The nation’s largest flatbed carrier, Daseke Inc. (NASDAQ: DSKE), expects “general industrial softness” and a “sustained weakness” in the oil and gas markets to continue through the first half of 2020. On the company’s earnings conference call, Daseke’s management team said that the market has been softer in the first quarter when compared to the fourth quarter of 2019.

When asked for specifics, management said that oil rig counts are “down hard,” but its wind-energy business has provided a substantial offset. Management said that the company’s exposure to the oil and gas markets was 13% during 2019.

When pressed on the impacts of the coronavirus, management said that the bulk of the company’s business is domestic, but that they have seen a drop in container volumes. Further, they said that one customer project that is tied to Chinese components has been delayed.

The Dallas area-based carrier reported an adjusted net loss of $0.12 per share for the fourth quarter of 2019, better than analysts’ forecasts for a $0.20 per share loss, but worse than management’s recently updated guidance.

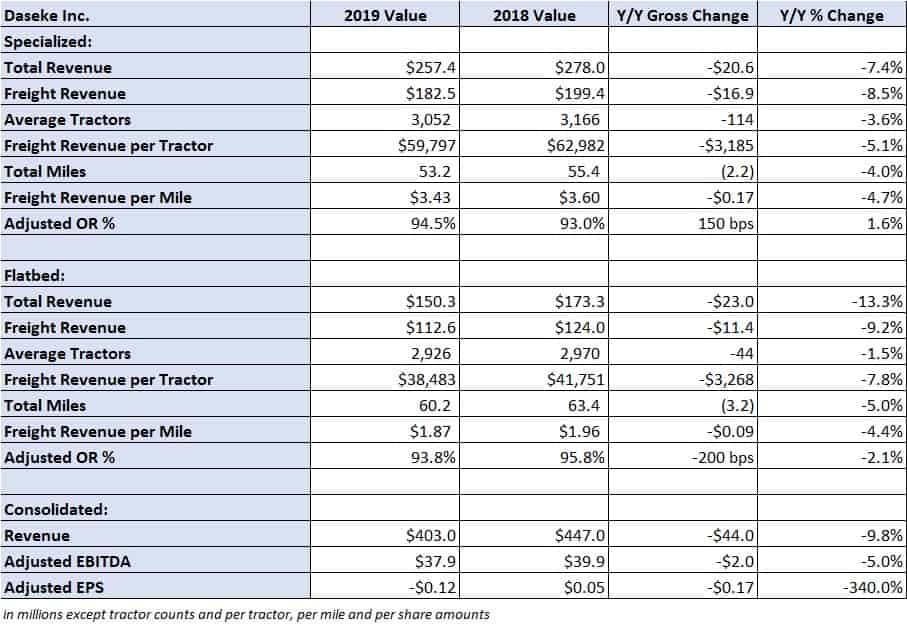

At the end of January, Daseke issued a press release increasing its financial expectations to the “high-end” of its prior guidance range for fourth-quarter and full-year 2019. The new expectation called for a fourth-quarter adjusted net loss of only $6 million to $2 million, or roughly $0.09 to $0.03 per share. While total fourth-quarter revenue of $403 million, down 10% year-over-year, was within management’s new guidance, the $7.8 million adjusted net loss was not.

Further, Daseke’s full-year 2019 adjusted net income of $2.1 million missed management’s updated full-year 2019 guidance of $3 million to $7 million.

“Adjusted” figures exclude items expected to be non-recurring, like transformation, restructuring and impairment charges. In 2019, Daseke recorded $312.8 million in impairment charges as valuations of prior acquisitions declined mostly due to the declines in used truck prices.

Next phase of restructuring

The carrier continues to restructure operations after a decade of acquisitions. Daseke remains on track with “Phase I” of its restructuring plan, which lowered the company’s tractor count, trailer count and non-driver headcount each by 8% and is expected to achieve an annual run rate of $30 million in incremental operating income by the end of first quarter 2020.

“2019 proved to be a year of significant transformation for Daseke, as we took aggressive action to streamline the business, reset our leadership team, and reposition the company to drive profitable growth in the future,” said Daseke CEO Chris Easter.

Easter was named Daseke’s permanent CEO last month after serving in the role on an interim basis for six months after the company’s founder and CEO Don Daseke stepped down.

Additionally, the company announced “Phase II” of the improvement plan. This phase is expected to deliver a run rate of an additional $15 million in operating income by the end of 2020. Like Phase I, this phase will integrate three more previously acquired operations, taking its total number of separately operated business units from 13 to 10. (Phase I provided a reduction in standalone carriers from 16 to 13.) Other “business improvement actions” are expected to be taken as well.

Easter continued, “In total, we expect that Phase I and II of our Operational Improvement Plan, which began in August 2019, will deliver $45 million in annual operating income improvements as we enter fiscal 2021, and will position the company for more profitable growth as the industrial market improves.”

Fourth-quarter results

Daseke reported revenue declines in both of its specialized and flatbed divisions due primarily to “lower freight rates and lower miles driven.”

The company’s specialized segment saw a 7% year-over-year decline in total revenue to $257 million due to “softer oil & gas related end markets.” The division’s average tractor count was 114 units lower and rate per mile declined 5% to $3.43 in the period.

The division reported a 94.5% operating ratio (OR), 150 basis points (bps) worse year-over-year. In addition to demand weakness, management noted strength in wind-energy markets and the sale of underutilized equipment as offsets to further margin degradation.

The flatbed division reported a 13% decline in total revenue at $150 million compared to the fourth quarter in 2018. The average tractor count declined by 44 units year-over-year with a 4% decline in rate per mile at $1.87. The division reported a 200-bp improvement in OR at 93.8% given improved brokerage margins, which were partially offset by “softness in manufacturing- and construction-related end markets.”

Daseke ended 2019 with net debt of $608.4 million, $48 million lower year-over-year. The company generated $130 million in free cash flow during the year, allowing it to pay down debt and fund its capital expenditures (capex). Daseke’s leverage ratio, net debt-to-adjusted earnings before interest, taxes, depreciation and amortization (EBITDA) excluding one-time items, was 3.18x at the end of the year. Management said that the leverage ratio may move higher in the first half of 2020 as 80% of its planned $75 to $80 million in capex will occur then.

Guidance

Daseke’s full-year 2020 guidance calls for revenue to be in the range of $1.61 to $1.69 billion and adjusted EBITDA of $170 to $180 million compared to $170.9 million in 2019. Management said that they expect volumes to be “relatively flat” year-over-year in 2020 with rate pressure in the first half, subsiding in the back half as flatbed truck capacity tightens.

Management highlighted $32 million in EBITDA headwinds stemming from pricing and volume declines given lower U.S. oil rig activity as well as higher insurance expenses. However, they expect these headwinds to be offset by $36 million in restructuring initiatives.

Management said that their guidance doesn’t include any potential impact from the coronavirus.

Shares of DSKE are 15% lower on the day.