This week’s CPG news items reflect a continuation of recent food/beverage trends.

More crossover between soft drink and alcoholic drinks: Monster Beverage is the latest soft drink company to get into adult beverages by acquiring CANarchy Craft Brewery Collective, an owner of craft breweries, in a deal worth $330 million. Other recent examples of category crossover include the Coca-Cola-owned Topo Chico brand (which now offers both alcoholic and nonalcoholic varieties) and Hard Mountain Dew (a collaboration between Pepsi and Boston Beer Company).

Surging food prices: Butter prices are up ~40% year-over-year, driven by slower milk production, the labor shortage and rising packaging costs. That percentage increase is even worse than inflation in meat (Tyson has raised prices on meat 11%-39%, depending on the segment), which has been the category hitting consumers’ wallets the hardest on a dollar basis.

Additional packaging constraints: According to Constellation Brands, a shortage of brown glass is impairing its imported beer volume. Scarcity in bottles comes despite the shift in share away from bottled beer to canned beer and the market share shift away from beer, in general, to liquor, seltzers and canned cocktails. During the pandemic, beer makers have had difficulty sourcing aluminum cans, often having to rely on the unusual practice of importing cans.

Also a continuation of recent trends, freight data in SONAR shows continued tightness in the freight markets. Here is a mini highlight reel of 5 SONAR charts:

