It may be several months before freight volumes return to pre-crisis levels, but things are looking brighter than last week. SONAR’s Outbound Tender Volume Index (OTVI) has ended its horizontal slide and begun to climb its way back to normalcy. The capacity picture is still lagging and continues to be at historically loose levels, but even though spot rates bounced in a few markets, overall rates are still horrible.

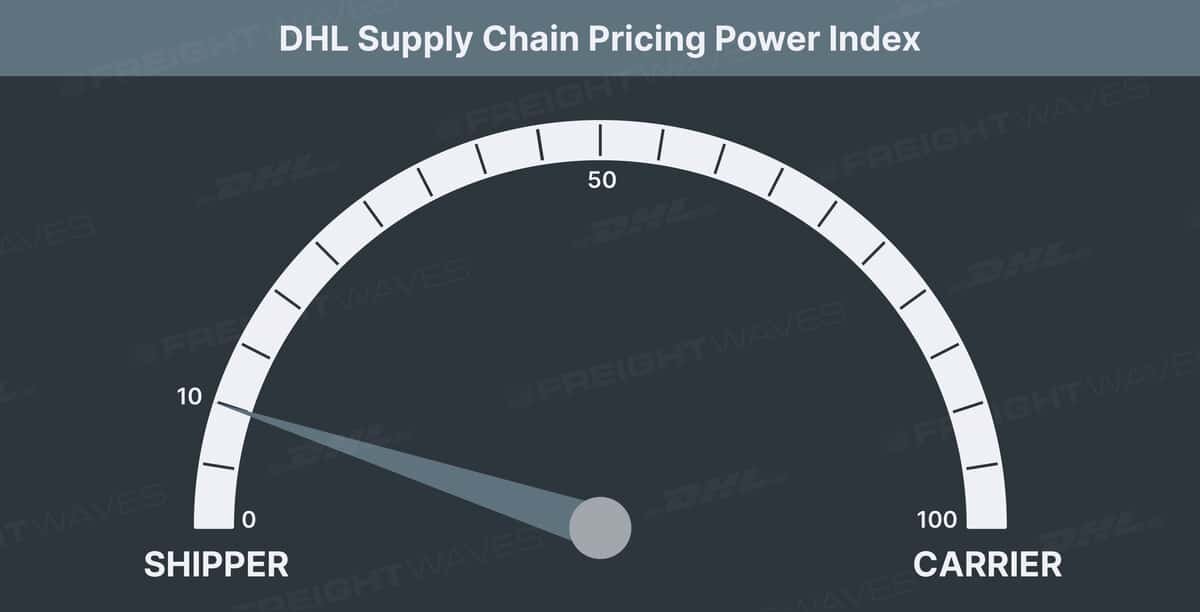

As a result, the weekly DHL Supply Chain Pricing Power Index dropped another five points this week to a reading of 10, suggesting a significant advantage for shippers.

The DHL Supply Chain Pricing Power Index uses the analytics and data contained within FreightWaves SONAR platform to analyze the market and estimate the negotiating power for rates between shippers and carriers. Any reading over 50 indicates pricing leverage for carriers, while readings below 50 give an advantage to shippers.

