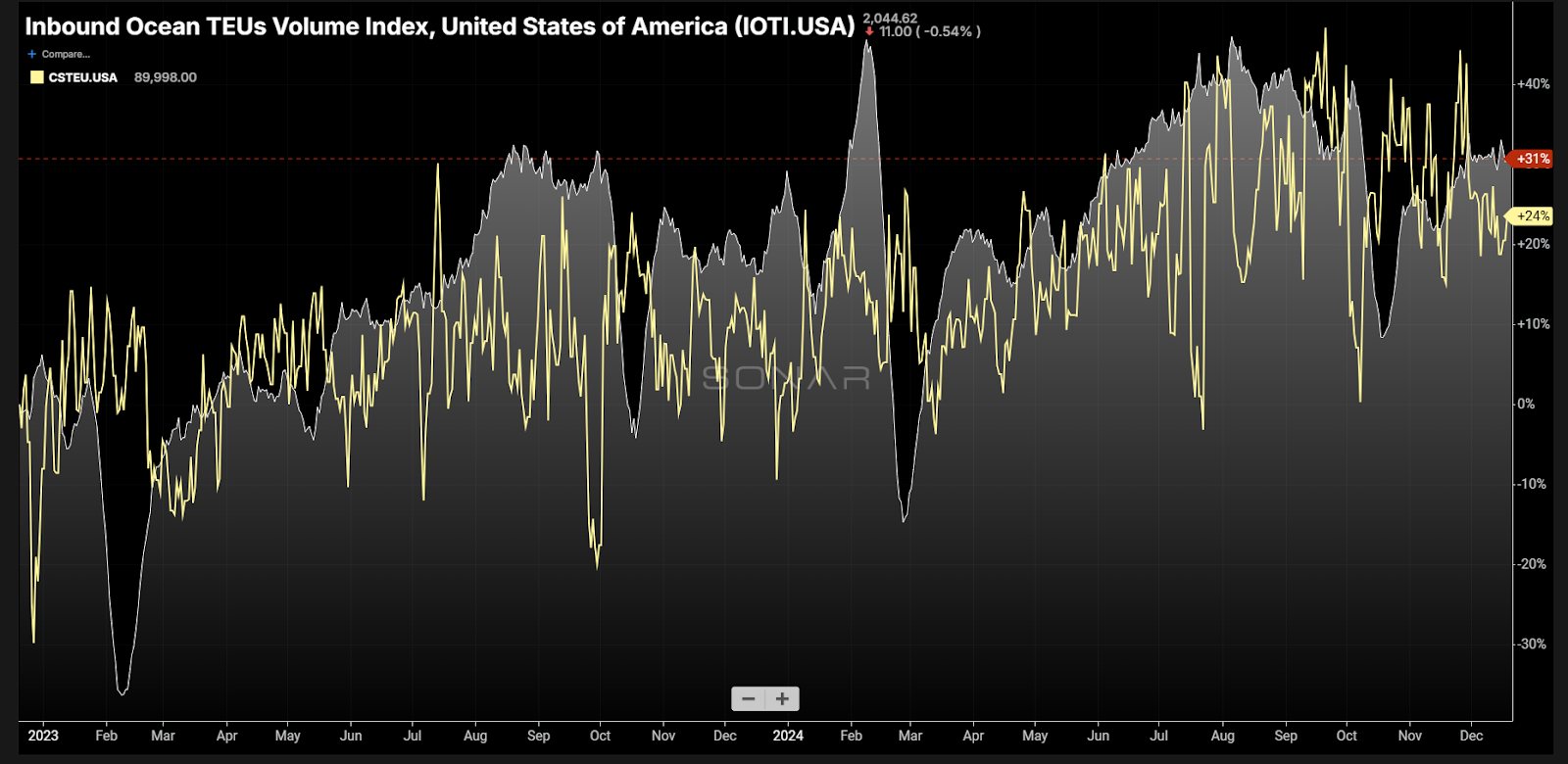

Chart of the Week: Inbound Ocean TEUs Index, Customs TEUs Index – USA SONAR: IOTI.USA, CSTEU.USA

U.S. container import demand is up more than 20% over where it was two years ago, according to U.S. customs and SONAR’s bookings data. While many expected steady increases in container volumes in 2023, the strong growth in 2024 was not on as many people’s bingo cards. What should we expect in 2025?

Import demand cratered in late 2022 thanks in large part to the inventory glut created by the just-in-case ordering strategy employed by many companies during the COVID supply chain crisis. With service and production being extremely unreliable, shippers had to increase their ordering lead times from weeks to months in advance of expected fulfillment.