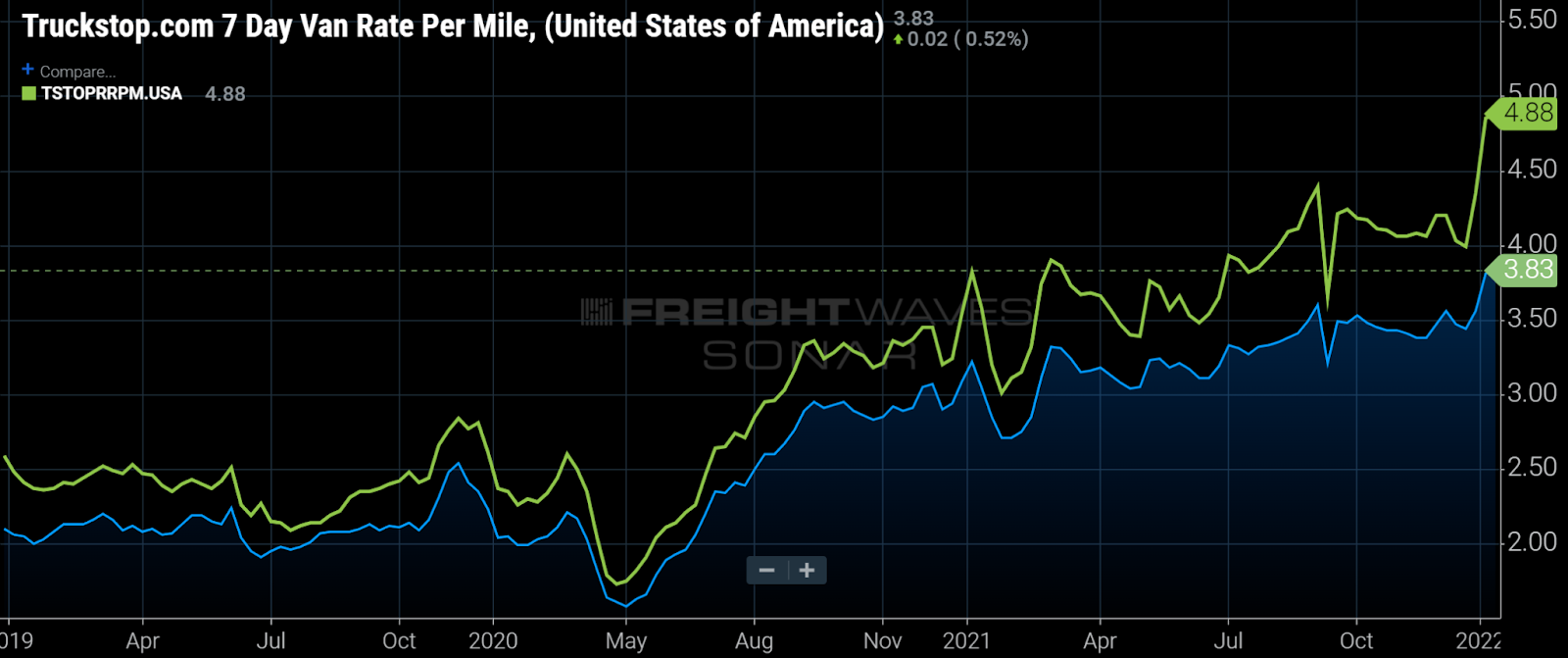

Truckload spot rates hit fresh highs. Dry van (blue) and reefer (green) spot rates, including fuel surcharges, average $3.83/mile and $4.88/mile, respectively. Those rates are likely to come down in the coming weeks as more capacity returns to the market following the holidays, but in general, rates for on-demand capacity continue to rise, showing continued tightness in the truckload sector.

