This article was originally published in The Stockout newsletter on February 3, 2021. To sign up for The Stockout newsletter, click here.

We recommend that CPG companies, and others that ship refrigerated goods, pay close attention to Marten Transportation’s results each quarter. Marten, which reported its fourth quarter last week, is listed seventh on the Transport Topics list of top refrigerated carriers and is the only “refrigerated pure play” among the publicly traded carriers (Swift Refrigerated is fourth on the list, but its results are buried in the 18,000-tractor Knight-Swift trucking segment). So, Marten’s results can give CPG companies a unique insight into how refrigerated carriers are performing without the impact of dry goods getting in the way.

Marten reported record results and it did so more with freight selection than pure price.

In a carriers’ market, amid elevated refrigerated tender rejection rates and spot rates, a natural place to start to look for insights on reefer pricing is Marten’s revenue per loaded mile, excluding fuel surcharges. But Marten’s results add context to why that metric should not be used as a proxy for pricing. In Marten’s core Truckload segment, revenue per loaded mile was up a rather mild 1.8% y/y, but more striking growth was seen in other statistics. Average revenue per tractor per week, net of fuel, increased 10.2% y/y as the company’s number of loaded miles increased 3.5% (with an even more impressive 6.3% increase in total miles per tractor) and, importantly, the percent of the miles that the company was running empty declined from 12% to 10.4%. Those stats indicate that the carrier was able to achieve record results (its best operating revenue and best operating income for any quarter in the company’s 75-year history) largely by selecting freight that was higher margin because it lended itself to improved tractor utilization where the carrier did not have to run as many miles out of route or experience as much downtime.

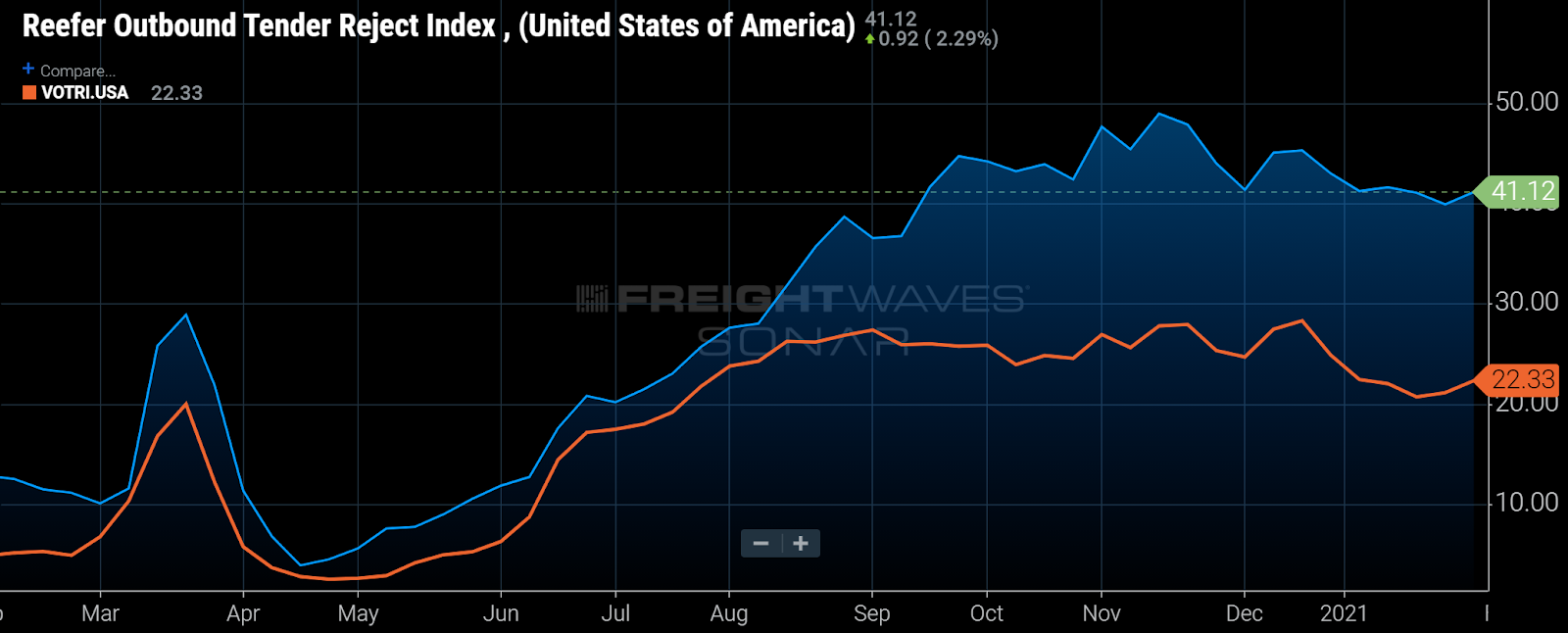

Amid higher tender rejection rates in reefer than in dry van, reefer carriers have improved their freight selection which, in turn, improves carriers’ tractor utilization and margins.

(Chart: FreightWaves SONAR: The blue and orange lines represent U.S. refrigerated and dry van tender rejection rates, respectively.)

But carriers’ focus on operations does not detract from their efforts to rate rates and Marten, for one, made clear that price increases are coming.

According to CEO Randy Marten, “We have been increasing and will continue to increase the compensation for our premium services within the tight freight market.” Separately, and not a comment specific to reefer, Knight-Swift guided investors to expect low double-digit contract rate increases in 2021. Other carriers have expressed similar sentiments on contract rate increases, citing both the tight truck market and the need to pass through costs, such as higher driver compensation levels.

