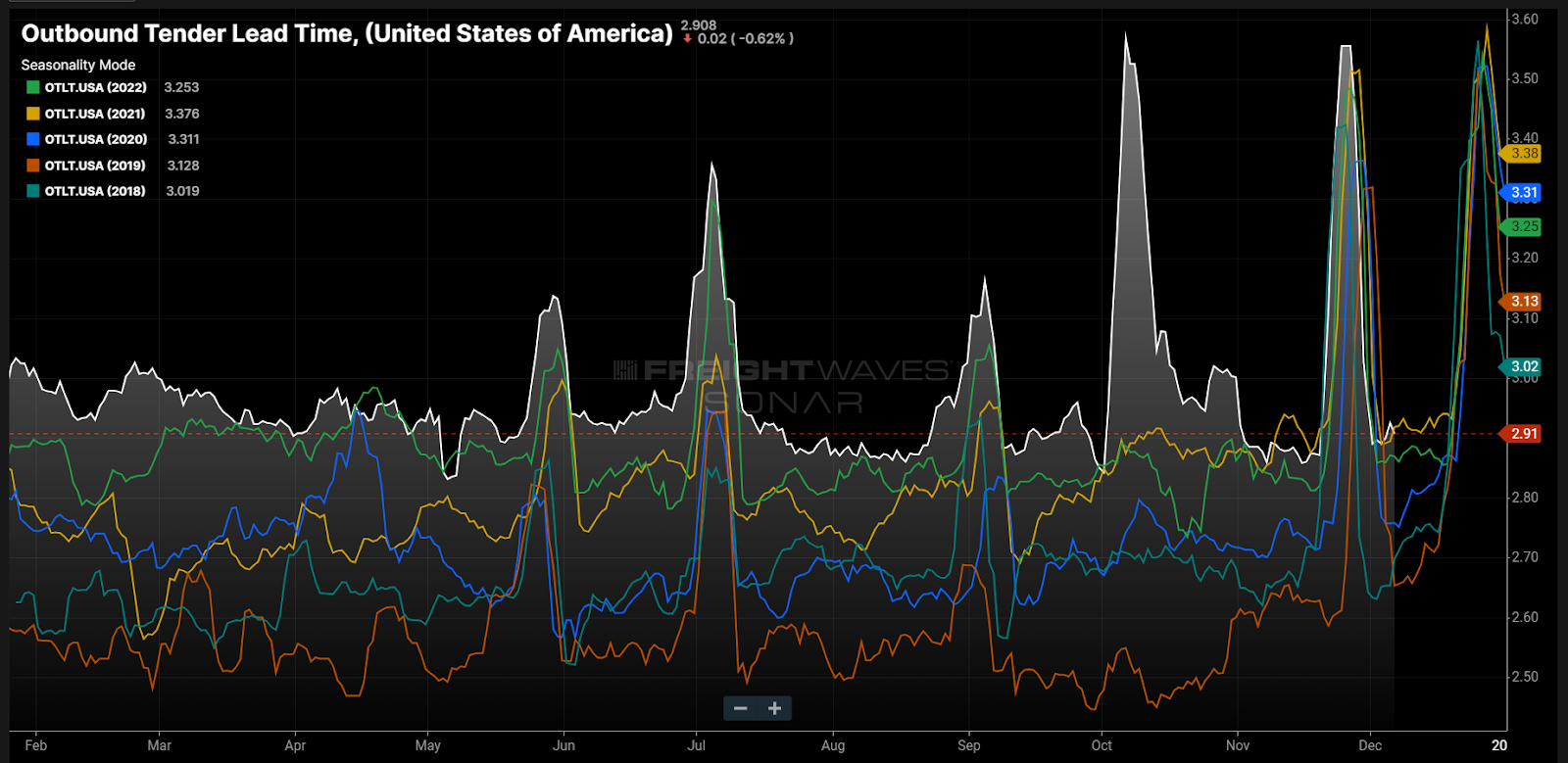

Chart of the Week: Outbound Tender Lead Time, USA SONAR: OTLT.USA

Tender lead times — the time between the initial request for truckload capacity and the requested pickup date — have remained 10-15% above pre-pandemic norms throughout 2023. This has been the one transportation management trend that has stuck and not regressed since the end of the shipping boom. It is also a trend that benefits both shipper and carrier.

Lead times have an optimal range depending on the origin. Generally speaking, a three- to five-day lead time gives a carrier plenty of time to prepare and adjust its networks to make a pickup, even in some of the more remote areas.

Lead times spike in front of holidays as shippers push orders for the future before they leave the office.

When lead times shrink rapidly, it can be an indication that shippers have had unexpected demand spikes. Gradual moves in lead times are more dependent on shipper expectations of capacity availability. This current pattern does not fit historical patterns.

National lead times (OTLT) averaged around 2.6 days in 2019, which was the shortest amount of time of the past five years.

So far in 2023, the OTLT has averaged just under three days. A half day may not seem like much, but think about it in terms of potential miles a truck drives in that time. The 0.4 days is roughly 200 miles or slightly longer than the distance from Chicago to Indianapolis for a truck.

Shippers typically average shorter lead times in soft markets because they know capacity will be available.