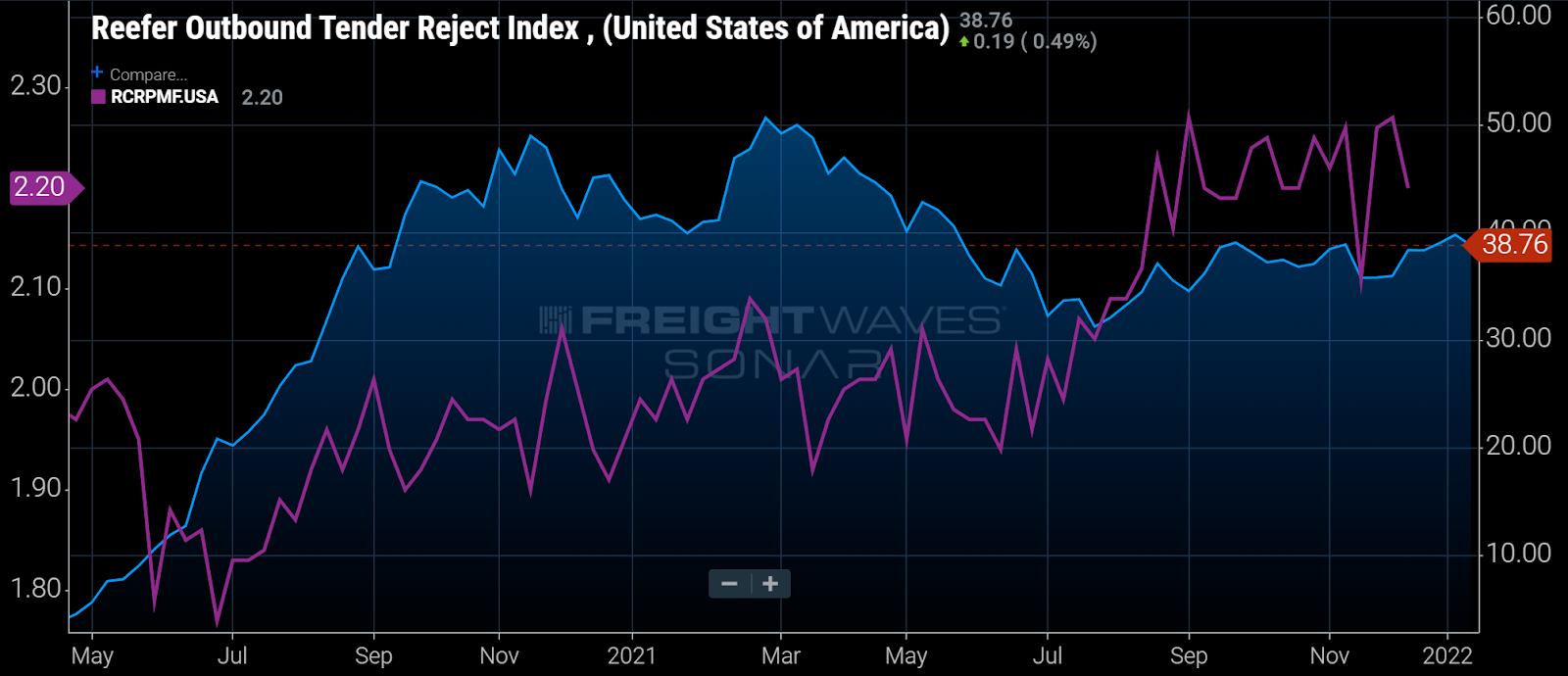

Reefer carriers are rejecting 39% of tenders. While it’s not quite the “coin-flip compliance” of last spring, the current reefer tender rejection rate is especially remarkable after the past year of rising contract rates. Reefer contract rates are up in the double-digit percentages versus last year at this time (purple line on left axis below). One might have expected carriers to become significantly more compliant after contracts were renegotiated at higher rates.

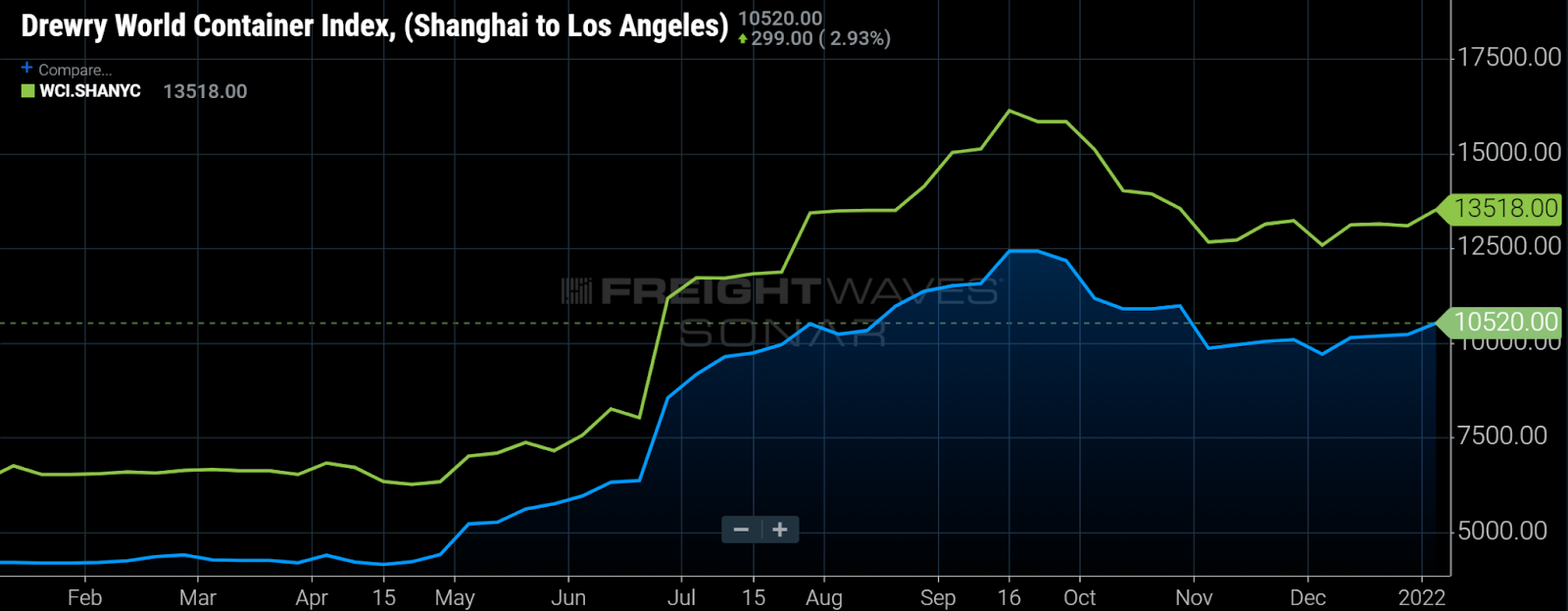

Ocean rates have stabilized at a highly elevated level. Late last year, eastbound trans-Pacific ocean rates had declined ~25% from their September highs after rising ~3x from late 2020. Some recent appreciation now leaves rates ~15% off those September highs, suggesting that the ocean markets are unlikely to immediately correct. If congestion at the ports eased, the resulting improvement in vessel productivity would effectively increase capacity and lower rates, but vessel congestion has only gotten worse to start the year.