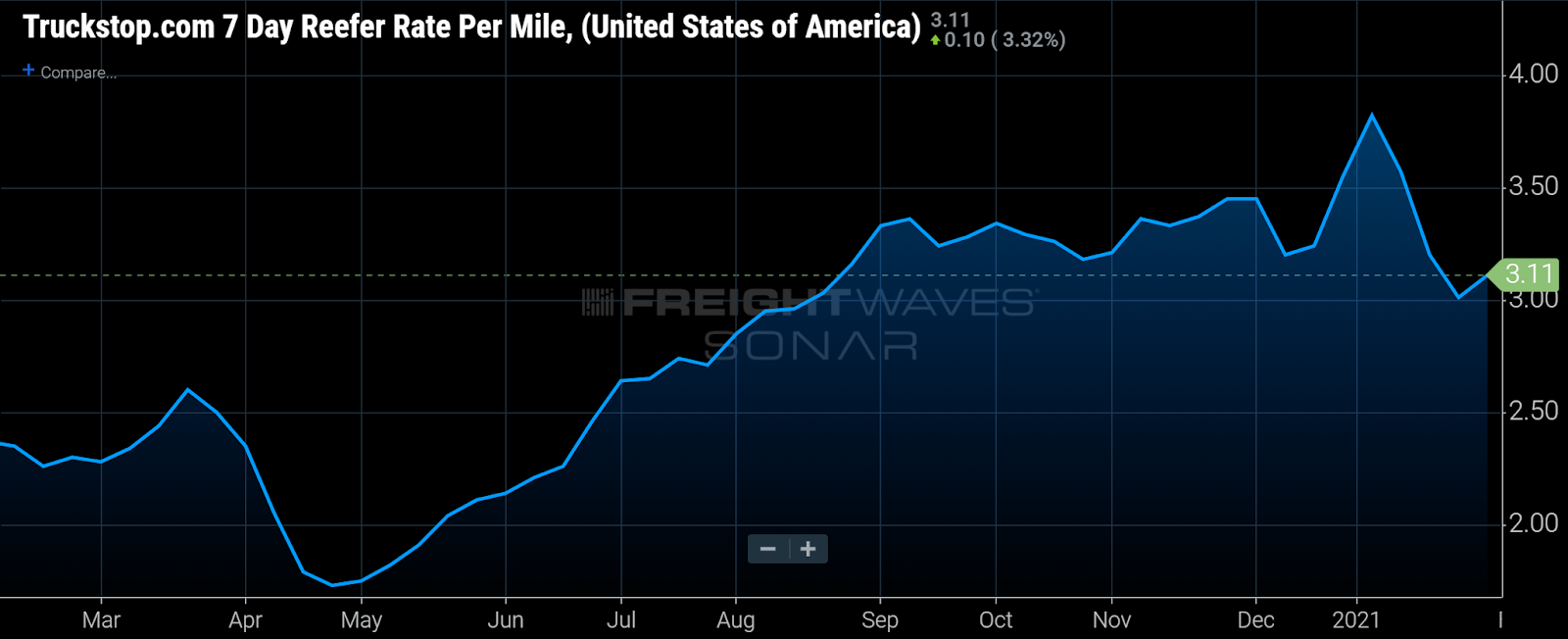

Many shippers of refrigerated loads are looking to avoid the elevated spot rates, like those shown below, by utilizing dedicated capacity.

(Chart: FreightWaves SONAR: Truckstop.com reefer rates per mile, including fuel surcharges.)

Marten is putting more capacity in its Dedicated segment, leaving less available capacity for shippers without the scale, or inclination, to enter into a multiyear contract.

Aside from the improvement in the utilization of the company’s fleet in its core Truckload segment, the other trend that most stood out to us in the company’s results is that it is putting a larger portion of its assets in its Dedicated division. In the 4Q20, Marten’s tractors were split nearly 50/50 between its Truckload and Dedicated divisions versus a 55/45 split in favor of its Truckload division in 4Q19. Accordingly, Dedicated has been the primary area of growth for the company; dedicated revenue increased 20% y/y in 4Q20.

We believe the capacity shift toward dedicated is largely a response to shippers’ desire to avoid the spot market and carriers’ desire to mitigate cyclical impacts.

Shippers are looking to avoid the spot market after experiencing a shockingly tight freight market during most of last year, which has persisted into this year, with the latest average Truckstop.com nationwide reefer rate of $3.11 mile (including fuel surcharges). The carrier benefits from a shift toward dedicated because it makes its business models more stable and gives downside protection for when market conditions loosen. Highlighting the stability of Marten’s dedicated segment from the carriers’ perspective, contracts in Marten’s truckload segment are typically one year in length versus the typical three- to five-year length for a dedicated contract. In addition, the company’s “nonrevenue miles percentage” (which includes nonpaid out-of-route miles) is only 0.7% in its dedicated segment versus 10.5% in its truckload segment.

CPG companies may have to adapt their logistics strategies for the tighter reefer market.

Marten’s results, and comments from carriers pointing analysts to double-digit contract rate increases, should serve as a reminder for consumer goods companies that it is important to make themselves preferred shippers. That includes not only being accommodative on rates, but also taking actions that can improve carriers’ equipment utilization such as helping carriers reduce wait times during loading and unloading and working with carriers to identify loads that fit well into their networks. In addition, CPG companies and other shippers will likely have to be at least somewhat accommodative on rate increases that will go toward inflation in carriers’ labor expenses. CPG companies that do not have the scale to enter into a dedicated contract will likely find capacity less available than even the market data that highlights reefer capacity tightness would suggest. Shippers that do have the scale to enter into a dedicated contract may want to buck the industry trend and avoid entering into a multiyear agreement at what could be the top of the market. As we’ve learned, a lot can change in a year.