Wall Street didn’t like Clorox’s earnings report late last week. There were analyst downgrades and shares are down from where they were a week ago and down 10% from their level three months ago. The company is in a tough spot with uncertainty over whether demand for its cleaning products will remain elevated as COVID declines, a supply chain that has become more complex, and input costs that are rising faster than its prices. Clearly, the company doesn’t want to be perceived as price gouging to take advantage of COVID and has therefore taken a very measured approach to pricing. That puts the company in a difficult position given the highly inflationary environment where input costs are rising across the board.

To sign up for The Stockout, a newsletter focused on CPG supply chains, please click here.

Clorox’s gross margin contracted 320 basis points in its fiscal 3Q, the first contraction in 10 quarters. This comes despite evidence that consumer habits that were adopted during the pandemic, such as frequent cleaning and eating at home, are largely sticking, at least for now. Revenue in the company’s just-reported fiscal 3Q was flat y/y following 15% growth in the year-ago quarter. The decline in gross margin was largely driven due to higher manufacturing costs, higher input costs and higher logistics costs. The company now expects its gross margin to be down for its current fiscal year.

Despite sharply rising costs, Clorox has been reluctant to raise prices during the pandemic on items such as cleaning products to avoid the perception of gouging. Of course, if the company were to raise prices significantly, it wouldn’t be price gouging, it would instead be a rational action to pass rising costs on to consumers. Other consumer products companies, such as Procter & Gamble and Kimberly-Clark have announced price increases in the mid-to-high-single-digit range. Those CPG companies use some of the same inflationary inputs, such as resin, which is an input in the production of baby products. The difference may be that those products are not as closely tied to fighting the pandemic as Clorox cleaning products. Plus, it remains to be seen whether there will be a consumer backlash since most of the price increases from other CPG companies are not coming until this fall.

Clorox called out resin as one of the primary inputs where costs are rising sharply; resin is used in plastics and the higher costs are hitting the cost to produce Glad trash bags. That is one of the product lines where the company does plan to raise prices in the coming months. Interestingly, one analyst pointed out that the last time the company raised prices of Glad trash bags there was market share loss to cheaper alternatives. What may be different this time is that the rising input costs are widespread with competitors facing the same cost pressure and also likely to raise prices. Presumably, competitors selling cheaper products are operating on thinner margins and will have to raise prices for those products to remain profitable.

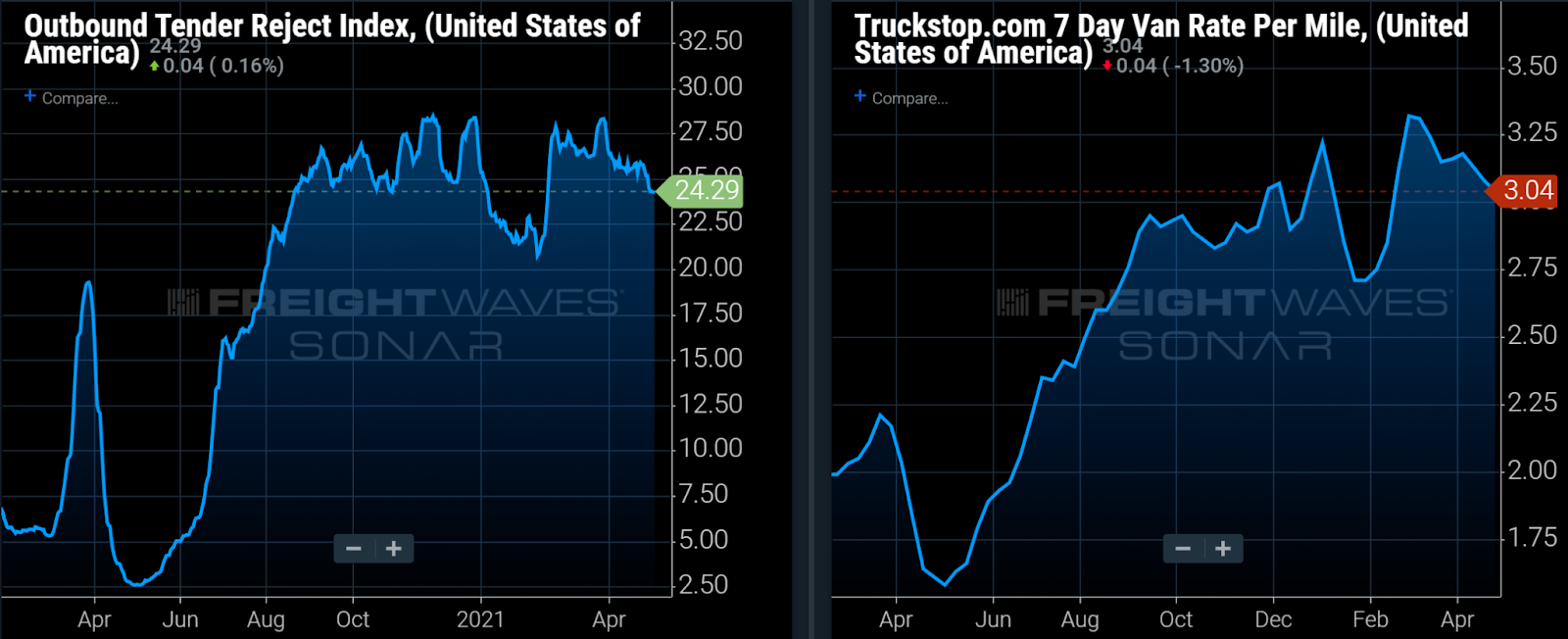

What a difference a year makes for transportation costs. Last year at this time, carriers were more compliant, rejecting fewer than 5% of loads (left chart below) and dry van spot rates were below $1.75 mile/including fuel surcharges (right chart below). Today, carriers are rejecting nearly one-quarter of all tendered loads and spot rates exceed $3 per mile, including fuel surcharges. Unlike many other costs, CPG companies are typically unable to hedge freight costs. Regional granularity contained in SONAR shows that many of the tightest freight markets are small and midsized markets in the Central states.

To learn more about FreightWaves SONAR, click here.

Clorox is struggling with supply chain issues in certain categories. The products called out by the company on its analyst call were its Brita product line, particularly Brita filters, and disinfecting wipes and sprays. The company is larger than it was before the pandemic and it is now using more third parties (perhaps using third parties as surge capacity) and expanding manufacturing capacity, which has added complexity to the company’s supply chain. As the company explained, the more that the company has expanded its supply chain, the more nodes it has and the more supply chain risk it introduces.

While those challenges are numerous, Clorox remains a cash-generating machine. The company targets free cash flow of between 11% and 13% of sales; has a return-on-invested capital of 30%; has a 2.4% dividend yield; and has repurchased an average of more than $300 million of shares per year the past five years. The company could also use its balance sheet to supplement cash return to shareholders since its leverage ratio of 1.9x is below the company’s targeted range of 2.0x-2.5x. Those are enviable metrics.

To receive The Stockout, FreightWaves’ CPG-focused newsletter, please click here.