Construction activity remained essentially flat for the second consecutive month, as the sector looks to gain some footing heading into the spring home buying season.

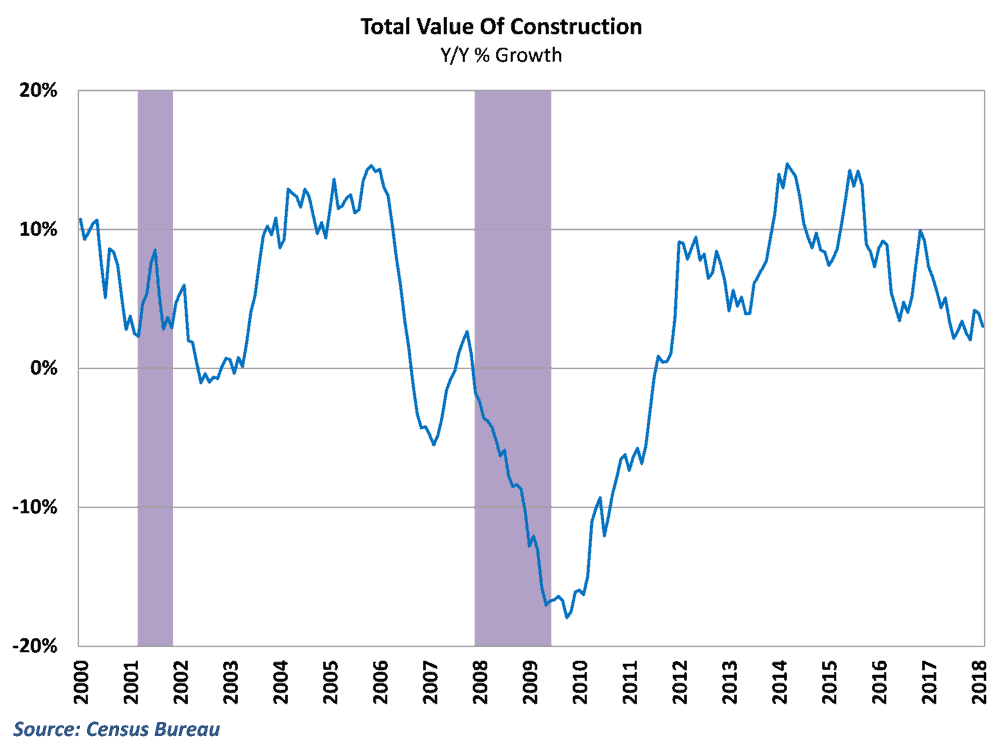

The Census Bureau reported yesterday that the total value of construction put into place in the economy rose by 0.1% in February to a seasonally adjusted annualized level of $1.27 trillion. This fell well short of consensus expectations of a 0.5% gain as year-over-year growth fell to 3.0%. (Story continued below)

Much of the disappointment in yesterday’s report stemmed from the public sector, as spending on infrastructure projects fell during the month. In the private sector, construction of both single and multi-family housing actually posted solid gains in February and remain on a general upward trend headed into the 2nd quarter. Construction on building improvements continued to struggle, however, declining for the second consecutive month.

Construction and freight markets

The amount of construction spending in the economy affects freight markets in a number of ways. Construction of new houses, office buildings, factories, and other commercial buildings typically involves the use of heavy machinery for grading the land before construction begins. Lumber and other building materials are then transported to the building site to begin construction. Both of these movements typically benefit flatbed carriers. Dry vans and LTL carriers typically benefit from the later stages of construction, as flooring material, appliances, and home or office furniture is transported to the building site.

Private residential construction activity is highly seasonal, with construction spending on new homes and improvements typically ramping up in February and March to have homes ready for show during peak buying season in the housing market during the spring and early summer months.

In addition, carriers benefit from the amount of spending on public infrastructure projects, particularly on highway and street expansions and improvements. Highway construction spending has generally declined over the past couple of years, with the trend continuing in February.

Behind the numbers

This was another disappointing report from construction after hopes were high following a strong end to 2017. The results are even worse than the headlines might suggest because the Census tracks the dollar value of construction put into place, not accounting for inflation. This makes it quite different than other metrics of construction activity such as home starts, and overstates the amount of actual activity taking place.

It’s worth noting, however, that part of the reason construction was doing so well in the 4th quarter was rebuilding efforts after hurricane season. As such, the weakness in recent readings is an indication that this boost may be fading. The spending declines on home improvement construction over the past couple of months would reinforce this notion, as much of the repair work on damaged structures gets captured in that category of spending. Construction on single family housing has been growing steadily for much of the past year, although again this is the nominal dollar value.

The declines on public infrastructure constructions spending are not new, but may be changing in the latter part of the year. President Trump began the administration’s push for infrastructure spending back in February, with plans for significant boosts in public and private construction of infrastructure projects. These plans face an uphill battle, but to the extent that some deal on infrastructure gets reached, there could be a significant uptick in public construction.

Ibrahiim Bayaan is FreightWaves’ Chief Economist. He writes regularly on all aspects of the economy and provides context with original research and analytics on freight market trends. Never miss his commentary by subscribing.