As part of FreightWaves overall coverage of freight markets, it publishes a summary of the changes in the economy over the past month, both in terms of the data releases and in developments in public policy. The Economic Roundup is designed to synthesize the events of the past month as they relate to freight markets, and provide a guide to trends to keep an eye on in the upcoming month. The Roundup is published on the first business day of each month with the next release scheduled for Friday, March 1st.

Overview:

It has been a challenging time to track the economy over the past month, as the government shutdown caused a disruption in data releases from both the Census Bureau and the Bureau of Economic Analysis. This includes several key indicators that speak to freight demand in the economy such as retail sales and international trade, and has clouded the picture of economic performance at the end of 2018.

Much of the data that has been available suggests that economy continues to slow from the rapid pace of growth seen during the middle of 2018. Consumer spending likely finished 2018 strong, but other areas of the economy have stumbled in recent months, including recent softening in investment demand, trade and housing.

GDP

After strong back-to-back quarters of growth in the second and third quarters of the year (4.2 percent and 3.4 percent, respectively), U.S. GDP likely slowed to a 2.6 percent pace of growth to round out 2018. Consumer spending appears to have held up nicely to round out the year, but contributions from other areas of the economy were likely significantly smaller.

The second and third quarters of growth were also subject to wild swings in some of the more volatile components of GDP. The third quarter saw a large gain in inventory building which was offset by a significant decline in net exports. This was likely driven by companies importing more than usual, and storing these products in inventory in an attempt to circumvent tariffs. Growth in the fourth quarter likely saw some additional inventory building and continued widening of the real trade deficit, but the size of the contribution to GDP growth should be smaller relative to the third quarter.

Trend to watch: The 2.6 percent growth rate expected in the fourth quarter is still considered above trend in the economy. First quarter 2019 GDP is likely going to be even slower, with a combination of falling equity values in December and reduced confidence taking some of the wind out of the sails of consumer spending and the government shutdown also subtracting from growth. GDP growth could very well fall below 2 percent to start off 2019.

Manufacturing and industrial production

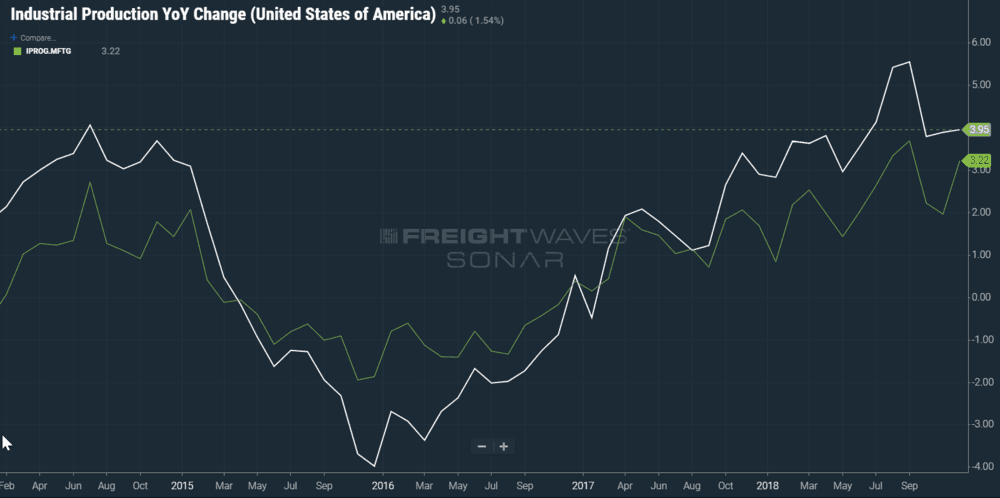

Industrial output continued to climb at a healthy pace in December, as total industrial production rose 0.3 percent from November’s levels. Year-over-year growth stayed strong at 4.0 percent to round out the year, as a jump in manufacturing production helped to offset declines in utilities output during the month.

Survey data from the manufacturing sector has been far less favorable, as both data from the Institute of Supply Management (ISM) and regional Federal Reserve manufacturing readings have slowed in recent months. Weakness in the new orders components of the ISM and regional Fed surveys have fallen sharply recently, which suggests that manufacturing industrial production numbers could weaken over the next couple of months, even if production in December performed well.

Trend to watch: The manufacturing sector will have to contend with an environment of weaker investment demand, a strong dollar and softening global growth. Production may be solid now, but look for it to begin to slip over the next few months.

Retail and inventories

It is tough to get a read on the outlook for the retail sector since the official release of December’s sales is still not available because of the government shutdown. December is the single busiest month for retail activity, and performance during the holiday season helps to shape the outlook for the sector. With that said, most of the fundamentals for consumer spending remain strong, including continued healthy job and wage growth. We expect that retail activity performed well to round out the year and should be solid through most of 2019.

On the inventory side, again there is a lack of official data, but trends before the government shutdown pointed to climbing inventory levels in the economy, as companies built up stores of imported goods anticipating a deterioration in trade relations with China. If growth elsewhere in the economy remains healthy, these inventories will begin to get drawn down in upcoming months.

Trend to watch: Consumer confidence has experienced a significant decline over the last few months, driven in large part by the stumbling December stock market and the government shutdown. Equities improved at the start of 2019, but it will be interesting to see whether retail takes a hit in January results.

Labor markets

Job growth continued to improve in December, rounding out the year with an impressive 312,000 jobs added. Unemployment remained below 4.0 percent, wage growth remained above 3.0 percent year-over-year, and the number of job openings continued to outpace the number of unemployed people in the economy. For the year, 2018 represented one of the strongest years of hiring in the post-recession era, which is doubly impressive considering how tight the labor market already was headed into the year.