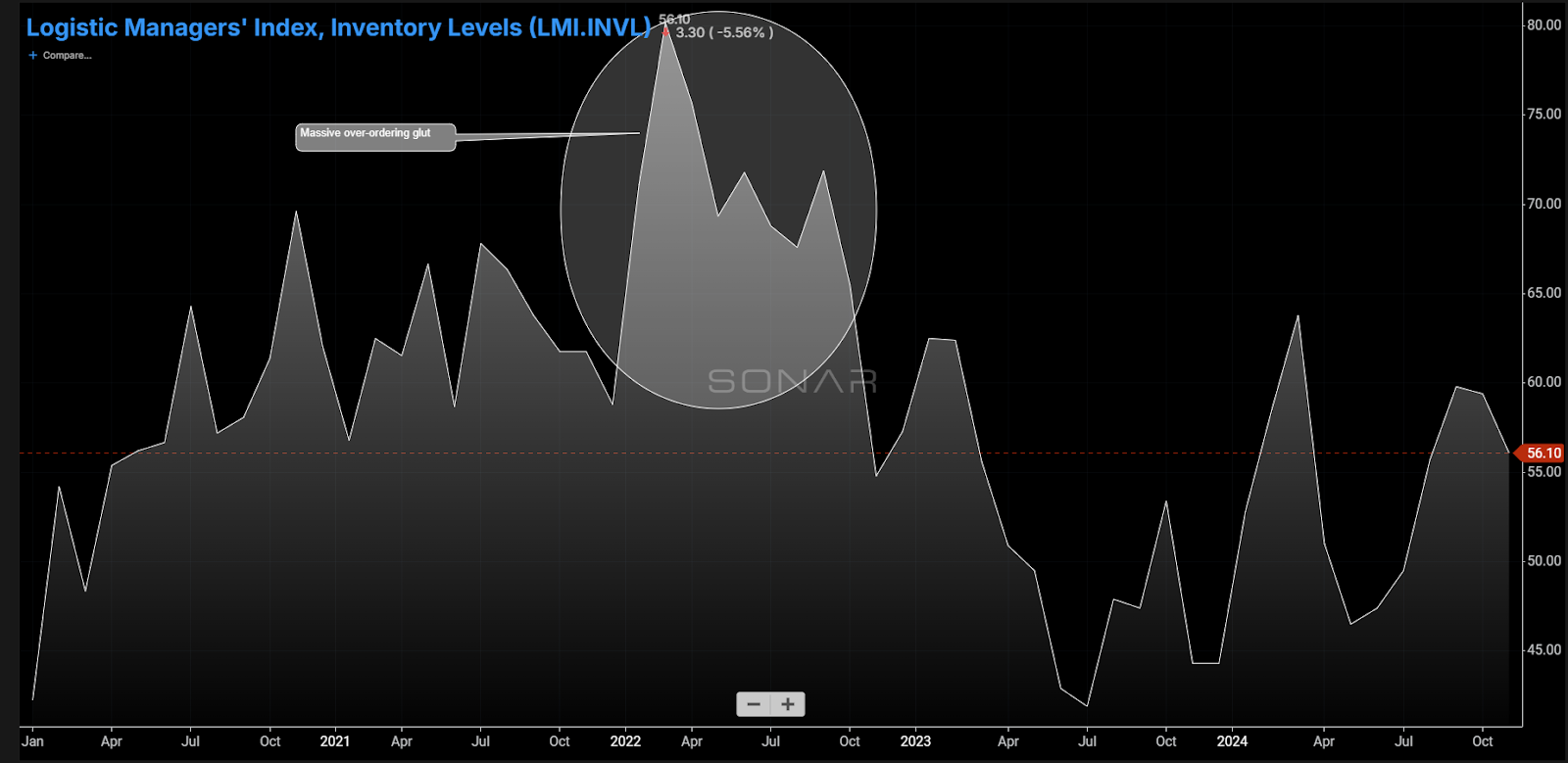

Once the stimulus checks and mass quarantining ended, consumers slowed their ordering just as supply chains were starting to catch up to the unanticipated waves of demand. The result was a massive buildup of goods in warehouses as companies were reportedly ordering about 45% more than they needed at the end of 2021, just to make sure they could meet demand.

The inventory level component of the Logistics Managers’ Index (LMI) reflects this inventory growth spike as values went from 58 (slight growth) in December 2021 to 80 (extreme growth) in February 2022.

Companies like Walmart and Target spent most of 2022 trying to right-size their inventories. By the end of 2022, most companies were reportedly much more streamlined and had nearly reverted entirely to more of a just-in-time inventory management strategy.

