Covenant Logistics’ (NASDAQ: CVLG) continued overhaul showed signs of gains as the truckload carrier posted a slight sequential gain in net income from the third quarter of this year while its operating ratio weakened slightly.

While most comparisons are done year-on-year, Covenant has stressed that it believes it is a radically different company than the one that exited 2019. Sequentially to the third quarter, this year’s net income of $10.48 million was slightly better than the $9.6 million posted earlier this year, though third quarter OR of 93.2% was somewhat better than the 93.7% recorded in the last three months of the year.

But year-to-year comparisons look strong also. Adjusted net income of $10.48 million in the fourth quarter of this year was significantly improved over the $1.87 million posted last year, and the adjusted operating ratio of 93.7% in this year’s Q4 was an improvement from the 98.8% recorded last year.

The fourth-quarter performance was not far off Wall Street estimates. The non-GAAP earnings of 61 cents per share was short of consensus by just 1 cent, according to SeekingAlpha. Revenue was short of consensus by $2.84 million, SeekingAlpha said.

The company’s earnings call is Tuesday. But in prepared remarks released in conjunction with the earnings report, Covenant’s chairman and CEO David Parker expressed satisfaction with the company’s progress in its quest to overhaul its operations. Among the gains he cited, a drop in revenue of less than $5 million year-on-year came from a fleet that he said is nearly 18% smaller than the fourth quarter of 2019.

Revenue was $225.2 million compared to $230.5 million last year. Freight revenue was $210.8 million versus $207.3 million. Operating income before charges showed the biggest boost, jumping to $9.56 million from $1.66 million.

Parker also said Covenant retired more than $200 million in debt and lease obligations.

Covenant took some significant charges during the quarter. Parker said the charges were $48 million in net cash and non-cash restructuring. That number included a $44 million hit on the impact of the TFS factoring operation that it sold to Triumph Bancorp, a sale that has been a mountain of troubles for Triumph so far.

“Our mission for 2021 is clear,” Parker said in the statement. “Seat more of our tractors, continue to control costs, and improve the profitability of certain legacy contracts in our Dedicated segment that generate unacceptable terms.”

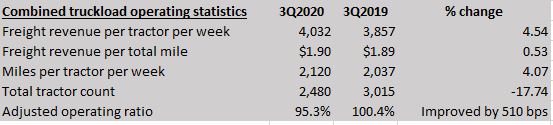

Although Parker cited a relatively small decline in revenue overall, in certain segments, the drop was more striking. In the combined truckload operations, revenue excluding fuel dropped to $131.4 million from a year ago, down from $152.8 million. But that group of operations posted adjusted operating income of more than $6.1 million after a small loss last year. The adjusted OR in the combined truckload segment strengthened to 95.3% from 100.4% last year.

Highlighting the greater efficiency that Parker spoke of, freight revenue per tractor per week in the truckload segment was $4,032 compared to $3,857. But that can be attributed in part to the stronger freight market. The number of miles traveled per tractor per week, a better sign of productivity, rose to 2,120 from 2,037.

The total tractor count that Parker cited in his statements stood at 2,480, down from 3,015.

The two parts within that Combined Truckload segment had significantly different ORs. The Expedited segment had an adjusted OR of 91.2%, a big improvement from the 99.3% posted last year. Meanwhile, the dedicated division’s OR was 99.9%, down from 101.6% a year ago. The unadjusted OR was more than 100%.

One thing that hasn’t changed, Parker said: “The average cost to resolve [insurance] claims continues to rise.”

More articles by John Kingston

Investors, Wall Street firm like Covenant’s bullish forecast

Sloppy earnings at Covenant but restructuring steps in Q2 were significant

Covenant sees ESG principles moving deeper into truckload segment’s strategy