Sick of earnings season yet? It’s this time of the quarter when I miss my old position as a sell-side stock analyst the least. For those looking to get caught up on earnings, there is plenty of coverage on FreightWaves. For freight carriers, the themes so far have been loosening market conditions and the lack of a fall peak season this year. Meanwhile, for CPG companies, recent themes include rising demand elasticities, moderating price increases, pressure from private label brands, continuing supply chain challenges and ongoing labor constraints.

For those sick of earnings, here is something different — five SONAR charts that stand out to me.

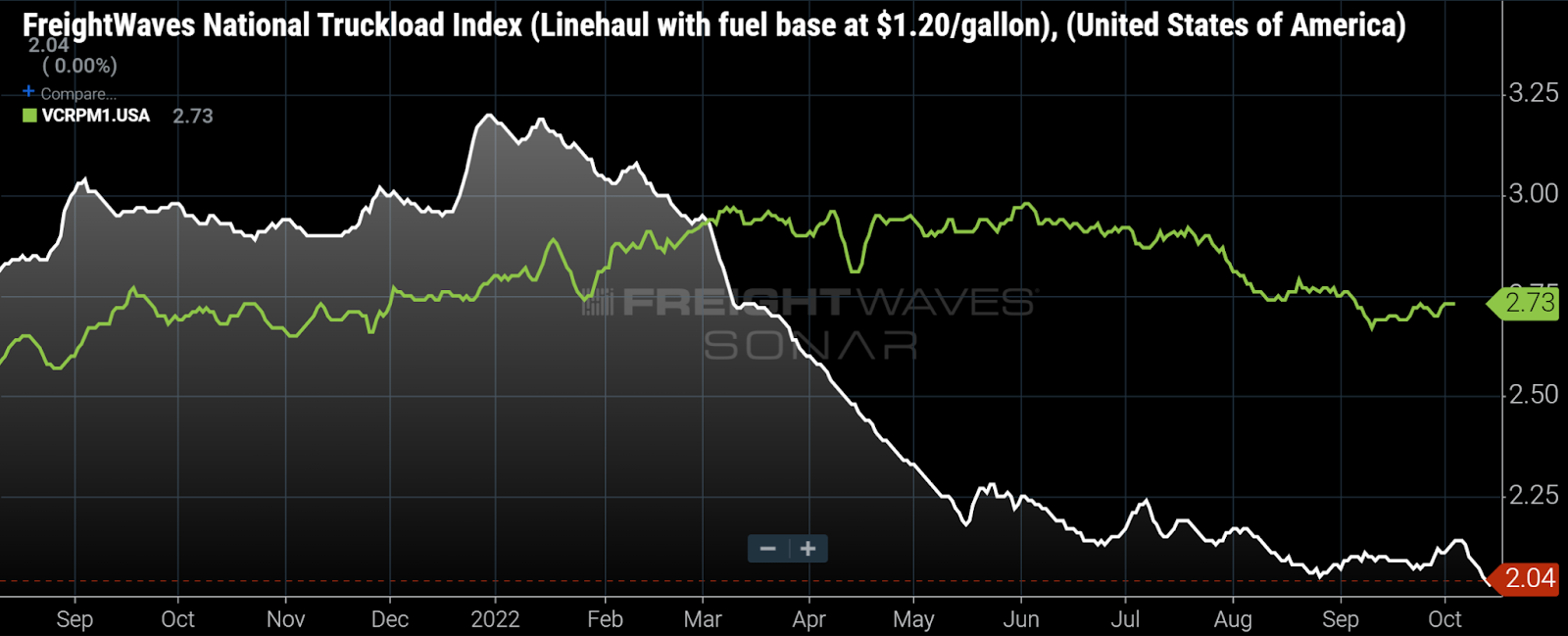

The spread between contract and spot freight rates remains high

The chart below shows how dry van spot rates (white line — adjusted to remove fuel surcharges) have fallen earlier and steeper than dry van contract freight rates (green line). Contract rates have started to moderate also, but the spread remains unsustainably high. Spot rates have been fairly stable the past two months and may be close to a floor, but contract rates have further to fall, suggesting that CPG companies and other shippers should be aggressive in upcoming rounds of negotiations.