Load volumes: Absolute levels and momentum neutral

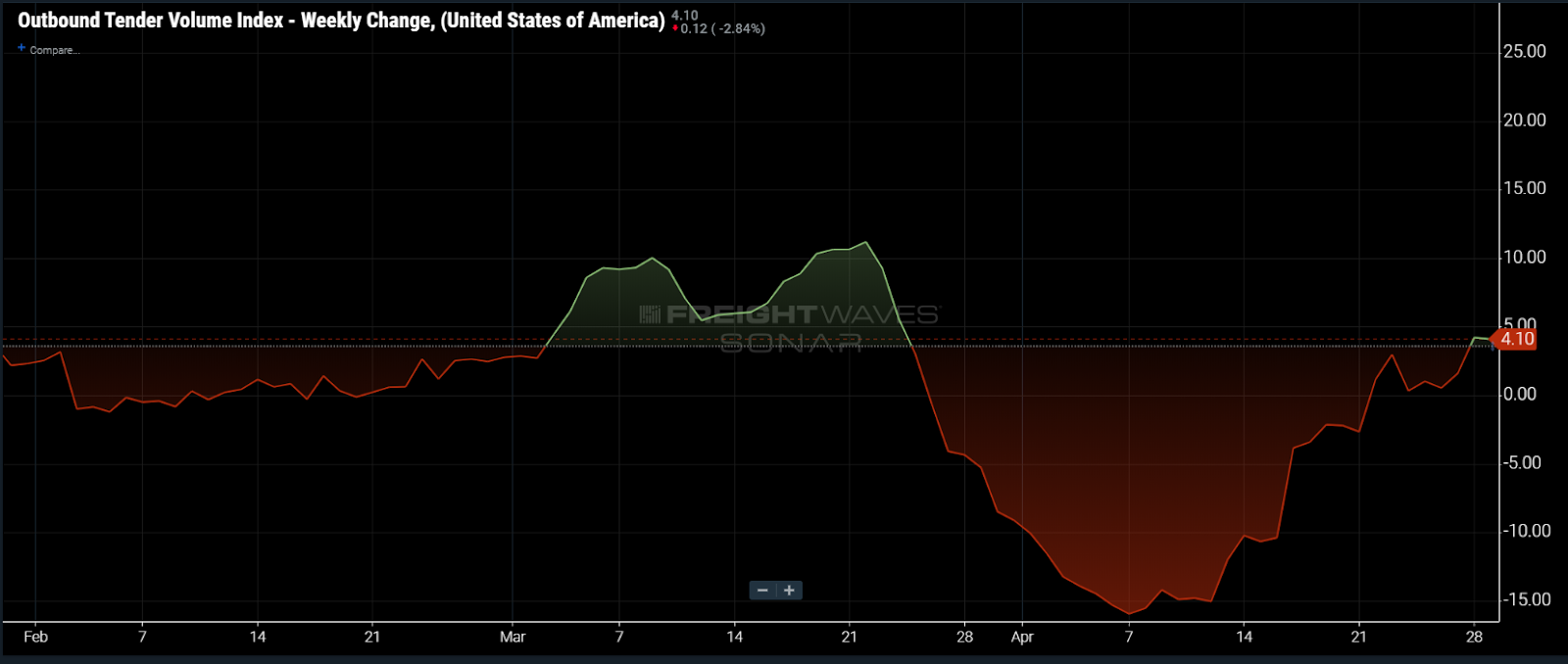

There is life in the Outbound Tender Volume Index (SONAR: OTVI.USA) once again. After two weeks of walking the x-axis, OTVI has turned to the upside. Volumes have risen just over 4% since last week and have broken the 9,000 mark.

Federal social distancing guidelines expired yesterday. Despite warnings from health and disease experts, half of U.S. states are moving forward with relaxing some restrictions. Unfortunately for freight volumes, most of the businesses reopening are service-based and do not move much freight. However, there was encouraging news for freight volumes out of Detroit this week when the major auto manufacturers set a soft reopening date for May 18.

It is not that the auto industry moves a high percentage of domestic freight. But auto producers are well-positioned to create the blueprint for a wider manufacturing reopening. The strong union presence of the UAW and other unions may be able to secure cleaner and safer work environments, as well as enough protective equipment. Also, the inherent structure of auto plants makes them better suited for working through COVID-19 for a couple of reasons. First, the plants are highly automated and workers use heavy machinery, which means they typically are already wearing gloves; secondly, auto plants are much less dense than say an ecommerce fulfillment warehouse or meat processing plant. It is our belief that auto producers can lead the way towards a manufacturing and industrial reopening. The issue will then be demand, which will be damaged by the economic losses of the next few months.

It may be some time before OTVI reaches pre-crisis levels, but parts of the economy reopening and produce season will increase volumes slowly for the next couple of weeks.

Tender rejections: Absolute levels and momentum positive for shippers

The Outbound Tender Reject Index (SONAR: OTRI.USA) has again fallen from a previous series low to an even lower value of 2.59%. This is well below any point in the index’s three-year history.

The index has previously found a support level around 4%, getting close to it but rarely falling below. This is the longest time OTRI has been under that support line, and with volumes at national holiday levels, there is not much pointing towards a rebound.

