Although the financial performance at RXO improved from the third to the fourth quarter of 2023, the year-to-year comparisons showed a stark downturn, which led analyst Brandon Oglenski from Barclays to ask a question on the 3PL’s earnings call with analysts.

RXO (NYSE: RXO) management on the call was mostly upbeat. CEO Drew Wilkerson kicked off the hourlong chat by saying, “Our model delivered outperformance for 2023.”

But Oglenski, according to a transcript of the call, was focused more on the quarter-by-quarter numbers that steadily declined at RXO for the first three quarters of 2023 before a small upturn in the fourth.

“I hope this doesn’t come off the wrong way,” Oglenski said, before noting that brokerage profitability has been stagnant. “I think we’re back to maybe the lowest approach even [than] where we were in early 2020. So help put in context that comment about growing profitable loads relative to consolidated results.”

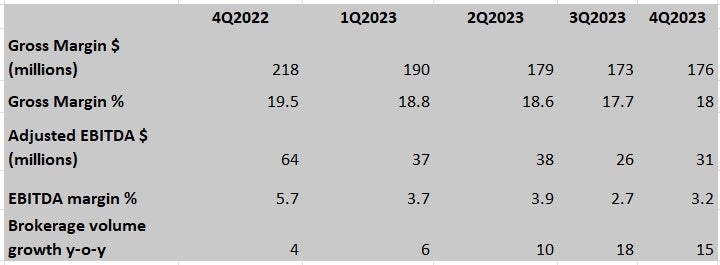

The actual numbers are that gross margin at RXO was $218 million in the fourth quarter of 2022 and declined the next three quarters to reach $173 million in the third quarter. It improved to $176 million in the fourth quarter. The fourth quarter of 2022 was the first full quarter the company reported after being spun off from XPO (NYSE: XPO).

Gross margin percentage of 19.9% in the fourth quarter of 2022 also declined the next three quarters, down to 17.7% in the third quarter, before rising to 18% in the final quarter of 2023.

Wilkerson’s response was essentially that the market was tough but that RXO was doing better than its peers. “We’re putting up best-in-class volume growth, and we’re doing that with best-in-class margins,” he said. “Now in the bottom part of the cycle, you do feel pressure on your gross profit per load.”

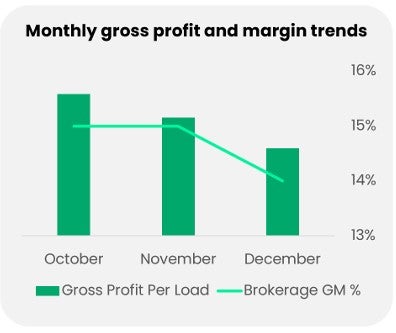

RXO does not disclose precise gross profit per load data. However, a graphic in presentation slides released with the earnings shows a slide throughout the fourth quarter, from between 15% and 16% in October to between 14% and 15% in December.

Wilkerson described that metric as “one of the biggest levers that we watch for where we’re going long term. … We’re confident that we’re making the right investments that allow us to operate at the best gross margin percentage with strong volume growth,” he added.

In his comments to kick off the call, Wilkerson touted several positive numbers beyond those in the accompanying table. Brokerage productivity, which RXO measures as loads per head per day, was up more than 15%. In the 15% growth in brokerage volume, truckload was up just 11% but LTL rose by 45%. “We again broke records in our brokerage business this quarter,” Wilkerson said, citing quarterly loads per day and total volume hitting new high-water marks.

Full truckload business was 84% of all volume, Wilkerson said.

RXO’s brokerage contract volume was up 23% year over year in the fourth quarter. The company cited “a strong brokerage sales pipeline, which has increased in size by 24% since the fourth quarter of 2022.” The prepared statement released in conjunction with the earnings said RXO expects brokerage volumes “to continue to grow on a year-over-year basis in the first quarter of 2024.”

Jared Weisfeld, RXO’s chief strategy officer, said the company’s “late-stage pipeline” of new business is up 24% year over year and 90% on a two-year comparison.

Investors were negative on the RXO earnings. At approximately 3:30 p.m., RXO stock was down 8.27% to $20.62. Its low for the day was $19.50.

RXO’s stock price had been riding relatively high recently. In the past three months, including Thursday’s performance, it had risen 18.4%. But its 52-week high wasn’t all that long ago: $24.33 on Dec. 27.

Earnings calls with analysts that take place in the second month of the ongoing quarter have the advantage of having a full month on the books to assess current market conditions, and several analysts asked how things were going for RXO in the first quarter. The answer generally was, not great but not that much worse.

Weisfeld said weather had an “acute impact” on performance in January. Some areas were “severely impacted” by weather, with the impact in weather-affected areas two or three times what it was in other parts of the country.

But he added that the bottom appears to have been reached. “We have seen some relief in the last week or so in terms of gross profit per load.”

In separate comments on the January market, Wilkerson said the first two weeks of January traditionally produce downward pressure on gross profit per load and percentage. “We saw that, but it actually was worse than what we anticipated,” Wilkerson said. He cited the Midwest and Southeast as areas particularly hit.

Wilkerson described conditions RXO faced in January. “We had hit the bottom of where the carriers were operating at, so there was no room to pull down carrier costs, and we’re operating in what is largely contractual volume,” he said. Hoping to work good margins in the spot market to offset that is possible, but as Wilkerson noted, “There aren’t a lot of spot loads out there in the market today.”

The numbers released by RXO showed the company’s total revenues were $1 billion, down from $1.1 billion in the fourth quarter of 2023.

That’s a 9% decline in revenue. That was strikingly close to the drop of just over 9% posted by the North American Surface Transportation segment at C.H. Robinson (NASDAQ: CHRW). Digital brokerage Uber Freight’s (NYSE: UBER) 12-month decline was 16.8%.

On an adjusted basis, RXO’s net income dropped to $7 million from $33 million a year ago. Its adjusted earnings before interest, taxes, depreciation and amortization was $31 million, down from $64 million a year earlier, and its adjusted EBITDA margin was 3.2%, down from 5.7% a year earlier.

James Harris, RXO’s CFO, said the “base case” for the company is that a freight market recovery would be emerging in the second half of the year. “Clearly, Q1 Is below where we expected it to be,” Harris said. If the second half of the year does show a recovery, Harris said, “we’re very confident we’ll grow that EBITDA in the back half of the year.”

More articles by John Kingston

Uber Freight’s revenue and EBITDA still weak

14-year-old case that brought ABC test to New Jersey was just settled

C.H. Robinson’s Q4 sees little improvement in shift at top of brokerage unit