The Israel-Hamas War began in October 2023 and eventually led to the Houthi rebels attacking merchant vessels in the Red Sea just over a year ago. Many container lines decided to stop operating in the region, extending the length of their trips from Asia to Europe by over two weeks.

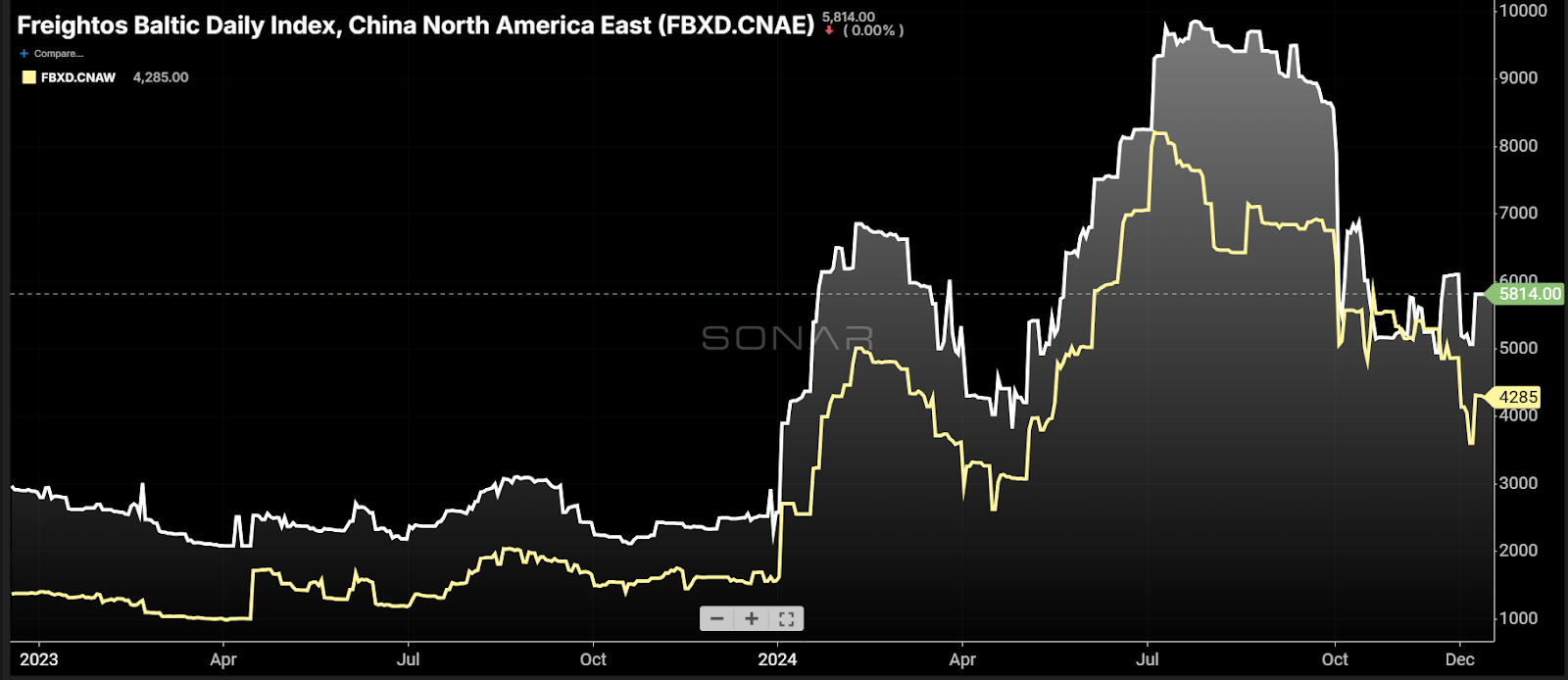

Container shipping rates appeared to react to the Red Sea conflict escalation in the beginning of 2024, according to Freightos’ Baltic Exchange Indices. Rates from China to both North American coasts nearly tripled in less than a month.