Since peaking at 19.25% on March 28, OTRI has plummeted more than 80%. OTRI is a measure of carriers’ willingness to accept loads at contracted rates and currently, carriers are moving whatever freight they can find. Contract volumes are beginning to increase, but tender rejection rates will not trend up across the country until capacity is filled in most markets. Currently, this is not the case. Many trucks have been idled and capacity remains loose around the country. The reopening of some industries and the produce harvests will tighten capacity in pockets, but not on a national level.

In terms of pricing power, it is not constructive to either shippers or carriers when volumes are this low. So, to grasp where the power is in this underperforming environment, we must look to pre-crisis capacity, which was already excessive. Although we believe bankruptcies and company failures will reaccelerate during the second quarter, capacity is still very loose right now. Until volumes pick back up, or a swath of drivers leave the market, that environment will remain.

Spot rates: Absolute levels and momentum positive for shippers

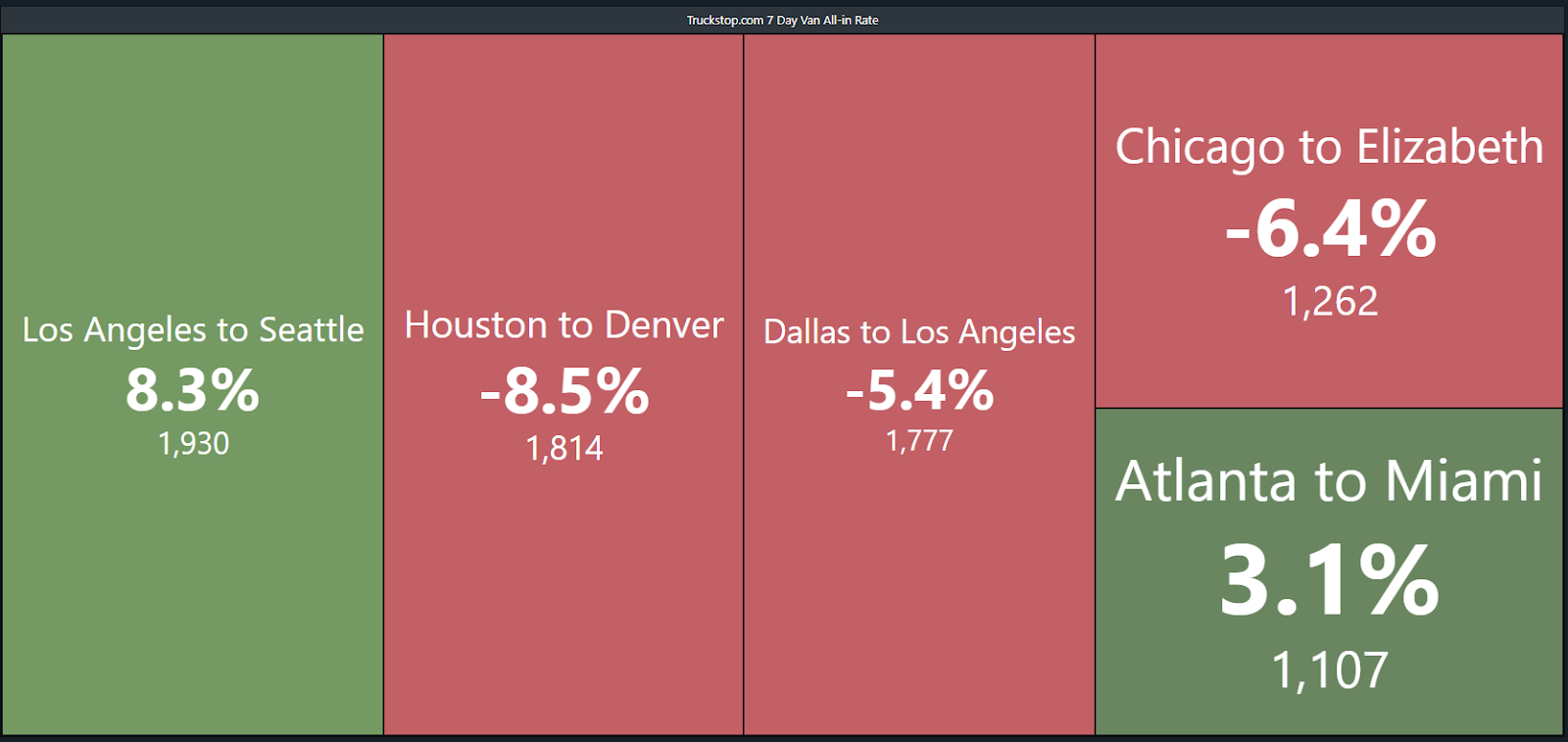

Spot rates have plummeted over the past month, but there are some markets with slight increases over the past week. Whether the pressure is from increased volume or a dead cat bounce is debatable. Either way, it is the first time more than 10 Truckstop.com lanes (SONAR: TSTOP) have been positive week-over-week since March. The picture is slightly brighter, but spot rates remain depressed in the majority of markets as spot volumes have been down significantly.

We have heard stories from drivers who confirmed our belief that spot rates would quickly encroach upon operational costs per mile during April. There will be expectations for grocery, consumer staples and medical supplies, but overall rates will be down considerably on a yearly and sequential basis in April. As FreightWaves’ CEO Craig Fuller noted Wednesday in a SONAR Freight Market Pulse, “Spot market activity won’t return until after the contract market does, so monitoring tender activity gives us a sense of market direction.” And with tender volumes and rejections pointing downward, it will be some time before the contract market returns to normal.

Economic stats: Momentum and absolute level neutral

There were several significant economic releases this week that are worth noting.

By far the most widely watched blockbuster economic data point this week was initial jobless claims, which came out Thursday. Given its frequency, this is one of the best real-time indicators we have.

We just received the jobless claims for the third week of April and they were 3.8 million; this comes on the heels of over 4 million initial jobless claims last week and over 5 million the week before last. This brings the 6-week total to 30.3 million Americans applying for unemployment benefits, which more than wipes out all the job gains since 2009.

