The systemic decline in U.S. coal production could cost U.S. freight railroads as much as $5 billion, according to a report produced by market ratings firm Moody’s Investment Service.

As coal demand from utilities drops by more than 50 percent by 2030, U.S. railroads could see an estimated $5 billion in lost revenue, which constitutes about 5.5 percent of 2018 industry revenue, Moody’s said in a September 4 report. But if that decline is gradual, such as a thermal coal decline of about 7 percent per year between now and 2030, then the resulting credit impacts to the railroads will be “manageable,” Moody’s said.

U.S. coal consumption is declining because cheap natural gas prices are competing against coal as a generating fuel. Federal mandates for air emissions have also resulted in utilities seeking other fuel sources for power generation.

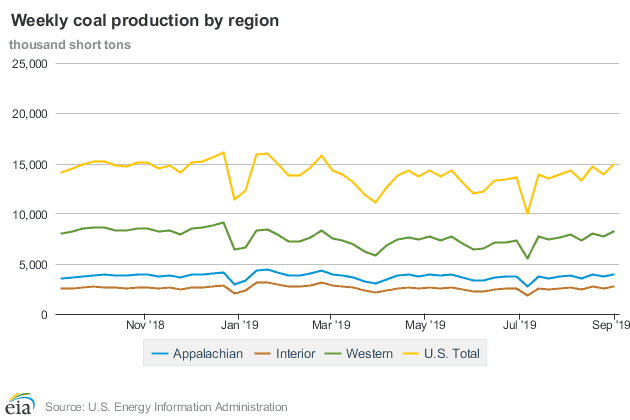

As a result of the power sector’s declining demand for U.S. thermal coal, major coal-producing regions are likely to see lower production levels. Appalachian coal production has already fallen in the eastern U.S., affecting railroads such as CSX (NYSE: CSX) and Norfolk Southern (NYSE: NSC).

But railroads that deliver coal from the Powder River Basin (PRB) in the western U.S. are likely to be more exposed to weakening coal demand, including BNSF (NYSE: BRK) and Union Pacific (NYSE: UNP), Moody’s said.

“PRB coal has a lower heat content than other coal types and its low-sulfur content is less advantageous after utilities were mandated to install scrubbers to reduce emissions of sulfur oxides,” Moody’s said. “Export opportunities of PRB coal are also constrained in view of opposition to proposals for coal export facilities at port locations in the Pacific Northwest, a social risk reflecting growing concerns about the emission of carbon dioxide and pollutants from coal.”

The railroads and coal producers might find some relief in export coal, but the export coal market can be volatile because of the cost structures involved in exporting coal overseas. European demand for thermal and metallurgical coal could also decline as well in the coming years.

“Higher cost structures – including incorporating transportation costs to overseas markets – hinder U.S. exporters of thermal and metallurgical coal to compete effectively in seaborne markets, in particular when prices are low,” Moody’s said. “Railroads have shown a willingness to lower rail transportation costs for export coal when prices are low to help U.S. producers compete with overseas suppliers.”

U.S. railroads might also seek to grow their intermodal volumes to cushion the lost revenue from coal, Moody’s said.

“The recent implementation by most U.S. railroads of operating models based on principles of precision scheduled railroading (PSR) appears to improve rail service levels – including on-time delivery – which is critical for intermodal freight. Intermodal freight tends to be more time-sensitive and demand more frequent service. Sustainable improvement of service levels would help to compete against over-the-road transportation by truck carriers,” Moody’s said.

As coal production faces a probable decline, the railroads will need to assess what to do with the portions of their networks that handle coal deliveries. Their options include seeking other freight that could run on the coal lines, selling the coal lines or abandoning them, Moody’s said.