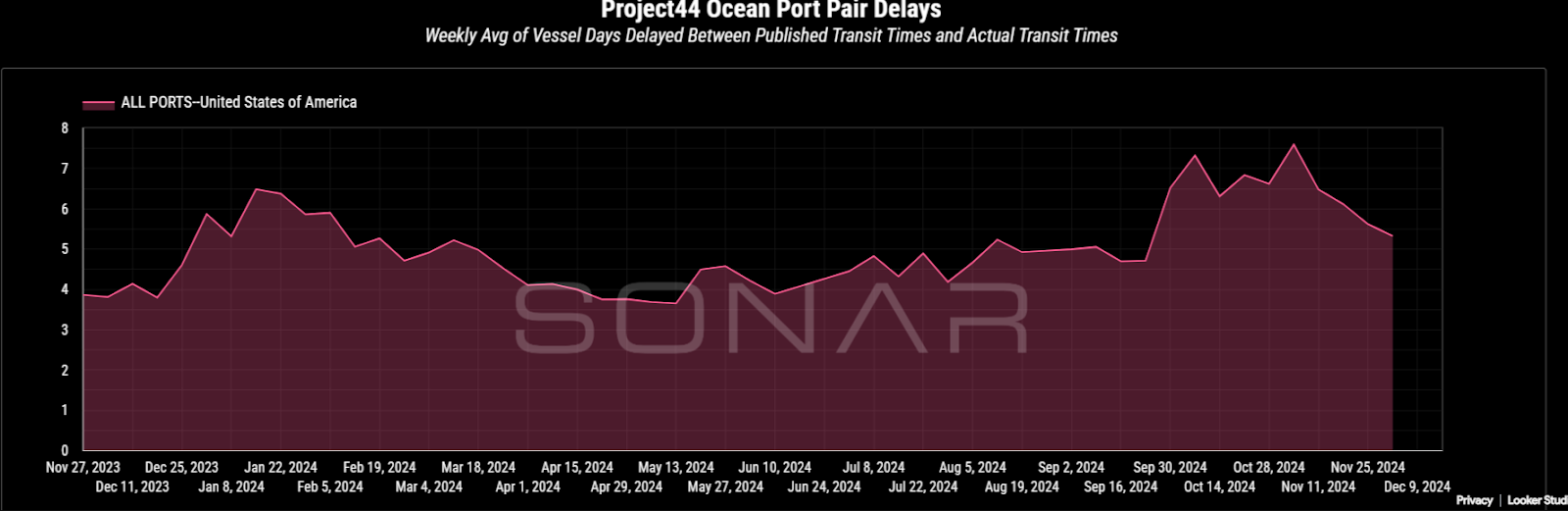

Service levels deteriorated as average transit times for shipments coming to the U.S. increased by more than two days, according to SONAR booking data. After a year of relative quietude, importers were once again hit with a bout of uncertainty.

Looking at project44’s Port Pair Delays in SONAR’s Container Atlas application, there was a noticeable spike in divergence from expected service times in January, which was to be expected. Another less foreseeable jump in delays occurred in October, just as the International Longshoremen’s Association strike began.

While most of the issues plaguing the maritime space were impactful to service, they did not necessarily increase demand in total. They led to the return of some small level of inventory pull-forward activity and pushed container flows back into the U.S. West Coast.

Looking back at the Freightos spot rates, you can see that spot rates from China to the North American east coast were actually lower than the much shorter west coast lanes in October for a brief time. This was due to shippers avoiding the strike.

The strike only exacerbated the longer-running coastal preference shift that had been occurring since late 2023 thanks to the Red Sea attacks and a drought affecting the Panama Canal.

What about demand?

Despite the fact that the Fed has been fighting off historic inflation with elevated interest rates, consumers have still been showing up in the U.S. This is not to say that all sectors have been feeling this evenly, but there has been growth in both maritime and surface transportation demand over the past two years.

Trucking demand has faltered somewhat at the end of this year as it has lost share to the railroads in the long-haul segments. Imports moving into the western ports have helped drive this.