To put into context just how high that number is, 2% of the American workforce lost their jobs in a single week, 3-4% of Americans have lost their jobs in each of the previous four weeks. Just in the past six weeks, more than 18% of Americans have lost their jobs. Although initial jobless claims are trending downward, the 3.8 million initial claims are roughly 6 times the previous peak of 665,000 in the 2008-09 recession and the all-time record of 695,000 in October 1982. If there is any good news at all, initial jobless claims fell for the fourth straight week, indicating initial claims have peaked. The unofficial unemployment rate now sits at close to 22%, more than six times the 50-year low of 3.5% from about six weeks ago.

Taking a deeper look at more granular credit card data from Bank of America Lynch for the week ending April 23, several things stand out. The good news is that consumer spending appears to have bottomed and stabilized, albeit at a low level.

Overall card spending was down an average of 17% for the trailing seven days, a significant improvement from the prior week’s minus 28% and far better than second quarter GDP projections in the negative 30%-plus range. If one adjusts the data one day further back and removes April 19 for the Easter distortion, the trailing week averaged 18% lower spending. Not surprisingly, airline, lodging, entertainment and restaurant spend all continue to plunge, while e-commerce is experiencing breathtaking growth of 87% on average for the past week (a marked acceleration from 50% in the prior week). Grocery is accelerating to the upside after a few weeks of lull post-panic buying. Online electronics sales are booming as $150 billion in stimulus checks hit consumers’ bank accounts on April 15. The good news is that nearly every category has bottomed and is experiencing at least a slight recovery. Consumer spending will be important to watch to gauge when the economy and freight volumes will pick up. With many businesses shuttered and 22% unemployment, it is tough to envision more of the dramatic improvements that we have seen in the past two weeks in the overall rate of decline.

Transportation stock indices: Absolute levels positive for shippers, momentum positive for carriers

It was a good week for our transportation indexes. Three out of four were positive and truckload led the way on the upside at 4.9%. Parcels was the worst performer, down 1.6% for the week, while LTL was up 4.7% and logistics was up 0.7%.

Earnings season continued this week and there were several notable transportation companies to report.

For more information on the FreightWaves Freight Intel Group, please contact Kevin Hill at khill@freightwaves.com, Seth Holm at sholm@freightwaves.com or Andrew Cox at acox@freightwaves.com.