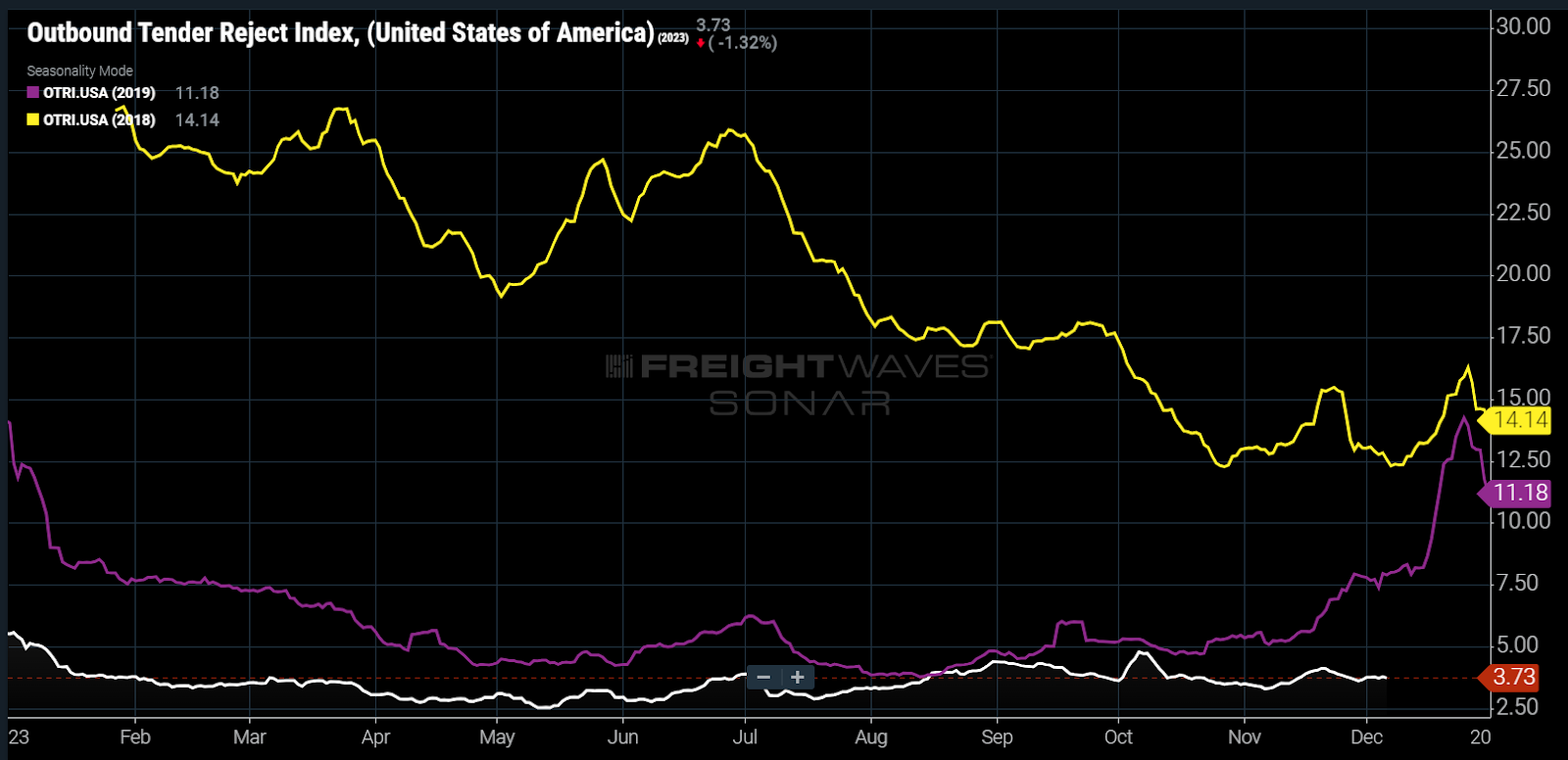

This is supported by the fact that lead times fell 3.3% from 2018 (a relatively tight market) to 2019 (a very loose market). They subsequently increased in 2020-22 and have remained elevated in 2023 even as the market loosens.

The National Outbound Tender Reject Index (OTRI), which measures the rate at which carriers turn down requests for truckload capacity, shows capacity was significantly harder to secure in 2018 than in 2019 (purple) and this past year (white). Higher rejection rates equal tighter capacity.

One would expect this year’s lead times to be similar to 2019, except they are 8% higher than 2018. So why has this trend stuck?

It is nearly impossible to pin down, but shippers may have realized the benefits of giving more time for carriers to prepare after two years of struggling. Service levels were abysmal in 2020-21, but some companies probably noticed their odds improved with more days to prepare.

This could also be a byproduct of shippers own internal processes changing. Inventory management has been a primary focus over the past few years. Shippers may have improved their planning and warehouse management practices, leading to better visibility on when to ship.

Shippers may also lack the sense of urgency due to having relatively elevated inventory levels. This means they can ship at their leisure due to a lack of urgency.

More than likely it is a combination of all of these and possibly more. The good news for carriers is that it appears to be sticking regardless of market conditions. This practice will definitely help shippers when the market inevitably turns the other direction.

About the Chart of the Week

The FreightWaves Chart of the Week is a chart selection from SONAR that provides an interesting data point to describe the state of the freight markets. A chart is chosen from thousands of potential charts on SONAR to help participants visualize the freight market in real time. Each week a Market Expert will post a chart, along with commentary, live on the front page. After that, the Chart of the Week will be archived on FreightWaves.com for future reference.

SONAR aggregates data from hundreds of sources, presenting the data in charts and maps and providing commentary on what freight market experts want to know about the industry in real time.

The FreightWaves data science and product teams are releasing new datasets each week and enhancing the client experience.

To request a SONAR demo, click here.