A recent polling of business leaders regarding future plans for capital investment in their respective companies declined sequentially in the third quarter of 2019.

A total of 138 chief executive officers participated in the third-quarter 2019 survey, the basis for the Business Roundtable’s CEO Economic Outlook Index. The index measures forward-looking expectations for sales, hiring and capital investment.

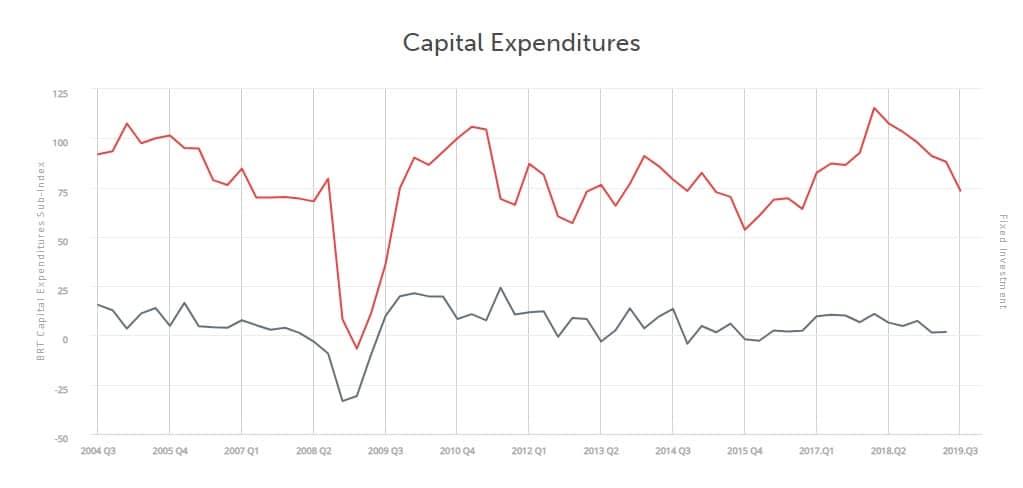

CEO expectations for capital investment declined 14.7 points to a 73.4 reading, down from the 88.1 reading in the second quarter and below the sub‑index’s historical average of 76.7.

The CEO Economic Outlook Index is a diffusion index, which subtracts the percentage of respondents reporting a decrease from those reporting an increase, ranging from -50 to 150. A reading of 50 or above signifies economic expansion while a sub-50 reading indicates economic contraction.

When business leaders were asked how they thought their company’s U.S. capital spending would change in the next six months, nearly two-thirds of respondents thought investment would remain level or move lower with 13% expecting an outright decline in capital spending. Only 53% of respondents expected level or declining investment during the second-quarter 2019 survey.

Capital expenditures (capex) by a company include investment in physical assets such as buildings, technology and equipment. Capital investments traditionally lead to future freight demand and have been a meaningful contributor to recent economic expansion in the U.S.

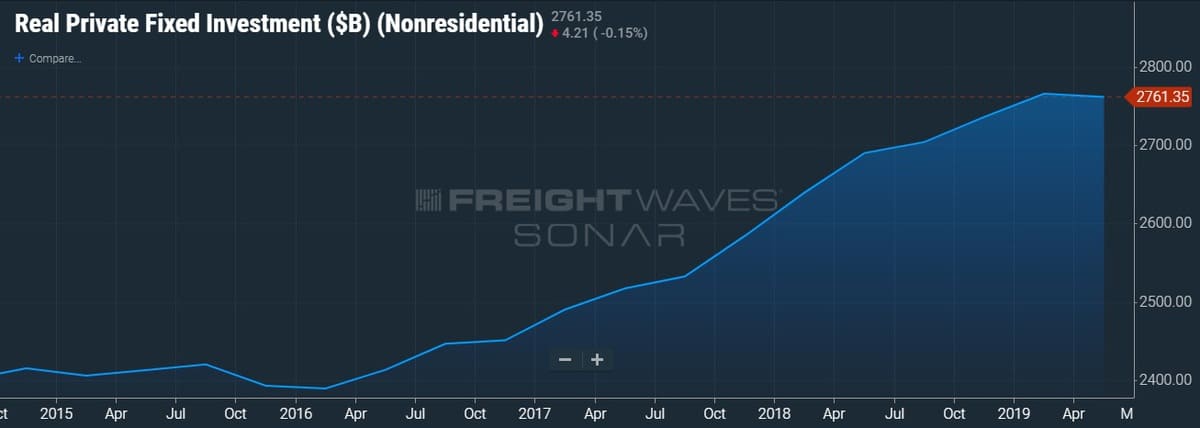

Real Private Fixed Investment (SONAR: RPFI.NRES) is the measure of growth in domestic investments reported quarterly. It captures additions and replacement to the stock of private fixed assets without deducing depreciation. It consists of nonresidential fixed investment and residential fixed investment measured in billions of dollars. The last reporting shows private fixed investment (nonresidential) declined for the first time since early 2016.

While the capex sub-index remains in expansion territory, sentiment is receding. Increased geopolitical uncertainty, namely U.S. trade policy centered on tariffs, and a slowing global economy were cited as reasons for the pullback.

“This quarter’s survey shows American businesses now have their foot poised above the brake, and they’re tapping the brake periodically. Uncertainty is preventing the full potential of the economy from being unleashed, limiting growth and investment here in the U.S. Opening markets and promoting rules-based trade remains vital to U.S. economic prosperity. Congress and the administration have the immediate opportunity to come together and provide stability and growth to our economy by enacting the U.S.-Mexico-Canada Agreement,” said Business Roundtable president and CEO Joshua Bolten.

Pressing further on the issue of trade policy, this quarter’s survey asked a special reflective question, asking CEOs “to look back at the last twelve months and report how U.S. trade policy and retaliation from foreign nations has affected their businesses.” The report stated that, “almost no CEOs reported a positive impact on their business.” One-quarter of all CEOs and 40% of manufacturing CEOs said that the trade environment has had “somewhat or very negative effect on capex.”

Further, more than half of the responses indicated that the impacts from the last 12 months’ trade policy had a “somewhat or very negative impact on sales” with one-third responding the same way with regards to the impacts on hiring.

The sub-index for sales expectations declined 13.5 points to 91.6, below the historical average of 112.9. Twenty percent of those queried on future sales expectations expect declines now versus only 9% last quarter. The hiring expectations sub-index moved modestly lower to 72.6, above its 58.5 historical average.

In sum, the CEO Economic Outlook Index declined 10.3 points sequentially to 79.2, in expansion territory albeit below the historical average of 82.7. This is the lowest level for the index since fourth quarter 2016.

Business Roundtable is an association of CEOs of America’s leading companies representing more than 15 million employees and more than $7 trillion in annual revenues. The Business Roundtable CEO Economic Outlook Index has been conducted quarterly since fourth quarter 2002.