A year ago, shipping experts unveiled their projections for 2020. Little did they know how short their forecasts’ shelf lives would be. Pre-COVID outlooks were practically worthless by February.

The pandemic reshaped cargo demand across all shipping segments, but for two in particular: container shipping and tanker shipping.

In both cases, COVID had a violent effect on demand — up then down for tankers, down then up for containers. And in both cases, initial expectations on rate effects were wrong.

The following is a look back at American Shipper’s coverage of the crisscrossing roller-coaster rides for container shipping and tanker shipping in 2020.

Container shipping: The fall

At first, analysts feared catastrophic COVID fallout for container lines. It turned out to be a gold mine. Stifel analyst Ben Nolan dubbed container shipping “the surprise rock star of 2020.”

The pandemic cycle began with a cargo supply side shock: the abrupt shutdown of the Chinese export system in January and February (see story). This caused box volumes at sea to suddenly collapse (see story).

But the Chinese supply side shock was short-lived. Factories came back online quickly (see story) and outbound volumes rapidly rebounded (see story).

The bigger threat to container shipping was the cargo demand shock from COVID lockdowns in Europe and the U.S. This spurred concerns in March and April that volumes could collapse even more so than during the financial crisis (see story) and that carriers could face “life-threatening” financial losses (see story).

However, unlike in previous demand slumps, carriers deftly controlled their capacity (see story). They “blanked” (canceled) up to 20% of sailings on mainline trades (see story) in the second quarter. They refrained from price wars and used blank sailings to bring ship capacity in line with lockdown-stricken demand.

Container shipping: The rise

As a result, the disaster scenario for carriers was averted. It became clear that carriers would minimize their losses. Then came another surprise: Cargo demand roared back in the second half, causing freight rates to skyrocket (story here). Carriers were not just going to minimize losses; they were going to rake in huge profits (story here).

A confluence of factors drove demand: restocking to replenish inventories (story here); holiday cargoes (story here); a shift from retail-store sales to e-commerce, pushing more time-sensitive cargoes through the West Coast (story here); and perhaps most importantly, a shift by consumers toward spending money on goods that they’d previously spent on services — supported by fiscal stimulus that allowed consumers to keep spending despite massive job losses.

The dramatic rebound in cargo demand caught ocean carriers by surprise. They reinstated all previously blanked sailings. They also chartered as many extra vessels as they could, pushing charter rates “through the roof” (story here). Today, there are few ships left to charter — the global fleet is effectively maxed out.

The capacity crunch for container equipment has been even worse than for ships. Containers have been called “the new gold” amid a “black swan” box squeeze (story here).

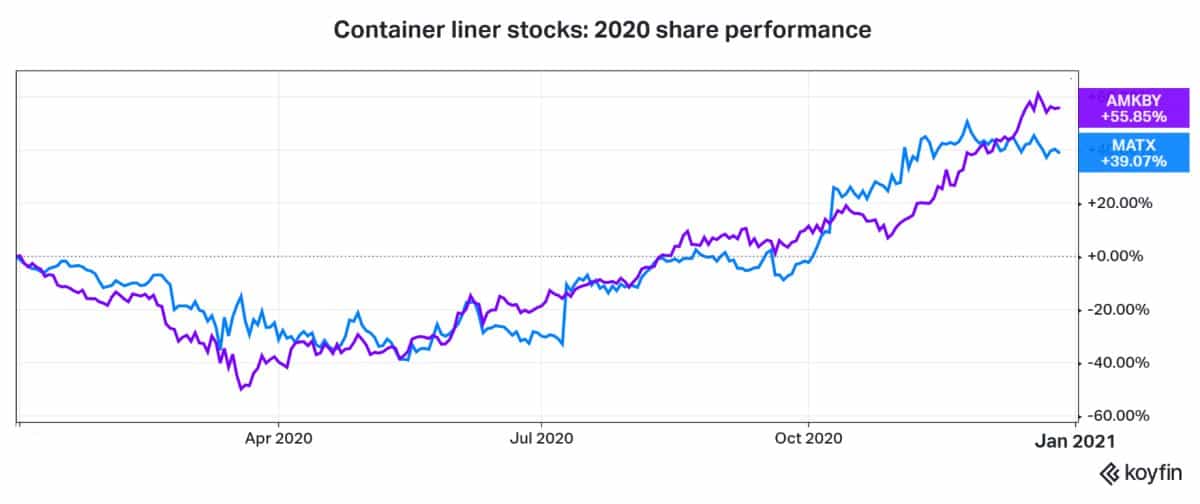

As 2020 comes to a close, the cargo boom remains in full swing. Container industry stocks are riding high (story here). As of Monday, the shares of Matson (NYSE: MATX) and the American depositary receipts of Maersk (OTC: AMKBY) were up 39% and 56% year to date, respectively.

The big questions for 2021: Will COVID fallout curtail import demand (story here)? Have importers shipped too much this year, leaving them with too much inventory next year (story here)? Will the Biden administration push for even more stimulus, and will vaccines unleash even more demand (story here)?

