Absolute capacity is returning to the market. I spend a lot of time writing about the impacts of relative capacity on the CPG space, which is extremely important, but have yet to mention absolute capacity. Absolute capacity refers to the total number of trucks that are available for hauling goods whereas relative capacity refers to the relationship between volume and capacity. In other words, absolute capacity is the ‘supply’ side of the trucking marketplace, where relative capacity is the balance between supply and demand.

One of the best existing leading indicators for which direction absolute capacity is headed is new Class 8 truck orders. While order numbers themselves don’t indicate whether the tractor is destined for a dry van, reefer, flatbed, specialized—or even private—fleet, they are still an extremely important data point.

Here at FreightWaves, we believe that 23,000 new trucks per month is the amount of trucks that need to be purchased each month to keep absolute capacity at current levels, the so-called ‘replacement rate’. We get to this number by estimating annual replacement demand at 275,000 trucks per year and dividing it by twelve.

As is apparent in the chart above, new truck orders were well below the 23,000 level for all of 2019 through September 2020. For the majority of this period, trucking had one of the most difficult periods in recent memory. The largest truckload bankruptcy in history, Celadon Group, occurred on December 11, 2019 which employed more than 3,200 drivers.

New Class 8 truck orders have exploded over the past month, a positive for shippers throughout the country. The most important thing to note is that these are just orders and it will take approximately six months for these trucks to be delivered to carriers. Relative capacity will be tight for the foreseeable future due to a multitude of reasons including strong volumes, heightened regulations, and a lack of drivers.

What does this mean for transportation managers? Although capacity is returning to the market, it is going to be a drawn-out process. Shippers, you can expect tight capacity and higher rates through the end of the year and through the first half of 2021. Carriers, you will have plenty of opportunities to take advantage of higher rates.

Grocery volumes see heightened intra-month volatility. Convoy’s Director of Economic Research Aaron Terrazas wrote a very interesting blog last Wednesday that highlighted some peculiar spending patterns that have emerged over the past three months.

Consumer packaged goods are essential to every human across the globe and even a pandemic will not change this fact. What can change is consumer spending patterns. Over the past three months, there have been noticeable and more prominent drop offs in grocery spending at the end of the month and spikes in grocery spending at the beginning of each month.

Terrazas believes—and I agree—that this phenomenon has to do with consumers’ wallets running dry at the end of the month and being replenished at the beginning of each month. Families stock up early, then pare their spending back for the remainder of the month.

As recently as Tuesday afternoon, there seemed to be additional aid coming to help Americans, but President Trump announced that he will refuse to sign the bill until direct payments are increased from $600 to $2,000 per person. Although more money in consumers’ pockets is a positive for consumer spending and the overall economy, any delay in relief could prove detrimental to the economic recovery and only deepen this unconventional spending pattern.

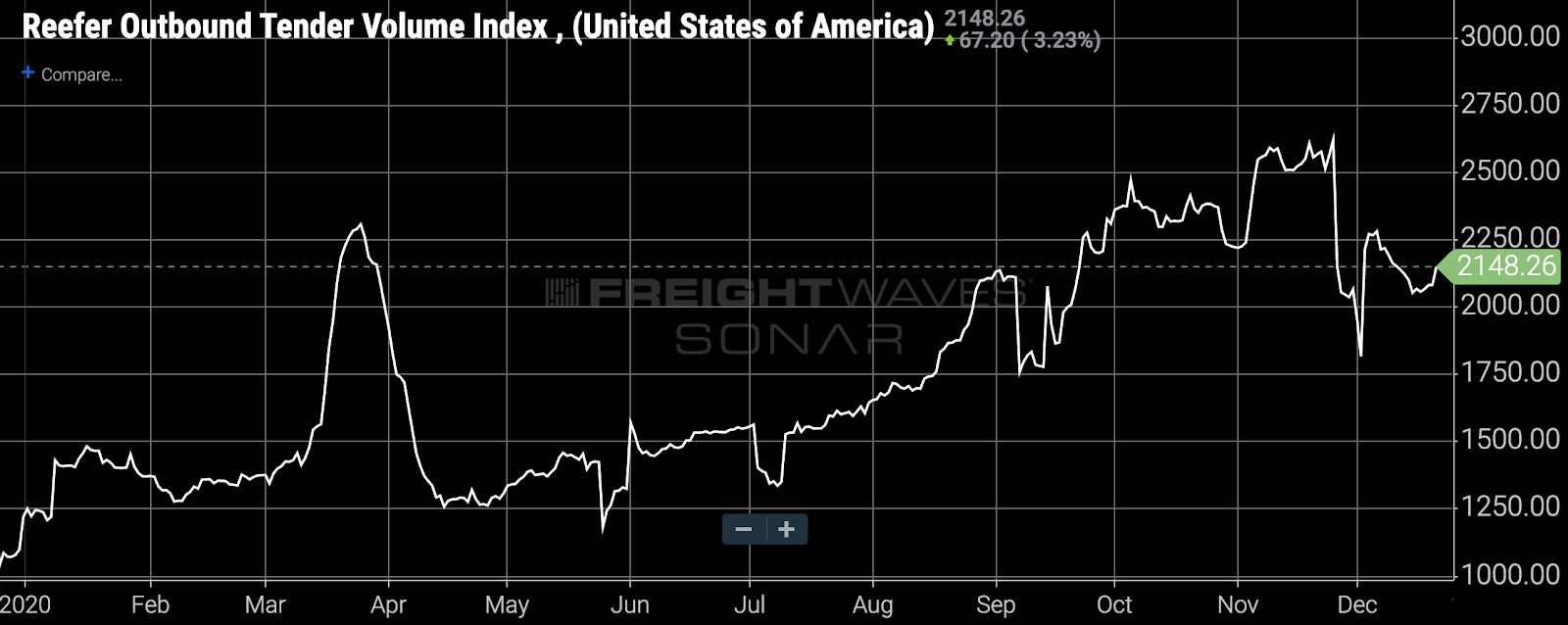

Reefer tenders have been on a rollercoaster ride throughout 2020, starting with the extreme “panic-buying” experienced in the middle of March through the beginning of April as consumers worried that there were going to be total lockdown measures along with food shortages.

I had concerns that there was going to be a repeat of panic-buying as the third wave took hold in the latter half of October, but there has been much less panic and stores have been relatively well-stocked, which speaks to the improvements in supply chains that CPG companies have made since the spring.

“It certainly has not emerged,” Terrazas told me in an interview when talking about whether he was seeing the same level of panic-buying as seen in the spring. “So much of what drove the panic-buying in March was the fear of the unknown—and obviously there are still unknowns—but there is not the wild speculation about closing state borders and the drastic stay-at-home orders that we saw in the spring.”