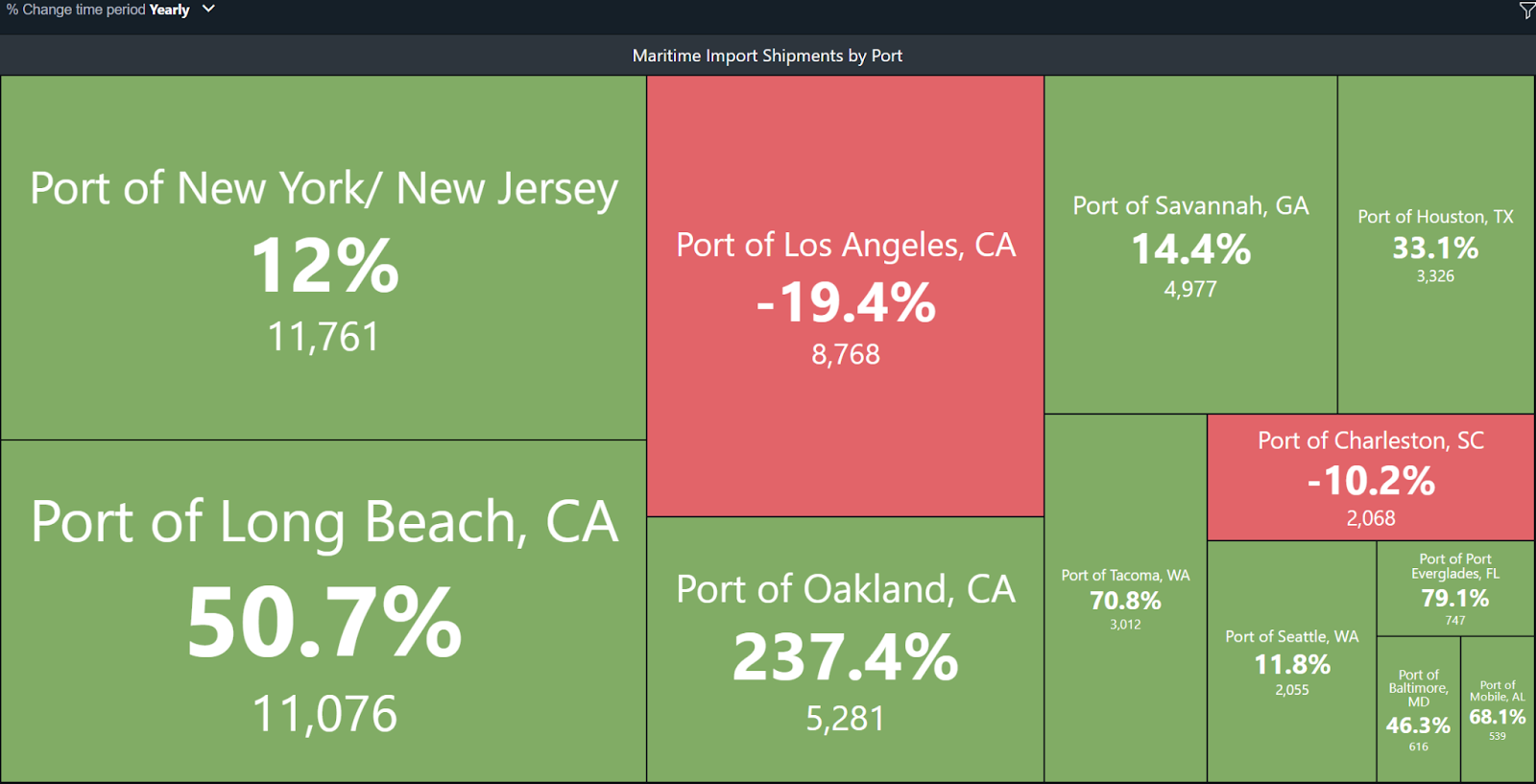

Import volume should keep driving demand for domestic freight transportation and warehousing space. Maritime import shipment volume in SONAR (which includes both containerized and non-containerized volume) is significantly higher than year-ago levels in nearly all the major U.S. ports.

