North America’s largest third-party logistics provider held the line on trucking volumes but paid for it with profitability.

C.H. Robinson (NASDAQ: CHRW) reported its operating and financial results for the fourth quarter of 2019 after the close on Tuesday.

Robinson reported total revenues of $3.79 billion in the fourth quarter, down 8.3% year-over-year, and net income of $99.1 million, down 47% year-over-year. Earnings per share fell 45.5% year-over-year to $0.73, well below the Street’s consensus expectation of $0.96 per share.

CEO Bob Biesterfeld cited “a quarter of challenging operating results” but noted that Robinson’s brokers were able to adjust pricing and halt the truckload volume slide the company experienced in the third quarter. Less-than-truckload (LTL) volumes even grew 4.5% year-over-year, although volumes for the overall LTL sector were negative.

Biesterfeld called out how Robinson’s substantial investments in technology are beginning to drive operating efficiencies in the business, opening up a 330-bps favorable spread between truckload volume growth and headcount growth. If North American Surface Transportation’s (NAST) freight brokers can cover more loads per person per day, the company creates operating leverage such that a trucking recovery will generate asymmetric upside for Robinson.

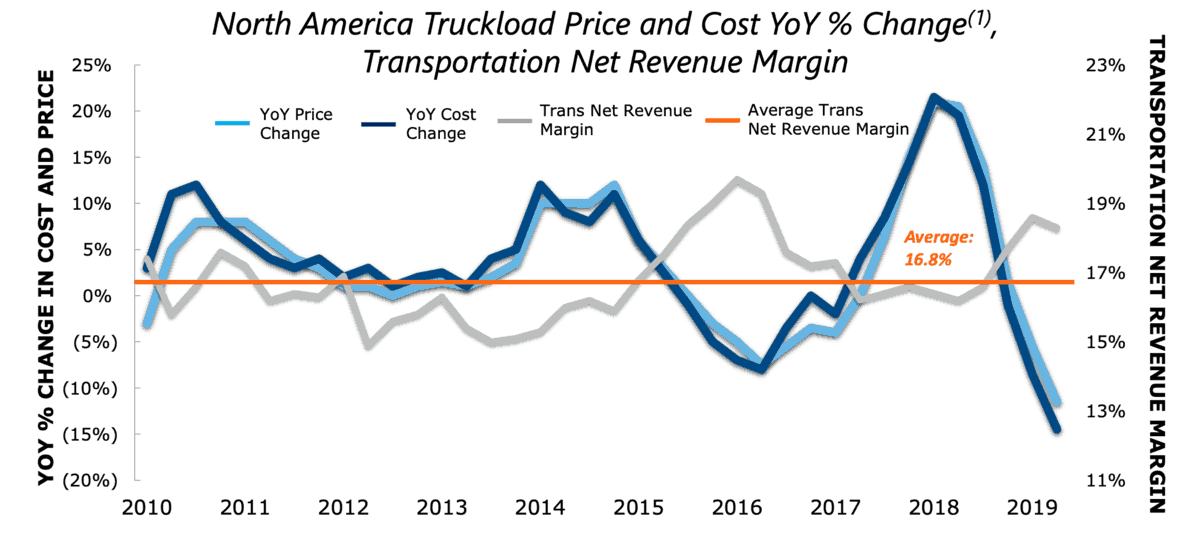

In the fourth quarter of 2019, C.H. Robinson management was faced with a choice: Let volumes continue to deteriorate and see market share fall, or reprice contractual business aggressively to maintain share at the expense of profitability.

Robinson chose the latter. While gross revenue did not fall as much year-over-year in the fourth quarter compared to the third quarter (-8.3% versus -10.2%, respectively), net income dropped precipitously (-47% in the fourth quarter compared to -16.5% in the third quarter).

After a year of loose capacity and low contract rates in the trucking industry, retail volumes popped in the fourth quarter of 2019. That volume tightened capacity and drove spot rates up at a time when contract rates were still being ratcheted down, compressing freight brokers’ net revenue margins.

Compared to the fourth quarter of last year, NAST’s net revenue margins compressed by 270 basis points to 14% — what appears to be the brokerage’s narrowest margin in 10 years.

“While our fourth quarter financial results demonstrate that we are not immune to large cyclical swings in the freight environment,” Biesterfeld said in a statement, “we firmly believe that our continued investments through cycles will drive the alignment between net revenue growth and operating costs needed to drive operating margin expansion through freight cycles over the long term.”