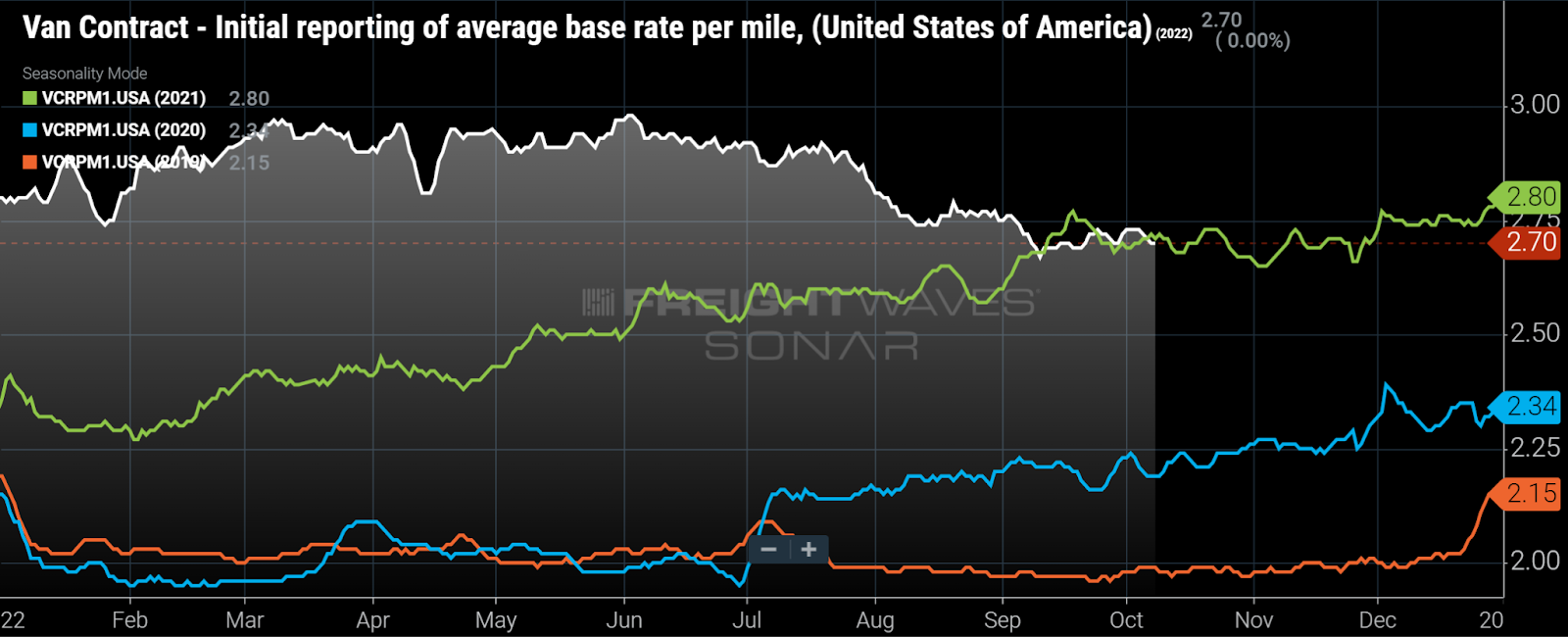

Dry van contract rates are lapping last year’s peak

Like most modes, dry van contract rates rose sharply two years in a row — from 2020 to 2021 and again from 2021 to 2022. Even with loosening freight markets, CPGs have highlighted freight rates as being a drag on profitability, reflecting elevated contract rates. Charts like the one below, which shows average dry van contract rates excluding fuel surcharges, shows how that may soon change as contract rates are no longer higher year-over-year and negotiating leverage shifts back into shippers’ favor.