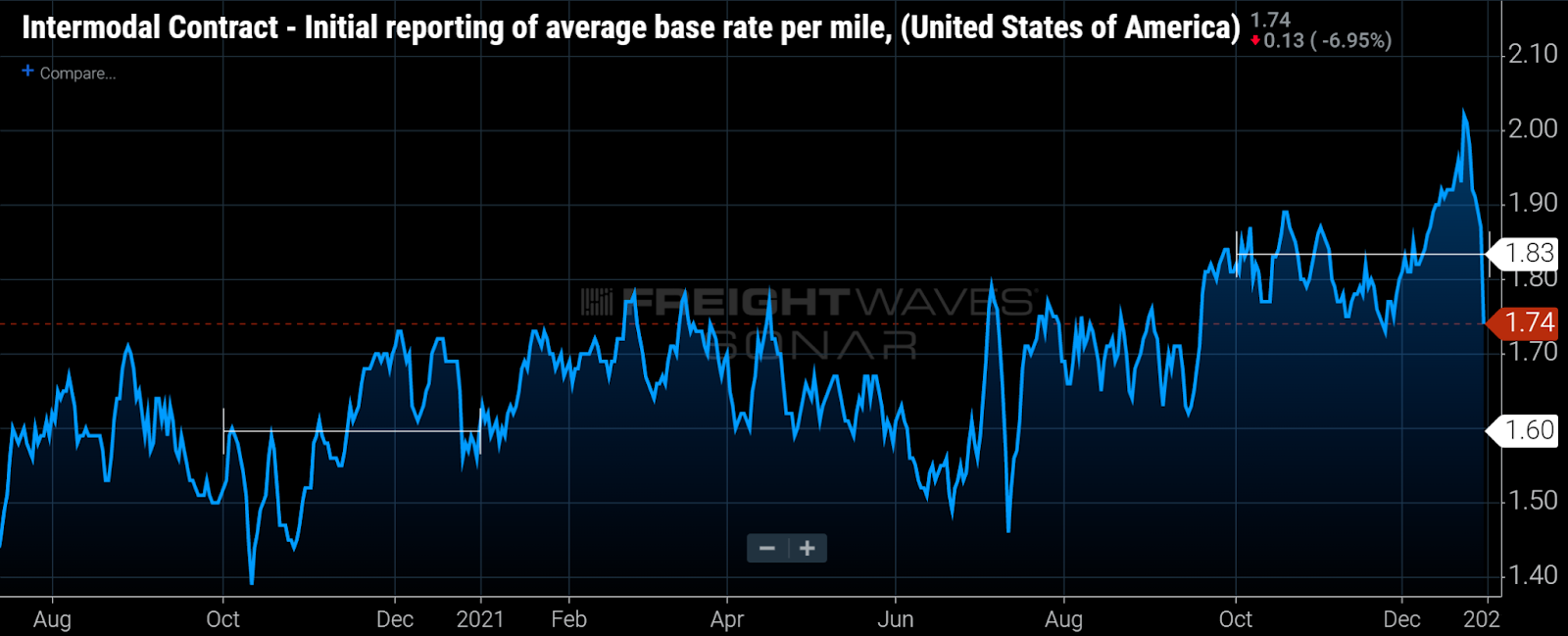

Intermodal contract rates (not including fuel) were up 14% y/y in 4Q21. The past year was frustrating for domestic intermodal shippers that saw their contract rates rise double digits while also experiencing delays due to terminal congestion and equipment shortages. As annual domestic intermodal contract reprice in 2022, shippers are likely to see rates again rise double digits on top of last year’s increases.

For other highlights from SONAR, check out the latest SONAR Highlight Reel.

To sign up for The Stockout, a free newsletter focused on CPG supply chains, please click here.