Strong numbers continue to roll in at LTL carrier Saia, which reported fourth-quarter 2021 results with a significant improvement in operating ratio from the corresponding quarter of 2020.

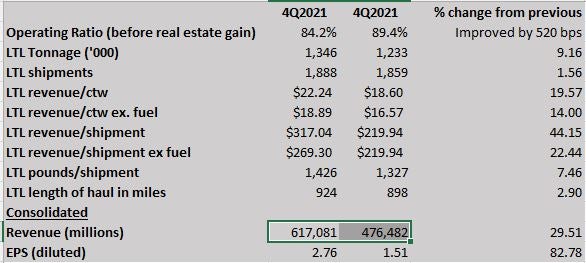

The company’s yield — revenue per hundredweight — was also up 14% from Q4 2020, rising excluding fuel to $18.89, up from $16.57 in the final quarter of the prior year.

Saia’s (NASDAQ: SAIA) OR for the fourth quarter was 84.2%, an improvement of 520 basis points from the 89.4% recorded in the final quarter of the prior year. However, the OR for Q4 did deteriorate slightly on a sequential basis, weakening 140 bps from the third quarter.

The bottom line beat consensus. According to Seeking Alpha, Saia’s GAAP-basis EPS of $2.76 per share was 16 cents better than consensus estimates. Quarterly revenue of just over $617 million was better than consensus by a little more than $17 million.

Saia’s stock is up 63.47% in the last 52 weeks, closing Tuesday at $299.72. But in premarket trading Wednesday after the earnings were released, it was up $40, or 13.35%, to $229.72. That would still be down considerably from the 52-week high of $365.50 established on Nov. 17.

Pricing power was evident in several statistics. For example, the $617 million in revenue was up 29.5% from the fourth quarter of 2020. But that came as total tonnage was up just 9.2%, pounds per shipment rose 7.5% and total shipments were up 1.6%.

“Our 2021 results reflect our ongoing efforts to profitably grow our business and expand our footprint to get closer to our customers,” CEO and President Fritz Holzgrefe said in a prepared statement. The difference in the revenue growth on the much smaller increase in shipments per workday, which were up just 3.3%, “is a reflection of this growing value proposition for our customers and their willingness to pay a fair price for great service.”

In a note to clients, the transportation team at Deutsche Bank led by Amit Mehrotra said the 84.2% OR was 100 bps better than expectations. The report also said the Saia results show that revenue growth at the company was about two-thirds driven by price, with the remainder by volume, which aligns with Holzgrefe’s comments.

A strong spread between revenue and cost per shipment, Deutsche wrote, suggests that pricing for both Saia and LTL in general “is not as cyclical as market participants fear, reflecting good service levels, which are most critical for LTL customers.”

Among other highlights in the earnings report:

— Saia’s cash holdings soared during the year. Cash and cash equivalents on the balance sheet were $25.3 million at the end of 2020. A year later, they were $106.5 million.

— Purchased transportation, which is normally a much smaller percentage of expenses for LTL carriers, rose significantly over the year. For the fourth quarter of 2021, expenditures of just over $70 million were 56% more than the fourth quarter of 2020. For the full year, that expense line rose 76%.

— Salaries, wages and employee benefits rose to $273.4 million from $248.2 million in the fourth quarter of 2020, an increase of 10.1%.

— Net income of $73.76 million translated into earnings per share of $2.76 on a diluted basis. That is up from $1.51 the prior year. For all of 2021, EPS of $9.48 was up 82%.

The FREIGHTWAVES TOP 500 For-Hire Carriers list includes Saia Inc. (No. 16).

More articles by John Kingston

Solid earnings send already hot Saia stock even higher

Sais’s execs not concerned about purchased transportation spend increase

Drivers well WorkHound onboarding process goes a long way in retention