Citing recent COVID-19-related disruption, J.B. Hunt Transport Services (NASDAQ: JBHT) said intermodal volumes could be down in the double-digit percentage range in the second quarter of 2020. The company noted “mid- to high-single-digit” volume declines so far in April and expects the trend to continue over the next couple of weeks.

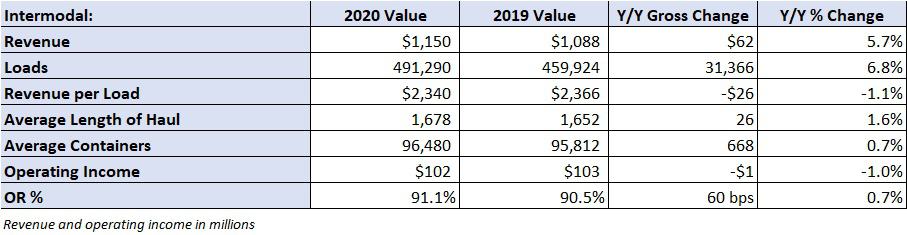

While intermodal rail traffic was roughly 9% lower year-over-year during the first quarter of 2020, J.B. Hunt reported a 7% volume increase, with transcontinental loads increasing 11%. Revenue per load was down 1%, up less than 1% excluding fuel. The division saw essentially flat operating income compared to the year-ago period even with headwinds from higher rail purchased transportation costs including the $8.2 million accrual related to the division of revenue with BNSF Railway, $4 million in one-time COVID-19 service bonus expenses, and higher equipment-repositioning costs.

Management called out imbalances in the network as inbound container freight from the West Coast ports is materially lagging backhaul movements. Additionally, competition from truck in the East remains a headwind to intermodal demand.

For first quarter 2020, J.B. Hunt reported earnings of 98 cents per share, 3 cents lower than the consensus estimate and 11 cents lower year-over-year. In addition to the accrual, the results included some nonrecurring expenses like $12.3 million in one-time bonus payments and $3.4 million of stock compensation for executive retirements.

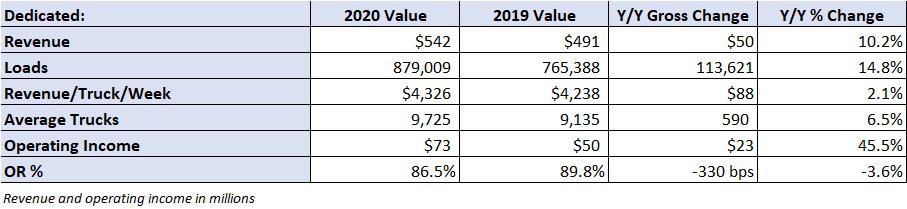

On the company’s conference call with analysts and investors, management said the dedicated division is holding up pretty well. They have moved approximately 1,000 trucks from dedicated accounts where demand has been negatively impacted by the pandemic to accounts that are in desperate need of capacity like grocers.

Dedicated was a key contributor again in the quarter. The division reported a 10% year-over-year increase in revenue with a 46% increase in operating income to $73 million. Management said that in addition to shifting equipment within dedicated accounts, the division flexed equipment to support its intermodal growth. The company netted 430 revenue-producing truck additions to the dedicated fleet in the quarter. Future dedicated fleet additions will be largely determined by the pandemic.

The company usually sees a consumer spending surge in the home improvement segment during the spring. Management said this hasn’t happened yet and that they expect second-quarter dedicated volumes to be flat with the first quarter, which implies a step lower on a year-over-year comparison. However, they expect dedicated margins to remain steady in the 11%-13% range. The dedicated margin was 13.5% in the first quarter, 330 basis points better year-over-year.

Still, the longer the lockdowns drag out, the greater the chance the company loses some seasonal business. Management said that the goal to add 800 to 1,000 trucks to the division in 2020 could be reduced by 20%.

Asked about contractual bid season and the pricing of new contracts, management said roughly one-third of contracts had repriced ahead of the lockdown and that those negotiations went largely as expected.

Negotiations have been a little choppier over the past couple of weeks, with some clients delaying new contracts over uncertainty and some pulling forward contract implementation as their capacity needs have spiked during the outbreak.