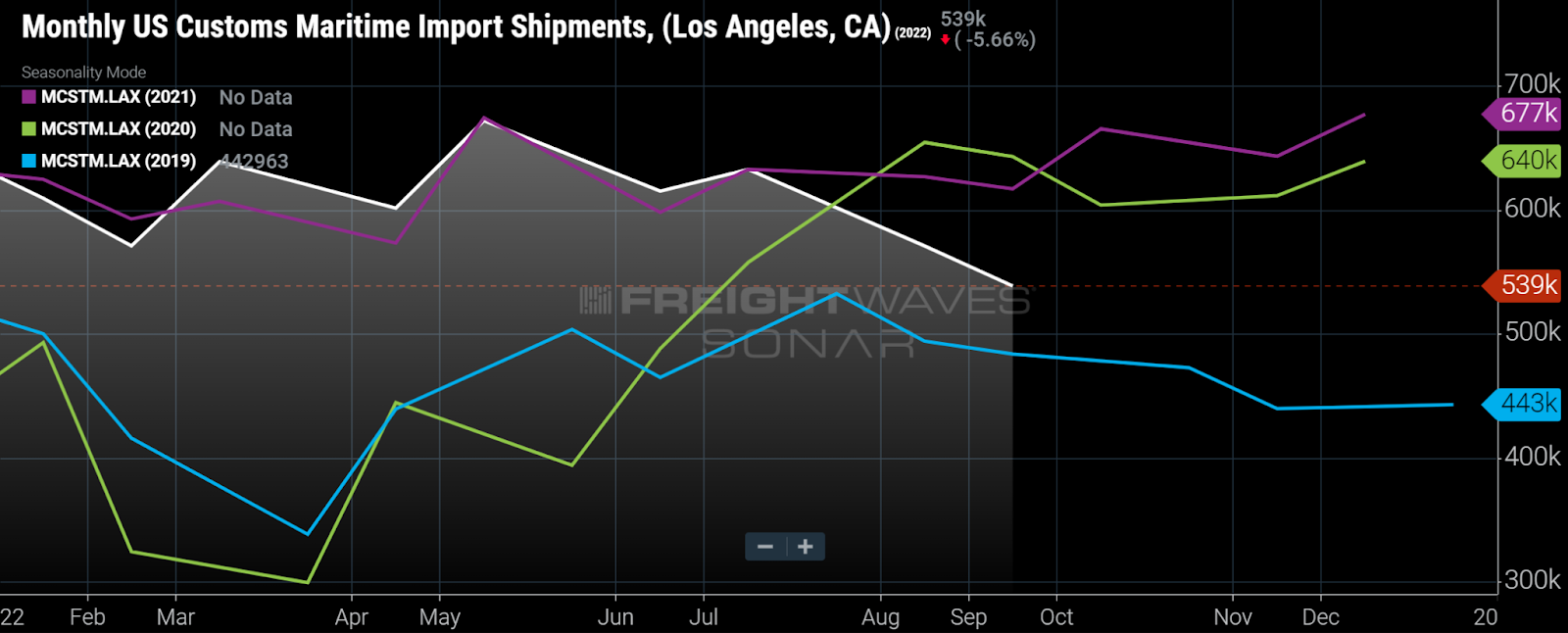

West coast imports have finally cracked

After being elevated since mid-2020, twenty-foot equivalent container imports to the Ports of LA and Long Beach plummeted in September, down 21.5% y/y and 7.4% y/y, respectively. For the Port of LA specifically, it was the lowest level for a September (typically, a strong month seasonally) since 2009. That data is relevant even for CPG companies that do not import products or ingredients because it directly translates to looser capacity for domestic surface transportation modes.