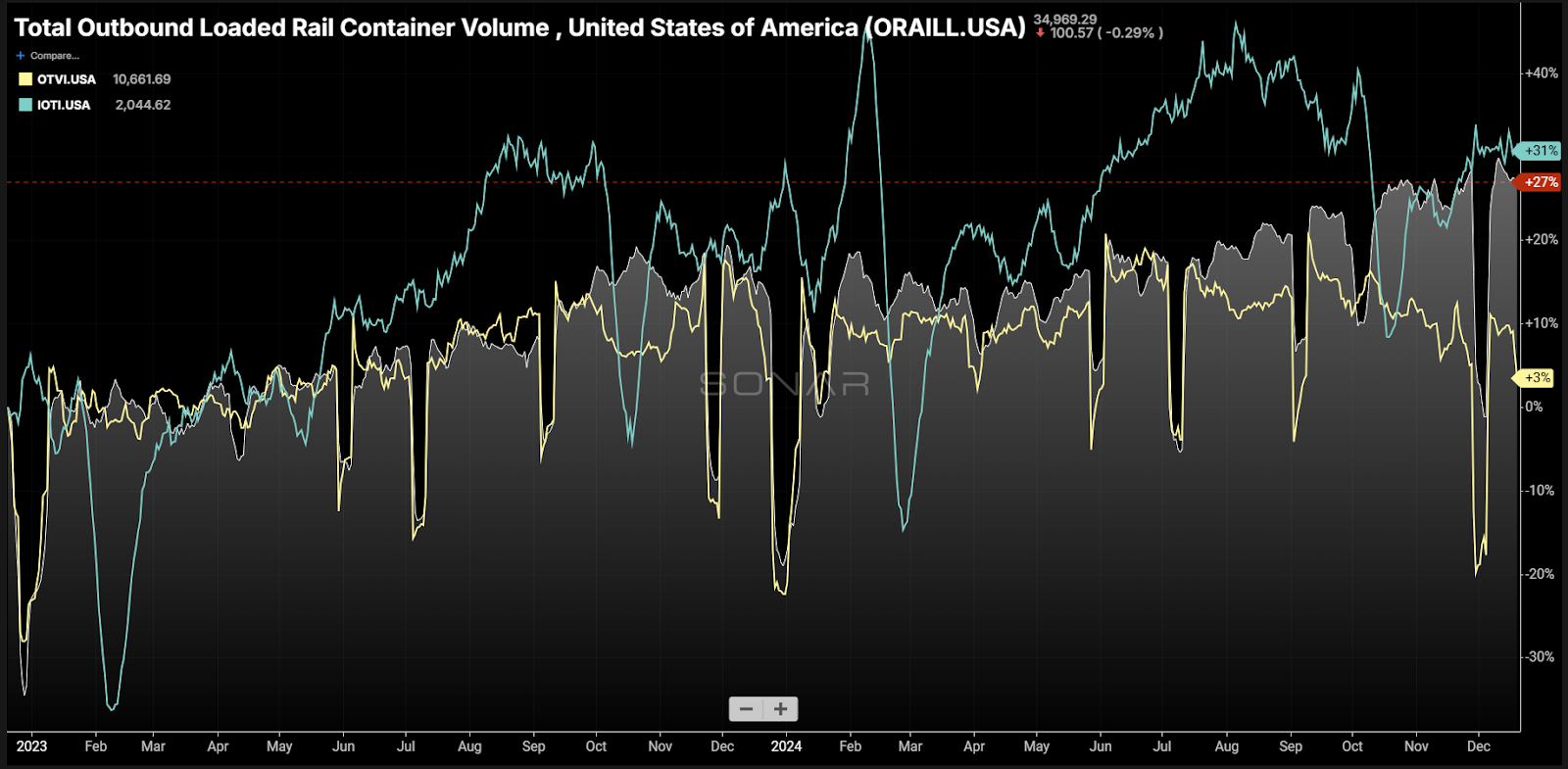

SONAR’s primary demand indicators representing trucking (OTVI), intermodal (ORAILL) and maritime (IOTI) are up versus where they were at the end of 2022.

Note that these indices primarily measure dry and containerized goods, not the bulk materials that characterize the raw material inputs for manufacturing. That sector remains in limbo.

So what’s next?

With inventory levels having been largely corrected, there is still looming uncertainty in the form of policy and tariffs. This will continue to keep shippers guessing on how strong demand will be in the coming year as well as where they will be able to source their goods.

How certain can we be about anything when the terrorist groups are now hosting security webinars?

In the short term, continued pull-forward activity should be anticipated, especially heading into the Lunar New Year period, when production in Asia stops. The Trump administration will be taking over at this point, and there are still clouds of uncertainty around what that means for consumers and businesses alike.

Uncertainty means slow growth is likely as a general trend until policy becomes clearer. The risk for sharp swings in either direction remains high. For many companies, it will be like driving in the fog. Vigilance and visibility will be crucial for avoiding running off the road and being able to hit the accelerator when the time is right.

About the Chart of the Week

The FreightWaves Chart of the Week is a chart selection from SONAR that provides an interesting data point to describe the state of the freight markets. A chart is chosen from thousands of potential charts on SONAR to help participants visualize the freight market in real time. Each week a Market Expert will post a chart, along with commentary, live on the front page. After that, the Chart of the Week will be archived on FreightWaves.com for future reference.

SONAR aggregates data from hundreds of sources, presenting the data in charts and maps and providing commentary on what freight market experts want to know about the industry in real time.

The FreightWaves data science and product teams are releasing new datasets each week and enhancing the client experience.

To request a SONAR demo, click here.