Following discouraging earnings reports from less-than-truckload peers, prompting a broad sell-off in the stocks, XPO solidly beat first-quarter expectations Friday and provided a favorable outlook moving forward.

First-quarter adjusted earnings per share of 81 cents came in 14 cents ahead of the consensus estimate and 25 cents higher year over year (y/y). The adjusted result excluded 25 cents per share of transaction and restructuring costs.

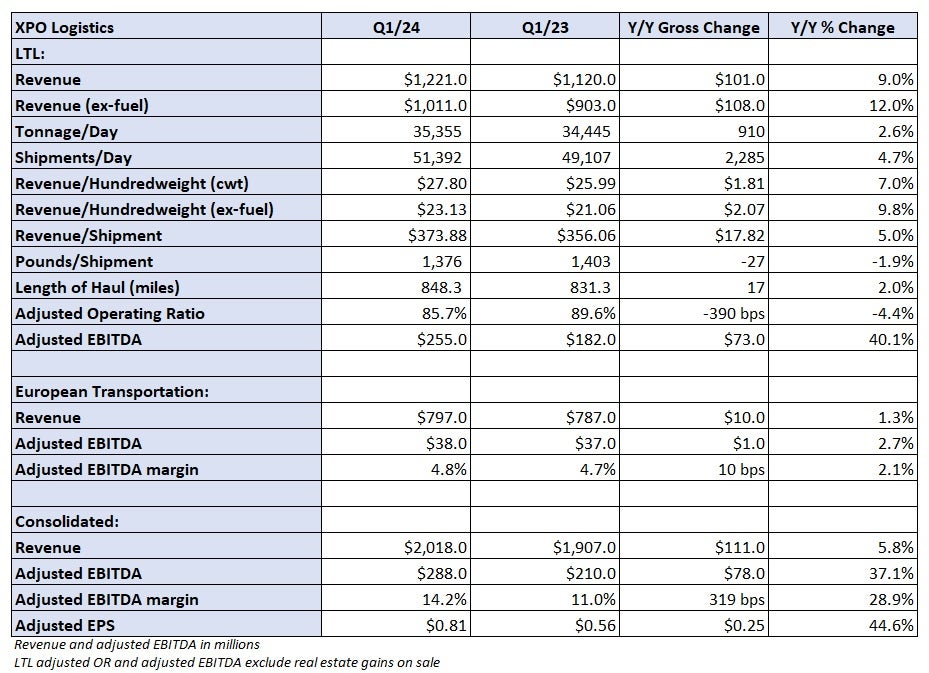

Revenue in XPO’s (NYSE: XPO) LTL segment increased 9% y/y to $1.22 billion as tonnage per day increased 3% and revenue per hundredweight, or yield, was up 7% (up 10% excluding fuel surcharges). A 5% increase in daily shipments partially offset by a 2% decline in weight per shipment produced the tonnage increase.

On a y/y comparison, tonnage fell 1.1% in January, but increased 3.5% in February and 5.9% in March. Tonnage was 3.1% higher in April as shipment growth of 4.8% was partially offset by a modest decline in weight per shipment. Tonnage improved slightly from March to April on a two-year stacked comparison after declining sequentially in February and March.

On a Friday call with analysts, management said the y/y tonnage and yield growth rates in the first quarter will likely be repeated in the second quarter.

Pricing increased an average of 8% y/y on contract renewals in the quarter, following increases of 9% in both the third and fourth quarters. The yield increases are tied to service improvements, an increase in premium business triggering accessorial charges, and shipment growth among its local accounts, which tend to have a better margin profile.

On its fourth-quarter call in February, XPO quantified the various initiatives as a midteen pricing opportunity.

Accessorial revenue increased by double digits in the first quarter, and shipments with local customers grew 10% as it has added more than 3,000 local accounts so far this year.

The bankruptcy of Yellow Corp. (OTC: YELLQ) also presented a pricing tailwind. XPO reprices roughly 25% of its total customer book every quarter, leaving one quarter left to be repriced following Yellow’s exit last summer. However, management said it expects to continue to capture high-single-digit increases on contract renewals for the rest of the year given its yield initiatives.

XPO has already opened six of the 28 terminals it acquired from Yellow, with six more coming on line in the second quarter. It will open an additional 12 by the end of the year, with the remainder opening in early 2025. The additions are expected to increase network door count by 10% to 15% (17,000 doors in operation at the end of 2023). The acquired terminals will be neutral to OR this year and accretive to earnings next year.

The LTL unit recorded an 85.7% adjusted operating ratio, which was 390 basis points better y/y and 80 bps better than in the fourth quarter, outperforming the normal sequential change rate by 120 bps.

Purchased transportation expense as a percentage of revenue was down 250 bps y/y as the company continues to reduce third-party linehaul miles. Outsourced linehaul miles stood at 18% in the quarter, which was 370 bps lower y/y. The goal is to reduce outside miles to a low-teen percentage by 2027.

The company is forecasting 200 to 250 bps of OR improvement sequentially in the second quarter, or a 400-bp y/y improvement. That implies a low- to mid-83% adjusted OR, which would come close to the outer band of its 2027 target.

Service enhancements are driving the carrier’s improved yield and cost profile. A record claims ratio of 0.3% in the quarter, an eighth consecutive quarter of improving on-time metrics and the rollout of freight airbags at service centers (in use at 75% of terminals currently) were some of the highlights.

Adjusted earnings before interest, taxes, depreciation and amortization in the unit was $255 million, a 40% y/y increase.

XPO’s European transportation segment saw revenue increase 1% y/y to $797 million. It recorded an adjusted EBITDA margin of 4.8%, which was 10 bps higher y/y.

Shares of XPO were up 6.1% at 11:25 a.m. EDT on Friday compared to the S&P 500, which was up 0.9%. Shares of LTL peers were up 1% to 2% after some sold off more than 20%, following Old Dominion’s (NASDAQ: ODFL) lackluster report last week.