Now that is an ad!

If you haven’t seen it yet, I’m going to waste two minutes of your time: Please check out the “Mean Girls” Walmart ad here. I’ll wait — The Stockout will still be here when you’re done. Who needs to buy Super Bowl advertising space with something so sharable? A few takeaways:

- It’s all about driving growth in Walmart Plus subscribers! Giving customers early access to Black Friday deals is the latest and, for many, best reason to sign up. Other benefits include “scan and go,” special rates at select gas stations, and free delivery from your local store. So, it’s a competitive response to both Amazon Prime and Costco at once. Adding Walmart Plus subscribers as well as driving general app downloads unlocks potential for targeted advertising, growth in e-commerce and share gain. There is also the psychology of subscriptions — customers shop where they have a subscription just so they don’t feel bad about paying for an unused subscription. I think once more consumers realize that Walmart delivers high-quality fresh foods as part of their subscription along with everything else, its e-commerce sales will really take off across demographics — the edge they have on Amazon is in grocery.

- Walmart’s Black Friday starts a whopping 16 days before Black Friday. That seems like a competitive response to the second helping of Amazon Deal Days. For freight it probably also supports the view that the peak season was pulled forward, as was discussed in the latest State of Freight.

- Highlighting Lego bricks for Black Friday was smart because they are stupidly expensive for what they are.

- Lacey Chabert (Gretchen Wieners) hasn’t aged a day in 20 years. I know — right? She needs to tell us what sunscreen to buy.

- My son (just under 2) would probably love the radio-controlled Teenage Mutant Ninja Turtles skateboarder.

Selling profitably on Amazon Marketplace possible, but not easy

(Photo: FWTV)

On Monday’s The Stockout show, I interviewed Chris Moe, CEO of Cartograph, a company that helps brands grow on Amazon and Instacart. While the recent lawsuit brought against Amazon by the Federal Trade Commission and 17 state attorneys general shed public light on the challenges that sellers on Amazon Marketplace face, Cartograph has long been helping sellers navigate those issues. Remarkably, more than 90% of Cartograph’s clients sell profitably on Amazon — that’s even more impressive considering that most are selling consumable items, a category that is notoriously difficult to sell profitably on Amazon.

Here are a few takeaways:

- Upstream techniques, such as designing products and packaging that fit well into Amazon’s logistics network, are far bigger determiners of profitability on the site than anything that can be done in regard to optimizing search results and page views.

- Amazon applies its favored nation price-matching inconsistently and seems to be deliberately unspecific about what the rules are. One strategy that some sellers employ is to act as though their products won’t be price-matched, until they are.

- Amazon does not price-match against direct-to-consumer sites. Rather, it applies price-matching to other superstores sites, such as Walmart, Target and Kroger properties.

- Sellers often introduce unique SKUs to be sold on Amazon. The uniqueness makes it more difficult for Amazon to price-match, but the retailer will sometimes price-match anyway by converting unique SKUs to a price per ounce.

- Moe also helps sellers grow their brands on Instacart, and he believes that the service, which involves hiring a personal shopper, will likely remain a niche because of its premium status (although consumers can now use the Supplemental Nutrition Assistance Program for the service). However, he likes the company’s strategy of diversifying away from grocery into other categories that can often be more time-sensitive.

See the full interview here.

Amazon’s shift to regional fulfillment model has gone better than expected

(Barchart.com Inc.)

In April, Amazon announced that it had completed a shift from a national fulfillment network to a regional fulfillment model, using eight distinct regional networks, to reduce handling cost, increase shipment consolidation and increase delivery speeds. Management described the process as one of the most significant changes to its fulfillment network since its inception. Half a year later, early results have exceeded initial expectations.

To support this effort, the company touts improved connectivity between fulfillment facilities and continued improvements in placement algorithms. Previously, using a national fulfillment network, items sometimes needed to be transported across the country when they were not available locally in the region where they were ordered.

For sellers on Amazon Marketplace, such as CPG companies, that potentially means needing higher inventory levels since they will have to maintain inventory in eight regions to qualify for Prime — which is critical since Prime customers buy about four times as much on the site as non-Prime members. For competing retailers, it means that the bar for fast deliveries is rising even higher — few retailers have the scale to offer such a wide array of products so close to consumption. Walmart is the notable exception.

