When we look back at the COVID era, we will remember stockouts of toilet paper, cleared-out grocery store shelves and the impossibility of getting the latest video game console because of the semiconductor shortage. Today, consumer goods are still serving as a reminder that COVID is not fully behind us. Just as there are still McCormick products that haven’t returned to shelves, the headline-grabbing CPG news items this week related to a shortage of individual ketchup packets. That one is so intuitive that it is amazing to me that it took this long for it to emerge.

Elsewhere in CPG news, there is additional evidence of inflation pressure in Conagra’s results, meat products may be the most vulnerable grocery category as consumers return to restaurants, and General Mills looks to cut back on manufacturing capacity provided by third parties.

To sign up for The Stockout, a newsletter focused on CPG supply chains, please click here.

Proving that the pandemic is not over, single-serving ketchup packets are in short supply. That news story this week is an intuitive result of restaurants shifting to takeout and removing shared ketchup bottles from tables. That brings back memories of the early days of the pandemic when there were excesses and shortages of the same product at the same time — such as kegs of beer spoiling while beer in cans and bottles was in short supply. Still, I can’t say that I noticed restaurants rationing ketchup packets. Maybe more consumers will come around to eating hot dogs the Chicago (and the correct) way — by never putting ketchup on a hot dog.

Some interesting points from this news story:

- Retail ketchup sales increased about 15% in 2020 over 2019.

- Individual packet prices are up 13% since January 2020.

- Long John Silver’s had to buy from secondary suppliers.

- Kraft-Heinz, which has ~70% share of retail ketchup, is running extra shifts on existing manufacturing lines, is opening three additional manufacturing lines to increase production by ~25%, and has shifted resources to single-serving production.

Even if COVID’s impact is winding down, inflationary pressure may just be getting started. Conagra Brands reported earnings Thursday and its comments on cost inflation stood out to me. Conagra’s cost inflation was 3.9% in the quarter, whereas earlier in the year, it had been a more manageable 2.5%. Cost inflation is an issue in line items across the board, and the company cited specific cost inflation in materials (up 3%), manufacturing costs (up 4%), and transportation and logistics costs (up 8%). In addition, the company cited a $15 million increase in transportation and logistical expenses to increase its supply of products to stores.

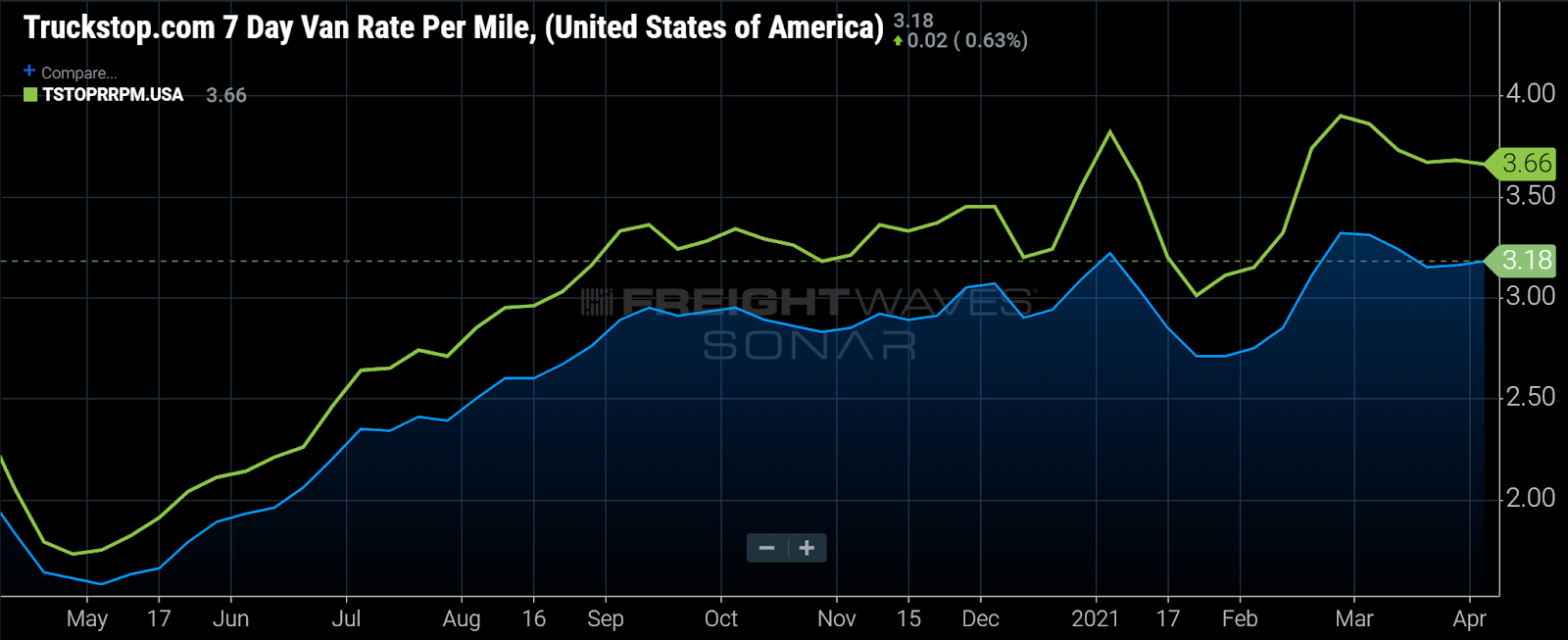

A one-year chart of dry van (blue) and reefer (green) spot rates highlights inflation in freight costs.

(Chart: SONAR; weekly spot rates including fuel surcharges, as reported by Truckstop.com, are shown above for dry van and reefer in blue and green, respectively.) For more information on SONAR or to request a demo, click here.

Among grocery categories, meat might have the furthest to fall. Most CPG companies are preparing for at least a partial return to normal, but it is unclear how sticky the newfound consumer habits will be and which CPG categories will be most impacted. Data company Numerator has attempted to address that question for food categories as it launched its Grocery Vulnerability Index.

According to Numerator, meat is the most vulnerable grocery category (50% more vulnerable to a severe sales decline than the average grocery category) followed by herbs/spices and condiments, which are 46% and 19% more vulnerable than the average category, respectively. The assertion that meat is one of the most vulnerable categories to the reopening of restaurants is supported by the unusual 2020 growth. Last year, meat sales grew 19.2% on a volume increase of 11%. For comparison, most of the large CPG companies reported sales increases in the high single digits for their segments that target in-home consumption.

Among meat categories, beef saw the most growth last year and also captured the most protein dollars. Interestingly, meat was also one of the categories that made the most progress in expanding e-commerce penetration in the past year. According to IRI, meat e-commerce increased 90% in the past year and now represents 10% of total meat purchases.

General Mills’ manufacturing outlook suggests that the company expects demand to moderate. General Mills expects to see mid-single-digit freight cost inflation as, like most CPG companies, it contends with inflation in ingredients and packaging, among other areas. This week, we gained insight into how the company may offset some of that inflation. Specifically, the company is looking to reduce external manufacturing once it begins to see demand taper off.

The company utilized more expensive external manufacturing to handle the stay-at-home demand surge, which is associated with a 10%-15% gross margin reduction on associated revenue. While the company still expects demand to settle in above pre-COVID levels as more consumers work from home permanently, it seems to expect, as most analysts do, that the partial return to normal will lead to at least a partial reversal of the fortunes seen during the COVID lockdowns.

To receive The Stockout, CPG-focused newsletter, please click here.