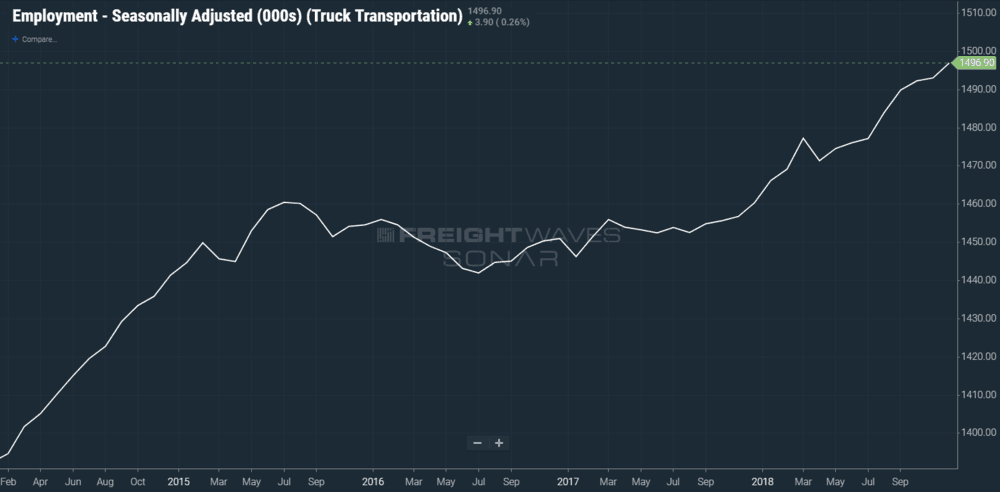

Trucking hires continued to make strides in December, adding another 2,900 workers to payrolls during the month. This marks the eighth consecutive increase in trucking jobs, pushing employment within the industry 2.2 percent higher than at this point last year. For the year, truck transportation added 36,000 additional employees to payrolls, which is the strongest year of hiring for the industry since 2014. Capacity appears to be expanding in the industry, which should ease some pressure on rates going forward.

Trend to watch: Employment numbers for January were released during the writing of this article, showing 304,000 jobs added in January, on the heels of a downward revision to 222,000 in December. Unemployment ticked up because of the government shutdown, but all appears to be healthy in the labor market at the start of the year.

Housing and construction

Like many other areas of the economy, much of the data surrounding housing and construction was delayed by the government shutdown. Housing starts, new home sales, building permits, and the value of construction put into place all were withheld in January, leaving many questions on the health of housing as we head into 2019.

The data that was available was not positive. Home buying sentiment has steadily declined in recent months as the number of existing home sales tumbled in December to a 4.99 million annualized pace. This is down 10.3 percent from a year earlier, as homebuyers continue to be plagued by rising mortgage rates and higher prices.

Trend to watch: The trend in housing likely won’t be clear even after data from December is finally released. There have been a number of weather-related fluctuations in the housing data in the third and fourth quarters, as hurricane season was quickly followed by the wildfires in California. The volatility connected to these events likely will not be fully worked through until the middle of the first quarter, leaving the underlying trend for now a bit uncertain.

International Trade

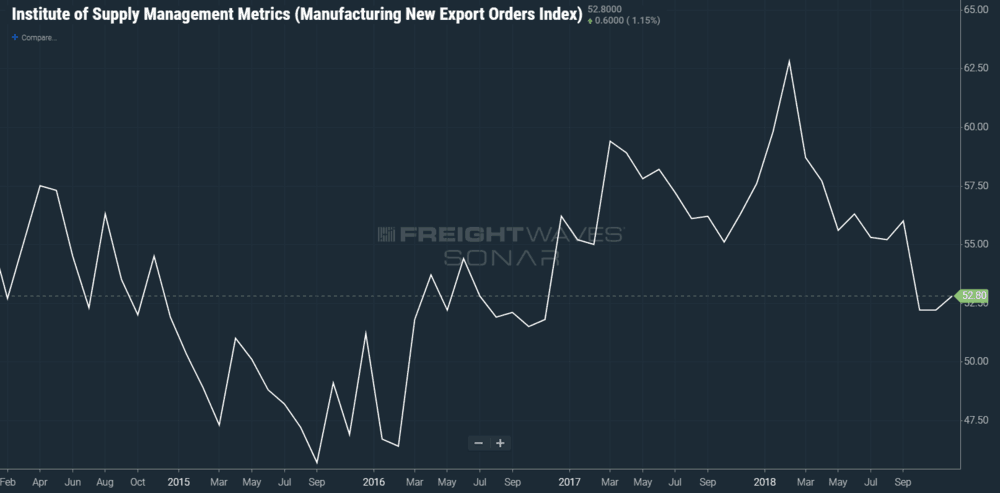

In the trade sector, official data is not available for end-of-2018 performance, but survey data suggests that export growth will be moderating in upcoming months. Data from the new export order component of the ISM index has slowed considerably over the last several months, signaling that demand from the rest of the world for U.S. manufactured goods is weakening. New orders typically lead actual shipments by one to two months, so growth should continue to cool from the generally impressive pace it enjoyed through most of 2018.

The export sector will likely be in a challenging environment throughout 2019, with the combination of a stronger U.S. dollar and slowing global growth hampering export demand. By contrast, imports may experience some early-2019 troubles, but should outperform the export sector because of the strength of the U.S. relative to the rest of the world.

Trend to watch: Because of all of the noise from the government shutdown, the tariff dispute with China took a bit of a backseat in the early part of the year. This situation is still very much unresolved, and the longer it drags on, the worse it is for trade performance this year.

Ibrahiim Bayaan is FreightWaves’ Chief Economist. He writes regularly on all aspects of the economy and provides context with original research and analytics on freight market trends. Never miss his commentary by subscribing.