The Trump administration is considering levying tariffs on the remaining $300 billion of Chinese exports to the United States so far unaffected by duties. Freight Intel, FreightWaves’ proprietary research group, has just published a study warning that such a move would disrupt trade flows far beyond what has occurred so far.

Freight Intel Group research publications are live on the FreightWaves SONAR platform.

The first waves of China tariffs focused on industrial and agricultural goods, but the new tariffs would cover consumer products such as electronics, apparel and household goods. Costs related to those tariffs are more likely to be passed along to the American consumer.

Year-to-date, the United States has been importing between 20 and 40 percent lower volumes of the goods from China that have been tariffed. Over the last 12 to 18 months, importers have been shifting their supply chains and relocating sources for components and goods. Some production capacity has been near-shored to countries like Mexico, which narrowly avoided tariffs on its own exports earlier this month.

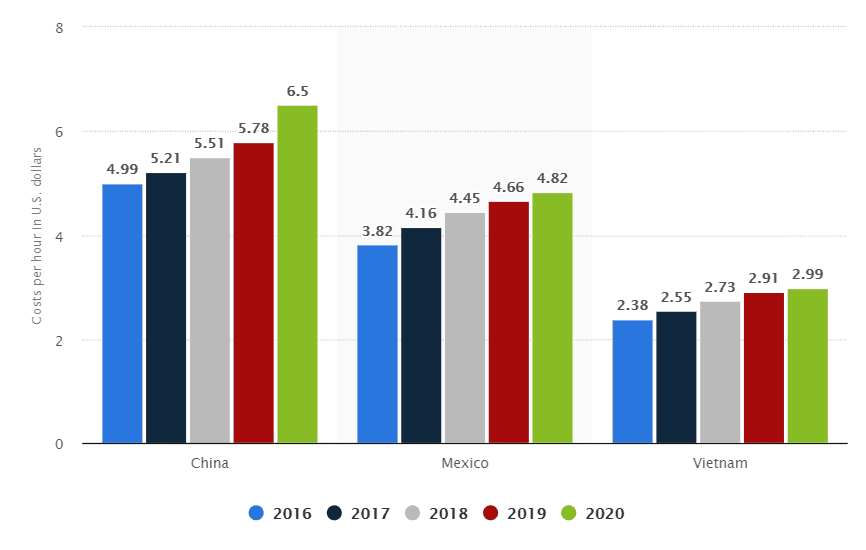

Other Asian countries like Vietnam and Bangladesh stand to gain from a breakdown in the U.S.- China trade relationship, but their economies and exports are tiny compared to China’s. For example, Vietnam’s GDP is smaller than Tennessee’s. Still, significant labor cost arbitrage opportunities exist in Mexico and Vietnam, compared to China. The chart below shows manufacturing labor costs for the three countries in U.S. dollars per hour:

“There’s nowhere to go. People say ‘Vietnam,’ people say ‘India,’ but keep in mind that India’s exports to the U.S. are about 10 percent of China’s and Vietnam’s went from 2 percent to 3 percent,” said Kevin Hill, who leads the Freight Intel group. “Everyone’s heading for the exit door in China at the same time and what they’re finding is that the facilities, the workforce, the infrastructure and the logistics do not exist to absorb that capacity. So you’re going to have greenfield projects that will take five to 10 years if you’re lucky, and you’re competing with everyone else, which will drive up prices.”

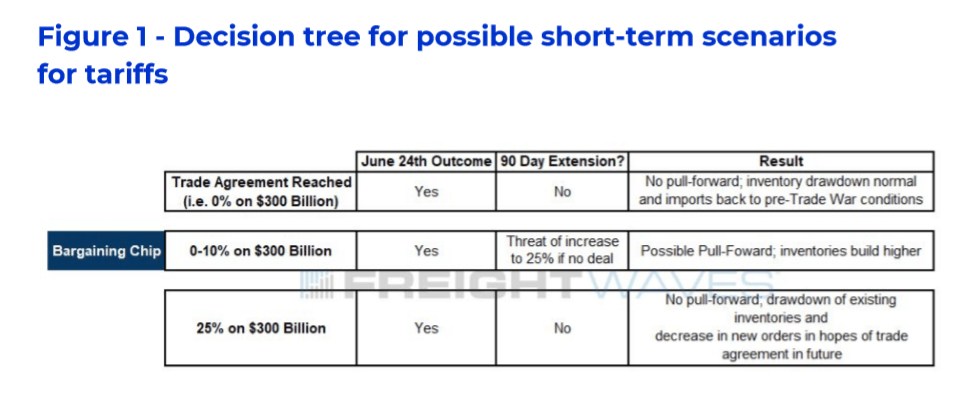

It is not known yet know whether new China tariffs will be implemented or not – a great deal depends on what takes place at the G-20 meeting in Osaka [Japan] next week – but there are a couple of ways they could be rolled out. When President Trump wanted to force Mexico to take action on border security, he threatened to levy 5 percent tariffs that would increase by 500 basis points every month until they reached 25 percent. This is a ‘bargaining chip’ strategy designed to avoid catastrophic disruption in the short-term but slowly ratchet up pressure on the target of the tariffs.

Of course, the possibility exists that President Trump could impose 25 percent tariffs on the $300 billion of Chinese goods all at once.

Freight Intel created the decision tree below to illustrate likely outcomes in the various scenarios:

One of the most acute risks for the U.S. transportation industry is the immediate 25 percent tariff scenario. Inventory-to-sales ratios are already elevated. The danger would be that in the event of a large tariff on consumer goods, importers would stop bringing new goods onshore and run down inventories, hoping for a resolution before replenishing their stocks.

“Trade demand will plunge as shippers either: 1) work through excess inventories; or 2) delay new orders until inventory levels hit rock-bottom in hopes that a trade agreement is reached,” the Freight Intel team wrote.

In the event of a 25 percent tariff, air cargo demand should remain normal until about 30 days before the deadline, when a significant ramp-up occurs. If ocean capacity on the Transpacific sells out, air cargo could tighten sooner.

Intermodal capacity is already very loose; the trains are hauling fewer carloads and are running at higher velocities. Importers pulling freight forward to avoid a 25 percent tariff will need that capacity to find affordable warehousing space in the interior of the country.

“Either scenario [gradually building tariffs or a sudden 25 percent tariff] creates considerable headwinds and is bearish for the freight markets as strategies for both involve delaying future orders for new product,” Freight Intel wrote. “Freight markets can adjust to these scenarios in the short-term, but if tariffs stay in place over the long-term, then difficult structural shifts in the freight markets will be in order.”

The FreightWaves Freight Intel Group is comprised of a number of FreightWaves’ Market Experts and research staff. The Group is producing white papers and research on topics of interest to those in the freight, transportation, logistics, and supply chain ecosystems. As topics dictate, they will be supplemented by academic and industry experts with specific knowledge and/or expertise.

SONAR subscribers have full access to the U.S. China Tariffs: Dancing on the Ledge report, as well as all other reports written by the FreightWaves Freight Intel Group. SONAR subscribers or others interested in FreightWaves’ research should contact Kevin Hill at khill@freightwaves.com.