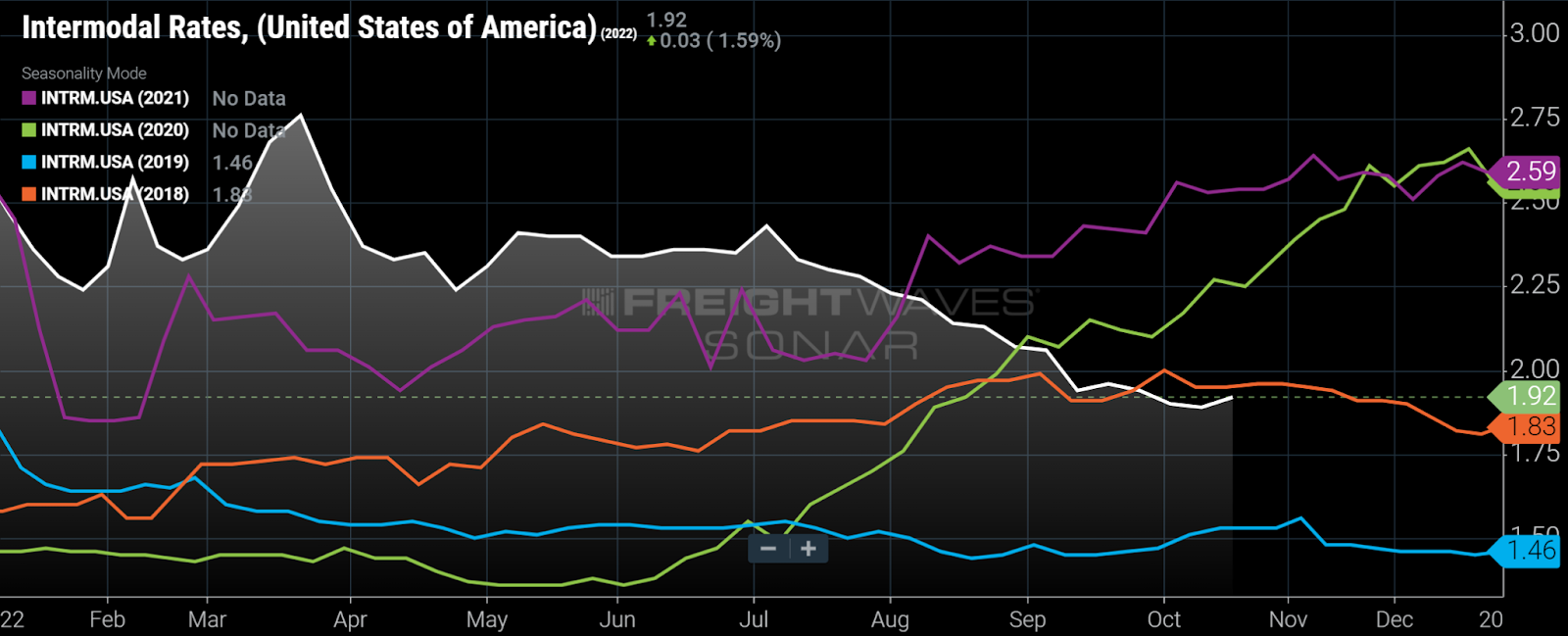

Carriers are not expecting a domestic intermodal peak season

I was not expecting one, but the comment from J.B. Hunt’s management team served as confirmation. In addition to the decline in imports, the lack of a seasonal rise in the chart below, which shows average door-to-door spot rates to move 53’ containers, also suggests that domestic intermodal volume this fall will be muted. When the Class I railroads are expecting tight intermodal capacity, as they were the past two third and fourth quarters, they take spot rates higher in an effort to protect capacity for contracted shippers. That didn’t happen this year.

