[vimeo-autoplay video-id=”390618432″]

The reorganization of XPO Logistics announced in January guaranteed the status quo in one respect: The company wasn’t going to sell off its less-than-truckload (LTL) division.

The fourth-quarter earnings the company released late Monday suggested that is a solid strategy as XPO’s LTL division improved its financial performance for the quarter even as most operating results were weaker.

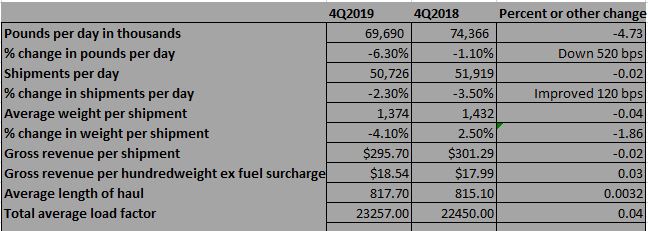

North American LTL saw its revenue for the quarter drop to $916 million from $940 million, a decline of 2.7%. But net revenue for North American LTL was up to $372 million from $362 million, an increase also of 2.7%. Net revenue percentage for the LTL division rose to 40.6% from 38.5%.

Most of the company’s operations turned in better financial results than the corresponding quarter of 2018. Net revenue percentage for the freight brokerage division posted a decline to 17.9% from 18.6%.But the Last Mile segment saw its net revenue percentage rise to 34% from 23.9%, and the Managed Transport segment rose to 27.2% from 21.7%.

LTL benefited from a decline in direct operating expenses, dropping to $138 million from $175 million, a decline of 21.1%.

The operating data on LTL was down, as expected. Pounds per day dropped 6.3%; shipments per day were down 2.3%; the average weight per shipment declined to 1,374 pounds from 1,432 pounds, a drop of 4%. Gross revenue per shipment declined to $29.70 from $301.29, but gross revenue per hundredweight rose to $21.52 from $21.03.

The end result was that the adjusted operating ratio for the LTL division was 82.3%, improving 500 basis points from the 87.3% posted for the fourth quarter of 2018.

CEO Brad Jacobs, in prepared remarks in the earnings release, said the LTL division benefited from “several new technologies” and that the adjusted OR of 82.3% was a fourth-quarter record.

XPO’s guidance for the coming year does not assume any particular divestitures, as the divisions to be spun off or sold have not been identified beyond the fact that the company will hold on to its LTL division. The guidance for 2020 came in near the consensus that Deutsche Bank analyst Amit Mehrotra had laid out earlier in the day in a note to investors. Adjusted EBITDA is expected to rise 7% to 10%, XPO said; the Deutsche Bank team said consensus expectations were 7%, which it viewed as “highly achievable, if not beatable.”

The company’s adjusted EBITDA for the fourth quarter of $432 million was in line with what Deutsche said was consensus.

The SeekingAlpha consensus was that the company would post revenue of $4.23 billion, but it fell short at $4.14 billion. But the consensus earnings per share was $1.01, and XPO posted adjusted EPS of $1.12 for the quarter.

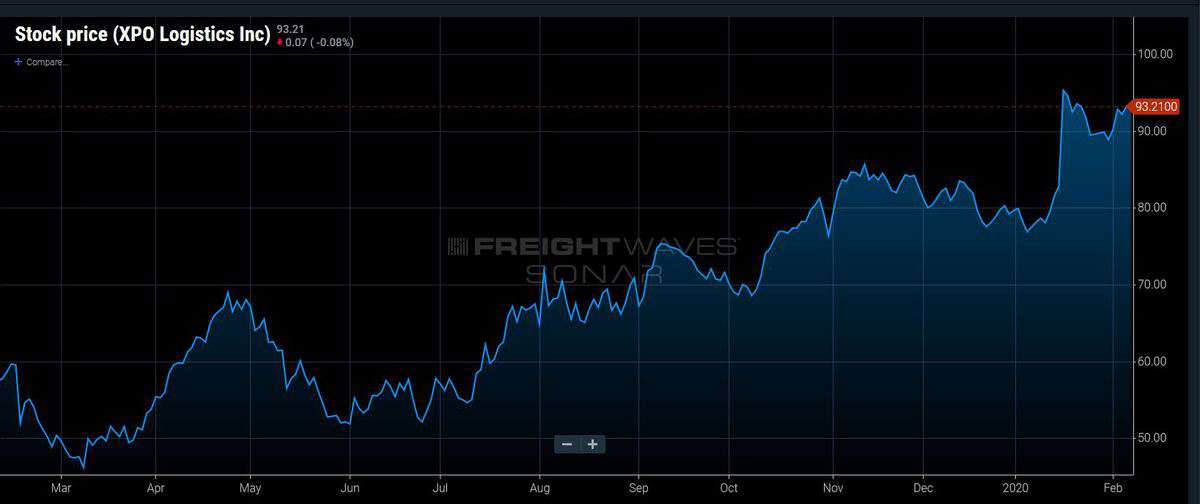

After the release of the earnings, investors clearly liked what they saw. At approximately 5:15 p.m. Eastern time, the stock was up $2.49 a share to $96.66, a gain of 2.64%. In the past 52 weeks, XPO has had a wild ride, swinging from a low of $45.73 per share to a high of $96.20, a price that was pierced in late-day trading Monday.

In post-release analysis, the Deutsche Bank team also was positive, calling it a “good” quarter and “much better than feared.” Specifically, Deutsche had earlier suggested that problems in XPO’s French operations might cause a miss on the consensus EBITDA projections.

“On our call-back with the company, CEO Jacobs noted that the sale/spin process is off to a ‘very, very good start’ and ‘going extremely well,’ but we don’t expect to get much beyond this on tomorrow’s earnings call … which is understandable,” Deutsche said in its report. The XPO conference call is Tuesday morning.