Net revenues in Robinson’s Global Forwarding division, which includes Ocean, Air, Customs and Other, fell across the board, although net revenue margins expanded to 21.5% from 21.1% a year ago, due to higher margins in Air. Space Cargo, a Spanish freight forwarder acquired in 2018, has been well integrated and contributed 2% to Ocean net revenue, 6% to Air net revenue and 1% to Customs net revenue.

Net revenues from All Other and Corporate, which includes the legacy Robinson Fresh business, were down 5% year-over-year to $59.2 million.

Shares of CHRW were down 7.5% in after-hours trading.

A Driver

Every broker thinks of their/their shareholders profit, while the truck is the one who delivers and at the current trend of undercutting each other, they just run trucking companies into the ground. One day they will face it, will be less trucks to deliver their “C”heap and “H”eavy Robinson freight.

Joe M Alvarez

I wish it was 35 years sooner. Truckers pay the price for their greed

Art

No company cares about employees, all that matters is profit being generated at lowest possible cost.

“Benefits”, “perks”, “cook outs” are just cheap forms of compensation.

Free life insurance costs 1 cent per hour.

Couple free lunches a year costs 1 cent per hour.

All the while they pay you less than competitors without these gimmicks.

If the company cares about employees/service providers why don’t they pay more per hour?

Elvis Durant

Cheap freight, cutting rates, and the diagnostic is that this is gonna get worst in 2020? Good luck!

47%? Ouch!

Art

The “digital” broker is going to kill margins for everyone in the industry.

Undercut market rates with venture capital money to buy customers.

Raise rates to finally make profit, next digital broker comes in with below market rates to get customer.

Vicious cycle race to the bottom as long as ignorant investors keep dumping money into money losing scams.

James

Robinson chose the latter. While gross revenue did not fall as much year-over-year in the fourth quarter compared to the third quarter (-8.3% versus -10.2%, respectively), net income dropped precipitously (-47% in the fourth quarter compared to -16.5% in the third quarter).

So in essence they sacrificed a 30% decline in Net income ” (-47% in the fourth quarter compared to -16.5% in the third quarter).”

in order to save a 1.9% decline in gross revenue ” While gross revenue did not fall as much year-over-year in the fourth quarter compared to the third quarter (-8.3% versus -10.2%, respectively ”

Am I the only one seeing an issue Here ?

Noble1= Shamash (Shemesh/Utu) the Babylonian God of the Sun(god of justice, morality, and truth-(enforcer of divine justice )

Their horizon is broad . They’re focusing on the long term . They understand the cycles in their industry . Short term pain for long term gain .

Quote:

“In the fourth quarter of 2019, C.H. Robinson management was faced with a choice: Let volumes continue to deteriorate and see market share fall, or reprice contractual business aggressively to maintain share at the expense of profitability.”

It’s a wise “business” decision .

In my humble opinion ……….

Dave

James, good point. Let me also add that they still made $99m in profit even with the % decrease. So 99m is still pretty good in this world today. Like I said, Convoy, Uber, TransFix, Load smart, Next trucking, shipwell, colane and the other so called digital brokers I read about daily must be bleeding cash to no end. Noble1 doesn’t know what he is talking about. I forcast that eventually at least half of the the digital guys just run out of cash as the only way to survive is to beg for more or to borrow it. Besides, all the legacy brokers are catching up fast (if they’ve not already) as the tech is so easy to get and use now and they are the ones with the deep customer contacts.

Art

Anyone can buy technology and software.. start up or traditional broker.

“digital” brokers still doing “traditional” load matching/booking..

The investors are so dumb.. believing uber is doing something different than the hundreds of competing brokers.

Noble1= Shamash (Shemesh/Utu) the Babylonian God of the Sun(god of justice, morality, and truth-(enforcer of divine justice )

Wow you’re quite a manipulator ,

First you start off by flattering him with your “good point” statement , then you convert to pointing out that they made $99 Million even though they’re earnings are lower , rather than pointing out why they earned less , and their game plan . You completely ignored his question .

Then you write about a whole different logistics topic while attempting to insult me in the process while attempting to portray yourself as an expert , LOL !

You’re not comparing apples to apples here . The article is based on C.H. ROBINSON earnings and it explains quite clearly why those earnings decreased .. That’s the point ! They’re not losing capital due to logistics ! In fact they are stating the opposite .

