Schneider National’s (NYSE: SNDR) third quarter report came in $0.02 light of analyst expectations at $0.32. This result excludes a $50.4 million restructuring charge associated with the closure of its First to Final Mile (FTFM) offering.

The bulk of the FTFM closure was completed by the end of August. The division saw a third quarter operating loss of $9 million. Total costs associated with closing FTFM are now expected to be at the low-end of management’s guidance range of $50 to $75 million. Schneider also booked an $11.5 million asset impairment charge on tractors held for sale. The company had a higher inventory of tractors held for sale due to lower freight volumes, slowing used equipment sales and the shuttering of FTFM. Schneider National was unable to place this equipment through its retail partner for re-sale, instead utilizing a block sale to unwind its fleet.

“We have taken a series of steps this year to position the company for 2020. Decisions around FTFM, our inventory of tractors held for sale and various cost-related initiatives were all made with a focus on the future,” said Schneider’s CEO and president Mark Rourke.

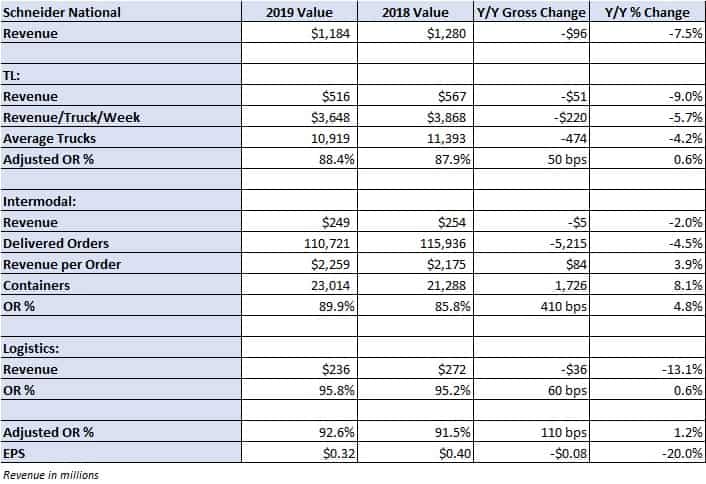

The truckload (TL) carrier reported an 8% decline in revenue year-over-year to $1.18 billion. The TL division saw revenue decline 9% as revenue per truck per week was 6% lower. Excluding items and events, the TL operating ratio was 50 basis points (bps) worse year-over-year at 88.4%. A weaker freight market highlighted by lower volumes and price were contributors to the division’s modest decline. Management said that there has been some seasonal capacity tightening in September and into October, but still well below last year’s levels. However, contract pricing has been flat in its for-hire offering on a year-over-year comparison.

“Despite challenging market conditions, our core operations performed well in the quarter. Both volumes and price were compressed compared to a year ago; however, for the first time in 2019, we experienced a moderate seasonal lift,” continued Rourke.

Intermodal revenue declined 2% year-over-year to $249 million as orders delivered declined 5%, partially offset by a 4% increase in revenue per order. Management said that intermodal contracts are renewing in the low single-digit range year-over-year. The company’s container fleet increased 8% year-over-year to slightly more than 23,000 units.

Intermodal operating ratio was 410 bps worse year-over-year at 89.9%. Management called out the volume weakness and increased third-party costs as the culprits. Looking forward to 2020 rail costs, management believes that any rate increases from the railroads will be “market sensitive” and dependent on traditional supply-demand fundamentals. The railroads have said that they anticipate capturing general cost inflation through rate increases, but some analysts believe that the railroads will look to take inflation-plus as they have done in the past.

Logistics revenue was 13% lower year-over-year at $236 million on 11% volume growth in brokerage, which was offset by a decline in revenue per order as “rates remained compressed throughout the quarter.” Also, the division had a volume headwind from a company that insourced some import/export business earlier in the year. The logistics operating ratio was 60 bps worse year-over-year at 95.8%, largely due to net revenue compression in brokerage.

Management took full-year 2019 adjusted earnings guidance lower due to the tractor impairment charge. The company now expects adjusted earnings per share (EPS) of $1.24 to $1.30 compared to prior guidance of $1.30 to $1.38 and the current consensus estimate of $1.32.

“In our Truckload segment, cost reduction initiatives and performance of our Dedicated business had positive impacts on third quarter results. Our Intermodal segment recorded the second- highest third quarter earnings despite the volume constrained domestic intermodal market. In our Logistics segment, brokerage volume grew 11% compared to a year ago and operating ratio improved 20 basis points sequentially in a difficult rate environment,” stated Rourke.

Shares of SNDR are up 1% on the day, much better than its TL peers that are seeing sharper declines.