U.S. Xpress Enterprises Inc. (NYSE: USX) reported a fourth-quarter adjusted loss of 5 cents per share, ahead of analysts’ estimates for a 9-cent-per-share loss.

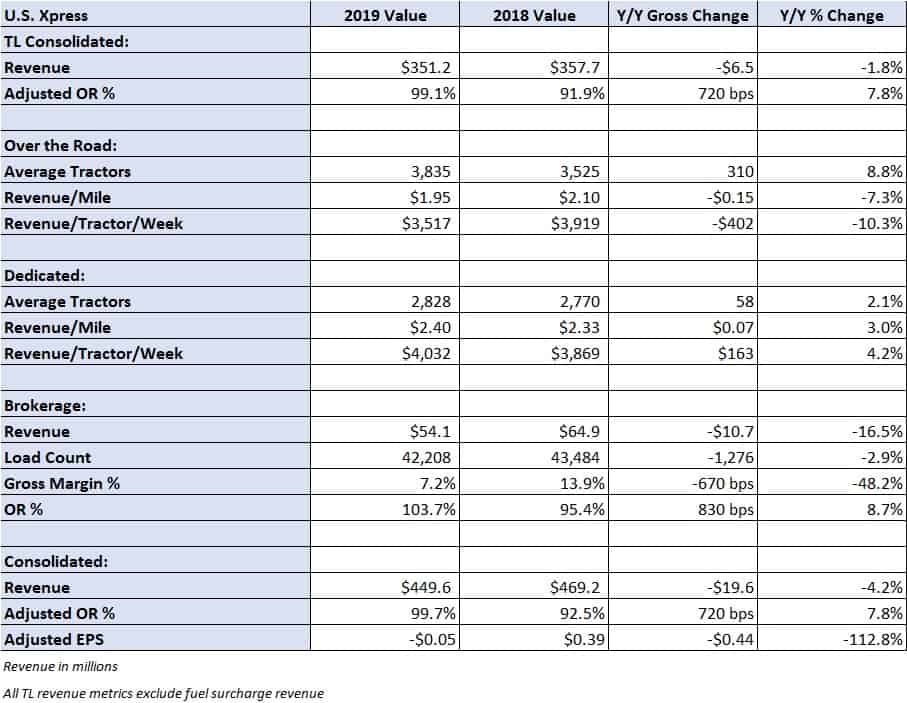

The Chattanooga, Tennessee-based truckload (TL) carrier reported a 4% year-over-year decline in total revenue to $450 million. TL revenue was 2% lower, with brokerage revenue falling 17%.

“Our fourth quarter results were impacted by the continued challenging market conditions experienced through much of 2019, posing a headwind to our financial results. Despite the market backdrop, I am very encouraged with the many successes that our team achieved this past year, as we made significant progress advancing our strategic initiatives focused on delivering improved efficiency,” stated U.S. Express President and CEO Eric Fuller.

Regarding their 2020 outlook, U.S. Xpress expects “slow growth in industry-wide truckload shipments” with truck capacity continuing to exit the market. The company believes the combination will lead to an inflection point in price during the year. However, the press release reiterated that the first quarter is usually the weakest of the year as revenue declines and costs remain elevated.

“While we see positive trends in certain areas, there continues to be uncertainty in the short-term environment, which will impact the actual sequential margin deterioration in the first quarter. We continue to believe that market conditions will improve in the back half 2020. The timing and magnitude of market changes will have a significant impact on our quarterly results given our substantial operating leverage.”

In the third quarter of 2019, Fuller said the company would continue to add tractors to the fleet on the expectation that capacity would continue to exit the market in 2020 and rates would firm. In the fourth quarter of 2019, U.S. Xpress reported that the tractor count had increased 368 units on a year-over-year basis, with the over-the-road (OTR) fleet growing 9% and the dedicated fleet up 2%.

Revenue per tractor per week declined 10% year-over-year in the OTR segment to $3,517 as rate per mile was 7% lower at $1.95. The company’s dedicated trucking division saw continued improvement with revenue per tractor per week climbing 4% year-over-year to $4,032 as rate per mile increased 3% to $2.40.

The press release called out an oversupply of truck capacity relative to demand for its OTR services, which resulted in the carrier seeing spot pricing 30% lower year-over-year. This was partially offset by improvement in the dedicated division.

“Our Dedicated division continued to perform very well in the fourth quarter having delivered its third consecutive quarter of record productivity. We were pleased that average revenue per tractor per week remained above $4,000, while we grew the truck count in this division by 2.9% sequentially. The execution in Dedicated through the year has been excellent and consistent with our long-term strategy, which is to continue to grow the business over time as attractive opportunities arise,” Fuller said.

Like most companies with brokerage operations, U.S. Xpress saw continued headwinds in its brokerage segment. Revenue declined 17% year-over-year, primarily due to lower revenue per load as brokerage volumes were only 3% lower. The gross margin on this business was cut nearly in half at 7.2%. The division reported a $2 million loss in the period.

The company ended the year with $123 million of liquidity and $390 million in net debt. U.S. Xpress announced Jan. 28 that it had favorably refinanced its revolving credit facility. The new facility provides increased flexibility and lowers the company’s interest rates.

The company recorded $20 million in net capital expenditures (capex) in January, which was expected to occur in 2019, but the refinancing occurred later than expected.

U.S. Xpress will hold a call to discuss these results with analysts and investors on Thursday at 8:30 a.m.