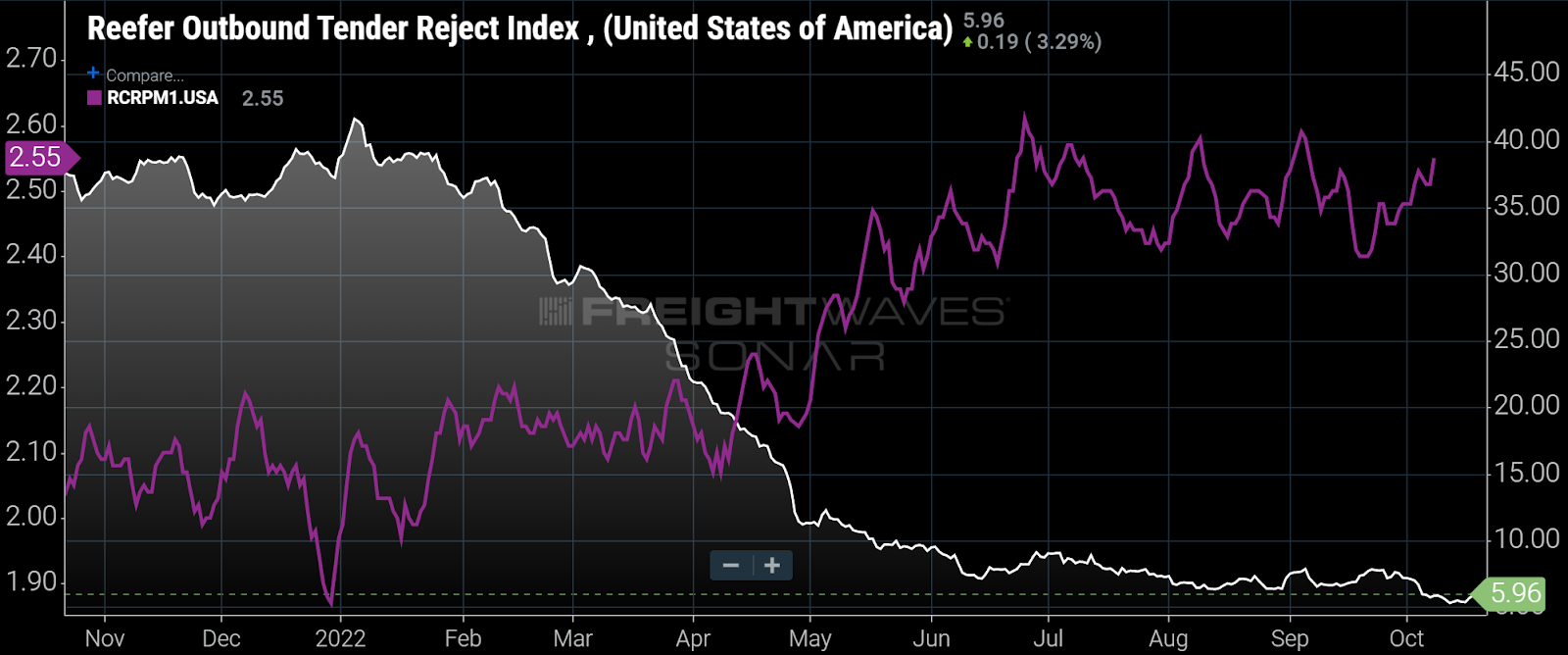

The reefer tender rejection rate is only 6%

While you could say “what a difference a year makes” right now for all freight segments, it’s perhaps nowhere more on-point than in the reefer segment. One year ago, average reefer contract rates, excluding fuel surcharges, were $2.05-$2.15 and carriers were rejecting 35%-40% of tenders because there were plenty of higher-rated loads on the spot market. That’s no longer the case and the current reefer contract rates of ~$2.55 (excluding fuel surcharges) are generally high enough to be market-clearing and, as a result, reefer carriers are only rejecting 6% of load requests.

Around the web:

Will the proposed Kroger-Albertsons merger put the squeeze on independent grocers?

Reports: Instacart is shelving its 2022 IPO plans

Flexport juices trade finance program with $200M credit line from KKR

Last mile isn’t enough anymore — it’s time to look at the last 100 feet

To subscribe to The Stockout, FreightWaves’ CPG supply chain newsletter, click here.

For more information on SONAR or to request a demo, click here.