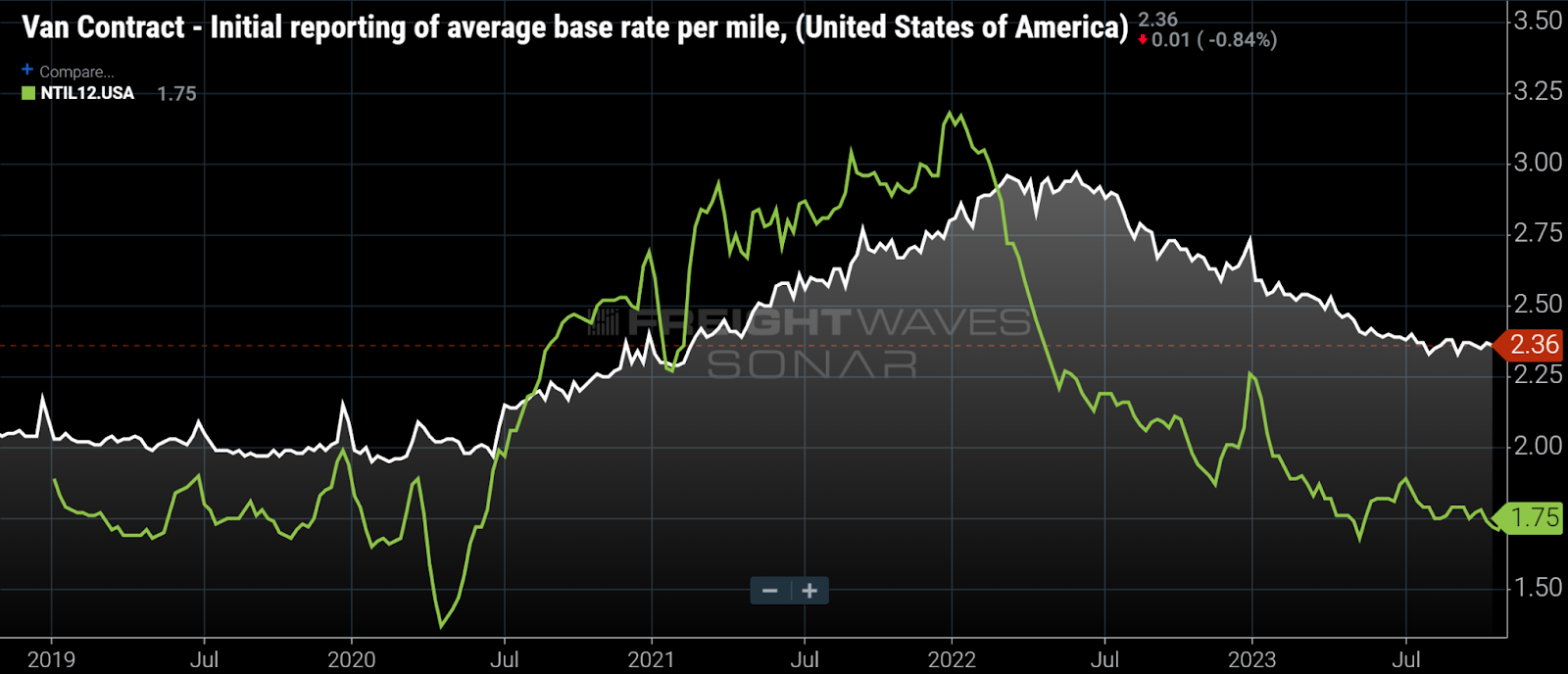

State of Freight webinar highlights capacity overhang that is likely to persist

The spread between contract rates (white) and spot rates (green) is set to decline with spot rates approaching a floor and contract rates being rebid to lower levels. (Chart: SONAR)

I recommend going back and viewing the full webinar and/or at least reading John Kingston’s summary. Since this newsletter is written primarily with shippers in mind, here are a few takeaway from their perspective:

- Freight demand increased in Q3, which is unusual seasonally. But, rather than representing true growth in freight demand, it appears to have been a sign of an early peak season.

- Despite an elongated period of loose freight markets, a tightening doesn’t seem imminent. While freight demand has held up remarkably well considering pressures on the consumer and sharply rising interest rates, excess capacity that came into the market following a tight freight market and an interest rate at zero during the early years of the pandemic is the main reason why freight markets remain loose. FreightWaves CEO Craig Fuller estimates that another 20% of capacity needs to come out of the freight market in order to see tightening. Capacity has exited the industry only slowly — at the current pace, capacity could take another year or longer to come into balance with demand.

- Shippers are in the driver’s seat for the upcoming bid season, which is most active in the fourth and first quarters. Therefore, contract rates in 2024 are likely to be below 2023 levels on top of a year-over-year decline this year.

- Some carriers are parking trucks “against the fence” since rates in certain lanes are low enough that carriers are not incented to put more miles on their equipment. That suggests that latent capacity could be redeployed once the freight market turns around some, muting the impact of a freight market recovery.

- Rail intermodal has taken some share back from long-haul truckload in response to improved rail service levels, falling intermodal rates and goods becoming less time-sensitive. But that is unlikely to significantly impact the truckload market because intermodal is a relatively small niche within the domestic surface transportation industry.

To subscribe to The Stockout, FreightWaves’ CPG and retail newsletter, click here.