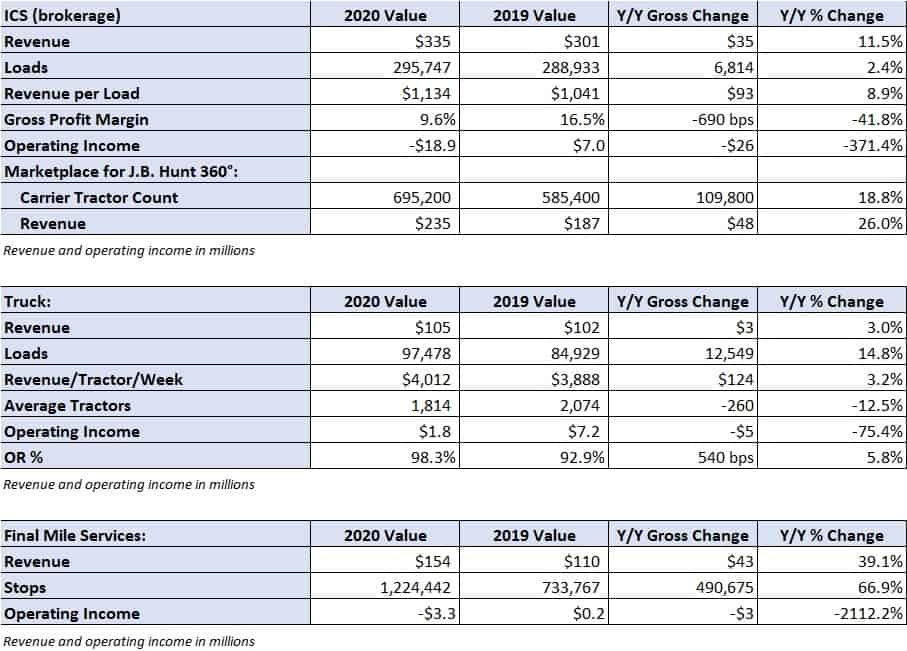

The company’s Dedicated Contract Services (DCS) segment was separated into two reportable segments — DCS and Final Mile Services (FMS). FMS is the nation’s largest final-mile asset-based network, generating $566.6 million in revenue during 2019. The division provides home delivery of big, bulky products with services ranging from drop-off to white-glove delivery.

In the first quarter, the division reported a 39% year-over-year increase in revenue to $154 million, largely due to recent acquisitions. J.B. Hunt acquired RDI Last Mile at the end of 2019, Cory 1st Choice Home Delivery for $100 million earlier the same year, and Special Logistics Dedicated in a $136 million deal in 2017.

Increased costs from investments in expanding the final-mile network as well as work stoppages at some of its customer sites due to the outbreak drove a $3.3 million loss in the period. Management noted that this division has been impacted the most by the lockdowns.

The final-mile division has exposure to the furniture, retail replenishment and appliance markets. Management noted that the furniture business has slowed significantly but that most of their exposure to that segment is asset-light through contracted drivers. The retail replenishment unit has 300 trucks that don’t run Class 8 tractors and can’t be rotated into service elsewhere. That is a fixed cost for the company as long as demand remains depressed. The company’s appliance delivery unit is a little more balanced, with an equal mix of contractors and company drivers.

Management said that there is a fair amount of seasonality in the final-mile division during the second and third quarters of each year. Without the typical seasonal bump, management expects losses in this division to accelerate in the second quarter.

Asked to compare this downturn to the financial crisis in 2008 and 2009, management sees J.B. Hunt as a different company. The company has gained significant scale in its dedicated offering, which provides stickier contractual volume commitments. Also, the company’s investment in Marketplace for J.B Hunt 360°, its digital freight market platform, has gained significant market acceptance and provided the company with improved data and insights to increase visibility into its operations.

During the quarter, Marketplace for J.B Hunt 360° transactions increased to $294 million, $95 million higher than the 2019 quarter, as brokered load volume was up 44% on the platform. There are now nearly 700,000 carrier tractors on the platform.

Second-quarter brokerage revenue increased 12% year-over-year, with volumes climbing 2% and revenue per load up 9%. However, the division reported an $18.9 million loss as gross profit margins were 690 basis points lower year-over-year at 9.6%.

Management noted tightening of supply in the truck markets as lockdown mandates became widespread and consumers loaded up on household necessities and groceries. Further, 74% of brokered loads came from contractual agreements, a 600-basis-point increase year-over-year. This presented a margin squeeze as truck capacity tightened and spot rates increased.

While management wasn’t ready to make a call on brokerage margins for the remainder of the year, they said gross margin compression should ease over the next couple of weeks. They have seen truck supply loosen since March and margins have already improved.

J.B. Hunt ended the quarter with its debt-to-earnings before interest, taxes, depreciation and amortization (EBITDA) ratio at 1x, well within covenant guidelines. Additionally, the company has $48 million in cash with no balance on its $750 million revolving credit facility that can be increased to $1 billion if needed.

The company lowered its capital expenditure (capex) budget by $100 million on each end of its new range of $575 to $600 million.