Quote:

“Biesterfeld called out how Robinson’s substantial investments in technology are beginning to drive operating efficiencies in the business, opening up a 330-bps favorable spread between truckload volume growth and headcount growth. If North American Surface Transportation’s (NAST) freight brokers can cover more loads per person per day, the company creates operating leverage such that a trucking recovery will generate asymmetric upside for Robinson.”

Currently the low rates are the cause of their losses .

Quote:

“In the fourth quarter of 2019, C.H. Robinson management was faced with a choice: Let volumes continue to deteriorate and see market share fall, or reprice contractual business aggressively to maintain share at the expense of profitability.

Robinson chose the latter.”

Quote:

“While our fourth quarter financial results demonstrate that we are not immune to large cyclical swings in the freight environment,” Biesterfeld said in a statement, “we firmly believe that our continued investments through cycles will drive the alignment between net revenue growth and operating costs needed to drive operating margin expansion through freight cycles over the long term.”

Now the least you can do is answer James question rather than ramble about other logistics co’s .

In my humble opinion ……….

Art

I think this means CHR is retaining customers who demanded freight rate decreased by giving in.

If CHR did not accept the customer’s rate reduction demands, customers would go to a lower priced broker like Uber, Convoy, Coyote, (or any of the other thousands of brokers).

CHR is hoping to maintain the customer until market rates increase and revenue will increase.

There seems to be a growing bubble of brokers/3PLs (commodification) which must depress margins for brokerages and carriers.

Most brokerages get new customers by offering rates at low or negative margin to get their foot in the door.

A ton of trucking companies have opened up brokerages too.

I don’t see how this will be sustainable.

Noble1= Shamash (Shemesh/Utu) the Babylonian God of the Sun(god of justice, morality, and truth-(enforcer of divine justice )

I wouldn’t be worried about these guys in the long term . They know what they are doing , and they’re expanding during this cyclical contraction . They will be fine . These guys manage over $20 Billion in freight and 18 million shipments annually .

Quote :

“While our fourth quarter financial results demonstrate that we are not immune to large cyclical swings in the freight environment,” Biesterfeld said in a statement, “we firmly believe that our continued investments through cycles will drive the alignment between net revenue growth and operating costs needed to drive operating margin expansion through freight cycles over the long term.”

I agree !

As for Convoy . Huge money behind them along with big brains and experience . Not worried for them in the least . They’re still considered to be in the start up phase .

UBER ? LOL ! While most were extremely negative on their 3rd quarterly earnings release in November 2019 , I called for a reversal in their stock . Most commenters don’t have a clue in their regard . Their stock price climbed and has performed quite well since then .

In my humble opinion …………

Art

How is Convoy going to revolutionize truck brokerage?

Automating finding trucks at the lowest price can be accomplished by any brokerage with an online bid system (little or no need for humans while carriers underbid each other online, like an eBay auction).

The whole efficiency and wasted miles reduction pitch by Convoy is smoke and mirrors.

Investors who don’t have a clue how the business work are being sold a fairy tale while Convoy burns their money.

Carriers run lanes they want/need to service their customers and drivers… not whatever Convoy considers to be most efficient or best for the environment.

The needs of drivers and the business often conflict with what is most efficient.

Dave

Art you are right. these so called digital brokers are just brokers. no difference. in fact pretty soon we will all be digital brokers lol

ThaGearJammer25/8

Good stuff. Stopped hauling for them two years ago. Figured overhead was so heavy they couldn’t pay carriers a decent wage.

Ohno

Having worked at CH. I can tell you that my friends that are still there are really worried. Wiehoff knew what was coming down the line. This is only going to get uglier.

Dave

I agree. Just imagine how bad the losses must be for Convoy ad Uber Freight. Ugly. Very ugly.

Art

So many brokers in the market today all chasing the same freight undercutting each other to get business.

Venture capital/private equity handing millions to Uber and Convoy to buy customers despite no profit.

Business fundamentals have taken a back seat.

Burn cash to grow! Makes so much sense!

JP

Big is not beautiful. 3.8 Billion Turnover. Net Income 99 million. Seriously, you don’t have to be Einstein to do the equations here.

As a wiseman said ‘ Turnover is Vanity, Profit is Sanity’.

Too many overheads and little margins, makes perfect sense, does’nt it ??????

Owned by equity companies looking to make a quick buck.

Watch this space and get your fingers burnt and the banks.

SME’s Forwarders are still the best.

sandi

Awesome, well said