Is carrier capacity management a structural change, or will it collapse amid the next demand downturn (story here)? If it is a structural change that allows liners to influence rates by managing capacity, will regulators intervene (story here)?

Tanker shipping: The rise

The pattern in tanker shipping is almost a mirror opposite of containers. Many executives, investors and analysts initially thought COVID would be a bonanza for tankers. Instead, tankers are struggling to break even and face an extended slump.

Back in March, COVID caused the price of crude to collapse. That, in turn, sparked a disagreement within the OPEC+ coalition on production cuts (story here). In response, Saudi Arabia began pumping at full throttle (story here). Saudi transport demand pushed spot rates for larger tankers over $200,000 per day (story here).

With fuel consumption constrained by COVID and OPEC+ production surging, excess crude overflowed into floating storage, tying up tanker capacity.

The more tankers used for floating storage, the fewer available to bid on voyage contracts and the higher the spot rates. In late March, Robert Macleod, then-CEO of Frontline (NYSE: FRO), described the floating-storage situation as a “once-in-a-generation” opportunity (story here).

By April, the floating-storage effect was boosting product-tanker fundamentals as well (story here). Given COVID fallout to fuel demand — particularly jet fuel — refineries pumped out too much petroleum products. Product tankers, like crude tankers before them, filled up with storage cargoes.

Tanker shipping: The fall

But spiking rates and stock sentiment fizzled faster than expected. Shares of Nordic American Tankers (NYSE: NAT) jumped (temporarily) in April, but larger-cap tanker stocks generally underperformed even as rates rose (story here) — purportedly because institutional investors “faded the rally.”

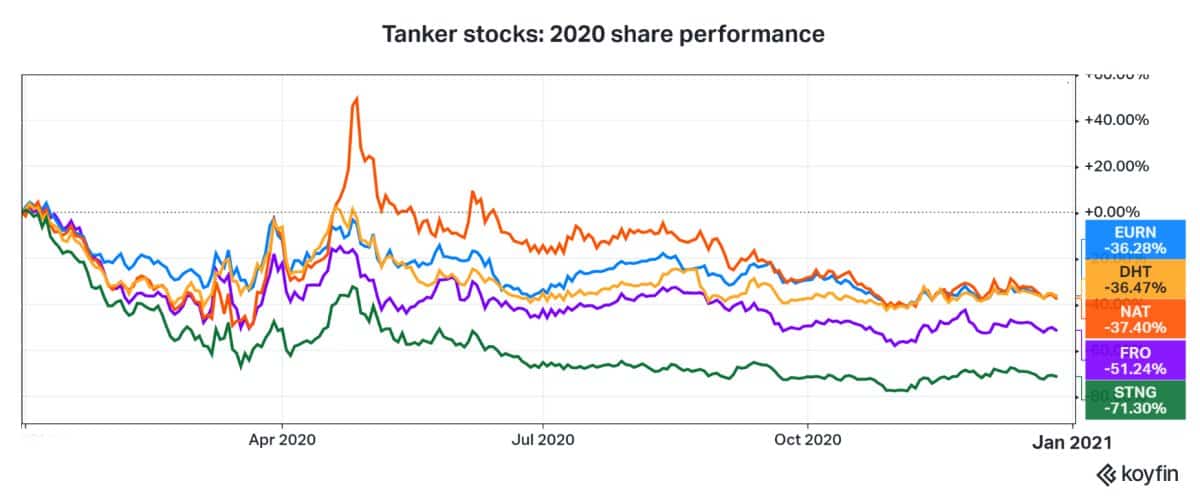

As of Monday, shares of DHT (NYSE: DHT) and Euronav (NYSE: EURN) were down 36% year to date, Nordic American Tankers 37%, Frontline 51% and and Scorpio Tankers (NYSE: STNG) 71%.

What happened to tankers in 2020?

First, the OPEC+ dispute was short-lived: production cuts resumed in May (story here). Second, oil prices began recovering in May, undermining incentives for traders to put oil in floating storage. Floating storage stopped building faster than expected (story here). Third, transport demand began to weaken seasonally in June, prompting rates to collapse (story here).

As the floating-storage thesis crumbled, tanker owners and analysts refocused on a post-floating-storage thesis. A rapid economic recovery would theoretically pull down floating inventories fast; the market would then revert to normal dynamics, and the recovery would drive higher transport demand.

It didn’t happen. Rates crashed further in September, sinking below operating expenses (story here). Demand has not rebounded, with air-travel shortfalls a continuing headwind. Floating storage did not unload quickly, leaving a stubborn overhang on transport demand (story here). And while there has been some winter uplift, late-2020 rates are down precipitously from five-year averages (story here).

The tanker outlook for 2021 is a reverse image of the container outlook. Just as there are risks but no clear end in sight for the container boom, there are opportunities but no clear recovery in sight for tankers. Some analysts don’t see a tanker market rebound until 2022.

Then again, tanker markets can spike overnight on surprise geopolitical events (see story here). And shipping experts’ annual outlooks can turn out to be completely wrong, just as they were a year ago. Click for more FreightWaves/American Shipper articles by Greg Miller